Research

Findings #14: Health Insurance Status of the Civilian Noninstitutionalized

Population, 1999

by Jeffrey A. Rhoades, Ph.D., and May C. Chu,

B.A., Agency for Healthcare Research and Quality

Abstract

This report from the 1999 Medical Expenditure Panel Survey (MEPS) provides preliminary estimates of the health insurance status of the civilian noninstitutionalized U.S. population during the first half of 1999, including the size and characteristics of the population with private health insurance, with public insurance only, and without any health care coverage. During this period, 84.2 percent of all Americans were covered by private or public health insurance, leaving 15.8 percent of the population, some 42.8 million people, uninsured. Among the non-elderly population, 82.1 percent of Americans had either private or public coverage only and 17.9 percent of the population (42.6 million people) lacked health care coverage. Among the elderly population, there was a significant drop from 1998 to 1999 in private health insurance coverage and a corresponding significant increase in coverage by public health insurance only. The probability that an individual would be uninsured during this period was especially high for young adults ages 1924 and members of racial and ethnic minorities (especially Hispanics). Public health insurance continues to play an important role in ensuring that children, black Americans, and Hispanic Americans obtain health care coverage.

Introduction

This report is the fourth in a series

of reports on the health insurance status of the U.S. population.

Previous reports have presented health insurance estimates

for the first part of 1996 (Vistnes and Monheit, 1997), 1997

(Vistnes and Zuvekas, 1999), and 1998 (Rhoades, Brown and

Vistnes, 2000).

The health insurance status of the U.S.

population, especially the size and composition of the uninsured

population, has become an issue of perennial public policy

concern for several reasons. First, health insurance is viewed

as essential to ensure that individuals obtain timely access

to medical care and protection against the risk of expensive

and unanticipated medical events. Compared to people without

health care coverage, insured individuals are more likely

to have a usual source of medical care, to spend less out

of pocket on health services, and to experience different

treatment patterns, quality, and continuity in their health

care (Lefkowitz and Monheit, 1991; U.S. Congress, Office of

Technology Assessment, 1992).

Second, concern over the population's

health insurance status reflects a variety of equity and efficiency

considerations. These include the magnitude and appropriate

mix of private and public sector responsibility for financing

health care, the impact of health insurance on the efficient

use of health care, and the manner in which health insurance

affects the distribution of health care among the general

population and across groups of specific policy interest.

Third, timely and reliable estimates of

the population's health insurance status are essential to

evaluate the costs and expected impact of public policy interventions

to expand coverage or to alter the manner in which private

and public insurance is financed. Identification of how individual

and household demographic characteristics, health status,

and economic circumstances are associated with the population's

health insurance status is of critical importance in developing

efficient and targeted policy interventions. This is especially

relevant given the current emphasis on incremental health

care reform that is focused on particular health care markets

and population groups.

Finally, comparisons

of the characteristics of insured and uninsured populations

over time provide information

on whether greater equity has been achieved in the ability

of specific population groups to obtain health insurance or

whether serious gaps remain. In this regard, estimates of

the population's health insurance status from the Medical

Expenditure Panel Survey (MEPS), which is conducted annually,

provide critical data for evaluating the health insurance

implications of recent legislative initiatives: the 1996 Health

Insurance Portability and Accountability Act (HIPAA), Public

Law 104–191; welfare reform under the 1996 Personal Responsibility

and Work Opportunity Reconciliation Act, Public Law 104–193;

and the 1997 State Children's Health Insurance Program (SCHIP).

A primary goal of HIPAA is to reduce the impact of preexisting

health conditions on the continuity of health insurance during

employment transitions. Under welfare reform, mandated work

requirements and time limitations governing the receipt of

public assistance may have consequences for a recipient's

health insurance status. The goal of the SCHIP program is

to provide health insurance coverage to low-income children

who are not eligible for Medicaid.

This report presents preliminary estimates

of the number and characteristics of people with private and

public health insurance at any time during the first half

of 1999, on average. Particular emphasis is directed toward

estimating the size of the population that was uninsured throughout

the first half of 1999 and identifying groups especially at

risk of lacking health insurance.

^top

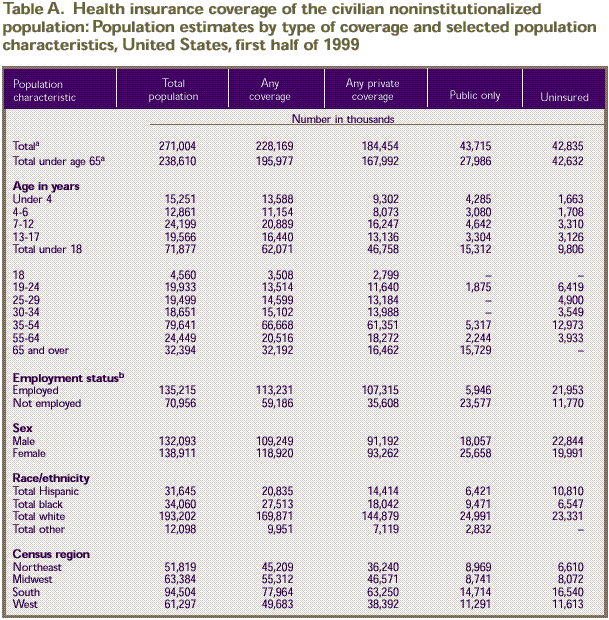

Overview

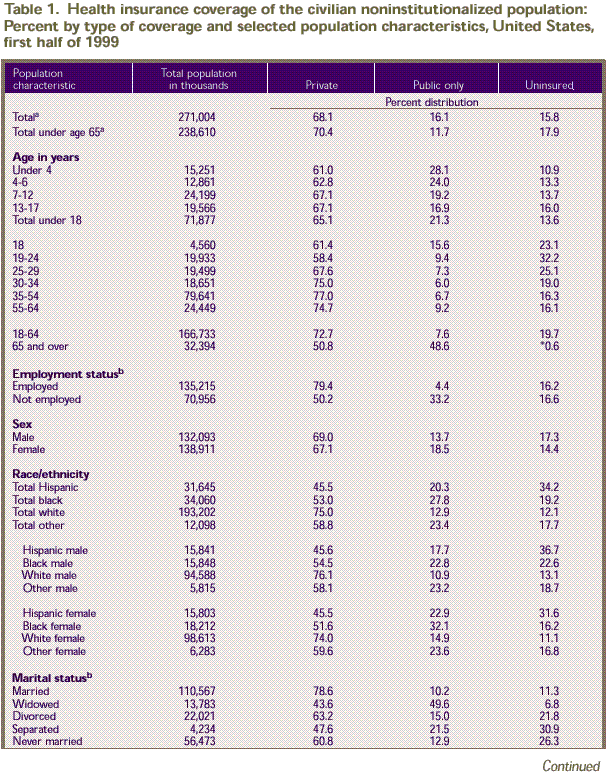

During the first half of 1999, on average,

84.2 percent of all Americans in the civilian noninstitutionalized

population had some type of private or public health insurance

coverage (Table 1). About 68

percent of Americans obtained health insurance from private

sources. Another 16.1 percent had only public sources of coverage,

primarily Medicare and Medicaid. (Throughout this report,

the public health insurance category includes only people

who had no coverage except public health insurance.) The remaining

15.8 percent of Americans, 42.8 million people, were without

health insurance throughout the first half of 1999. Among

the non-elderly population, 70.4 percent were covered by private

insurance and 11.7 percent by public insurance. Among the

non-elderly population, an estimated 42.6 million individuals

(17.9 percent) were uninsured. Table

2 gives more detailed information on the health insurance

status of the non-elderly population.

Overall these health insurance estimates

do not differ significantly from the 1998 MEPS figures for

the non-elderly population, as reported in Rhoades, Brown,

and Vistnes (2000). However, there were differences between

the two years for the elderly population. These differences

are discussed below.

Tables

1-3 provide

estimates of the population's health insurance status according

to selected demographic characteristics, perceived health

status, employment status, and residential location. Table

4 provides estimates of the distribution of the uninsured

population by selected characteristics. Table

A in the technical appendix provides

estimates of the number of people by health insurance status.

Some of the key findings and relationships revealed by these

data are discussed below.

Age

MEPS data reveal that, in general, children

are more likely than non-elderly adults to have health insurance

coverage. The main findings among age groups are described

below.

Children

There has been considerable interest in

the health insurance status of children. This interest stems

from the role health care coverage plays in ensuring that

children obtain the medical care appropriate to their specific

stage of development. To help ensure such coverage, Congress

passed the State Children's Health Insurance Program in 1997,

allocating approximately $24 billion over 5 years to provide

health insurance coverage to low-income children who are not

eligible for Medicaid. The SCHIP program follows on Medicaid

expansions beginning in the late 1980s that focused attention

on the role of the public and private sectors in financing

health care for low-income children.

MEPS data indicate

that public health insurance covered a substantial proportion

of children in

the first half of 1999: 28.1 percent of children under age

4, one in four children ages 4–6 (24.0), and one in five

children ages 7–12 (19.2) had public coverage, primarily

through Medicaid. As a result, the proportion uninsured among

children under age 18 (13.6 percent) was lower than the proportion

among non-elderly adults in general (19.7 percent for ages

18–64). Despite this finding, about 9.8 million children

lacked health care coverage.

Adults

Young adults

ages 19–24 were the

age group most likely to lack health insurance. Nearly a third

of young adults (32.2 percent) were uninsured, twice the rate

at which all Americans lacked coverage.

Slightly more than half of elderly Americans

(50.8 percent) were covered by private health insurance. Slightly

less than half of elderly Americans (48.6 percent) held public

coverage only (Medicare alone or in conjunction with Medicaid).

These estimates differ significantly from estimates for 1998,

when 55.3 percent of the elderly were covered by private health

insurance and 43.8 percent were covered by public health insurance.

This continues a trend first observed between 1997 and 1998,

when the percent of the elderly covered by private health

insurance declined from 60.5 percent to 55.3 percent (Rhoades,

Brown, and Vistnes, 2000).

There are several possible reasons for

the observed drop in private health insurance coverage among

the elderly. Increases in Medicare health maintenance organization

enrollment may have prompted people to drop private health

insurance; people may have elected to drop Medigap health

insurance policies as premiums have risen; and former employers

may have opted to discontinue private health insurance coverage

for retirees or have become unable to provide such coverage.

However, there are currently insufficient data to determine

definitively why these changes have occurred over the 3-year

period.

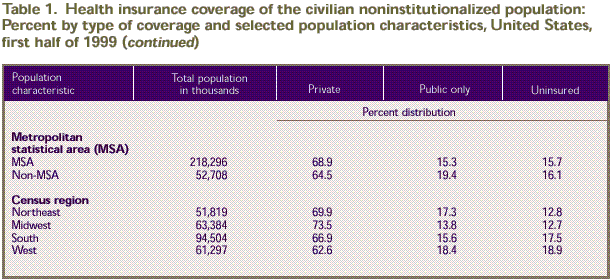

Employment Status

Since most

private health insurance in the United States is provided

through the workplace, employment

status is an important indicator of access to private health

insurance. MEPS data reveal the following for the population

ages 16–64 (Table 2):

- Almost four-fifths (79.9 percent) of

workers were covered by private health insurance, compared

to half (51.2 percent) of individuals who were not employed.

- People who were not employed were more

likely than those who were employed to be covered by public

insurance (21.8 and 3.4 percent, respectively).

- Workers were less likely than people

who were not employed to be uninsured (16.8 and 27.0 percent,

respectively).

Race/Ethnicity

MEPS data indicate that significant disparities

exist in the rate at which racial and ethnic minorities are

covered by private and public health insurance compared to

white Americans (Table 1). For

example:

- Less than half of all Hispanic Americans

(45.5 percent) and slightly more than half of black Americans

(53.0 percent) were covered by private health insurance,

compared to three-quarters of whites (75.0 percent). Over

a third of Hispanics (34.2 percent) and almost a fifth of

blacks (19.2 percent) were uninsured. In contrast, 12.1

percent of white Americans were uninsured.

- Hispanic and black Americans were more

likely than white Americans to be covered by public health

insurance (20.3 percent and 27.8 percent, respectively,

compared to 12.9 percent for white Americans).

Marital Status

Widowed people were less likely to have

private health insurance coverage in 1999 (43.6 percent) than

in 1998 (50.7 percent) and more likely to have public insurance

only (49.6 percent and 43.1 percent, respectively) (Rhoades,

Brown, and Vistnes, 2000). These changes in health insurance

coverage for widowed people can be attributed to similar changes

observed among the elderly population, many of whom are widowed,

for the two years (data not shown). Among adults under age

65, married people were more likely to have private health

insurance (82.0 percent) and less likely to have public insurance

(4.7 percent) or be uninsured (13.3 percent) than unmarried

people were (Table 2). Of people

ages 16–64 who were not married at the time of the survey:

- Over one-quarter of widowed people were

uninsured (26.4 percent).

- Almost one-quarter of all divorced people

were uninsured (24.6 percent). The proportion of divorced

people covered by public insurance declined from 13.8 percent

in 1998 (Rhoades, Brown, and Vistnes, 2000) to 9.5 percent

in 1999.

- Almost one-third of Americans who were

separated were uninsured (32.8 percent).

- More than one-quarter of Americans who

never married were uninsured (26.8 percent).

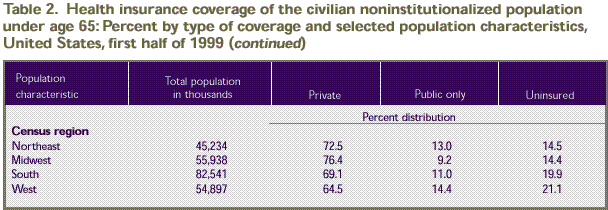

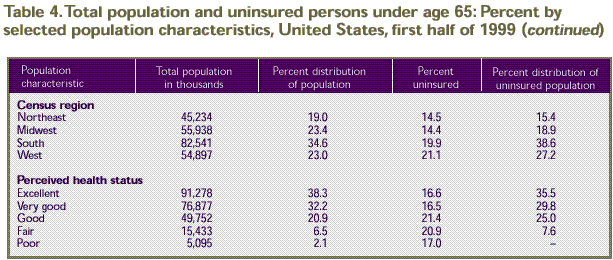

Residential Location

The type of health care coverage obtained

by Americans and the likelihood of being uninsured also varied

by region and whether or not they lived in a metropolitan

statistical area (MSA). Table 1 shows

that:

- People living outside MSAs were less

likely than those living within MSAs to be covered by private

health insurance (64.5 percent vs. 68.9 percent).

- People living in the West were less likely

than residents of the Northeast and Midwest to have private

health insurance (62.6 percent in the West compared to 69.9

percent in the Northeast and 73.5 percent in the Midwest).

Nearly one out of five people in the West and South were

uninsured (18.9 percent and 17.5 percent, respectively),

compared to 12.8 percent in the Northeast and 12.7 percent

in the Midwest.

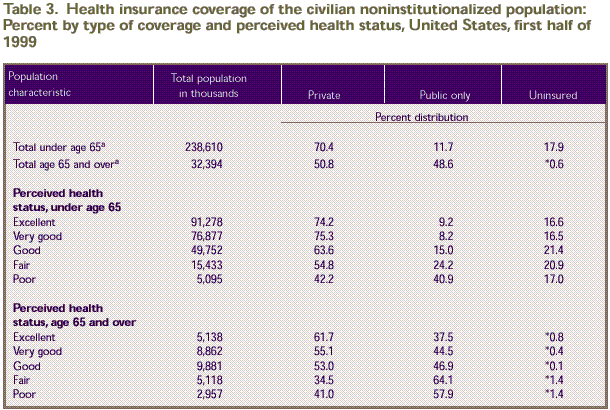

Health Status

There is considerable public policy interest

in determining whether people with health problems are able

to obtain health insurance and, if so, the source of such

coverage. MEPS respondents were asked to rate their health

and family members' health as excellent, very good, good,

fair, or poor. The data in Table

3 reveal the relationships described below between health

status and insurance coverage.

Non-Elderly People

More than one in five non-elderly Americans

in good health (21.4 percent) or fair health (20.9 percent)

were uninsured throughout the first half of 1999. Among the

non-elderly:

- People in fair or poor health were less

likely than those in better health to have private health

insurance. Only 42.2 percent of those in poor health and

54.8 percent of those in fair health had any private coverage.

- Public insurance helped to reduce the

health-related disparities in coverage. Almost one-quarter

(24.2 percent) of people in fair health and 4 in 10 (40.9

percent) of the people in poor health had public coverage.

Nevertheless, those in good or fair health were more likely

than people in very good or excellent health to be uninsured.

Elderly People

Elderly Americans in fair or poor health

were less likely to have private coverage than those in good

or better health. As a result, those in fair or poor health

were more likely to be covered by insurance from public sources

only (64.1 percent and 57.9 percent, respectively) than other

elderly Americans. Medicare, either alone or with Medicaid,

was the main public source of coverage. There were significant

differences between the 1999 and 1998 estimates for elderly

people in fair health: a significant decrease in the percent

covered by private health insurance (34.5 percent in 1999

vs. 49.0 percent in 1998) and a corresponding significant

increase in the percent covered by public health insurance

only (64.1 percent in 1999 vs. 50.7 percent in 1998). Presently

there are insufficient data to determine why these changes

have occurred between the two years.

^top

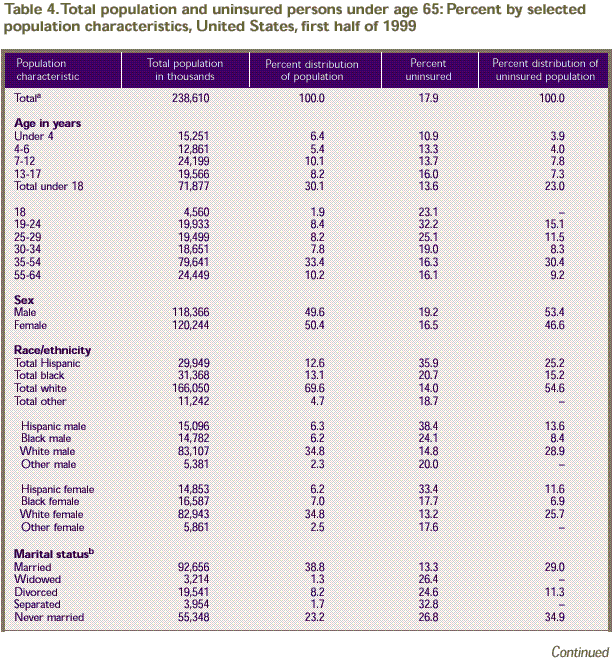

Characteristics of Uninsured Americans

Previous sections of this report have

described the health insurance status of Americans by focusing

on demographic, health status, and geographic characteristics

associated with the likelihood that particular groups obtained

private or public health insurance or were more at risk of

being uninsured. To put this discussion in perspective, data

displayed in Table 4 characterize

the uninsured population by considering the representation

of specific groups in the general population of non-elderly

Americans relative to their representation among the uninsured

population. In this way, one can assess whether certain population

groups are disproportionately represented among the uninsured.

Such information can be useful in formulating targeted policy

interventions on behalf of people without health insurance.

Age

Children under

the age of 18 comprised slightly less than one-quarter (23.0

percent) of the uninsured

population. Young adults ages 19–24 composed 8.4 percent

of the non-elderly population but 15.1 percent of the uninsured

population. Among all age groups, young adults had the greatest

risk of being uninsured.

For individuals

ages 30–34 and 55–64,

there was a significant change in the percent distribution

of the uninsured population between 1998 and 1999. The proportion

of the uninsured population represented by ages 30–34

declined from 10.0 percent in 1998 to 8.3 percent in 1999,

while the proportion ages 55–64 increased from 6.8 percent

in 1998 to 9.2 percent in 1999. These changes reflect a shift

in the age distribution of the population between 1998 and

1999 rather than a change in risk for being uninsured.

Sex

While males comprised slightly less than

half of the non-elderly population, they represented 53.4

percent of the uninsured population.

Race/Ethnicity

Racial and ethnic minorities were more

at risk of lacking health insurance than white Americans were.

As a result, minority representation among the uninsured exceeded

their representation among the general population. For example, Table

4 shows that:

- Hispanics represented only 12.6 percent

of all non-elderly Americans but 25.2 percent of the uninsured

population. Hispanics were the racial/ethnic group most

likely to be uninsured (35.9 percent).

- Although almost 7 out of 10 non-elderly

Americans were white (69.6 percent), whites accounted for

less than 6 out of 10 uninsured persons (54.6 percent).

- When the uninsured are categorized by

race/ethnicity and sex, white males and females represent

the largest proportions of the uninsured population: 28.9

and 25.7 percent, respectively.

^top

Conclusions

Preliminary estimates from the 1999 MEPS

reveal that, during the first half of 1999, 68.1 percent of

Americans obtained health insurance from private sources,

16.1 percent obtained coverage through public programs, and

15.8 percent of the population (42.8 million people) lacked

any health care coverage. Among the non-elderly population,

over one person in six was uninsured.

In general, there was no difference between

the 1998 and 1999 estimates for the non-elderly population.

However, among the elderly population there was a significant

drop in the rate of private health insurance coverage and

a corresponding significant increase in public health insurance

coverage only, a trend that continues from 1997.

The tabulations

presented in this report indicate that the health insurance

status of the U.S. population

is strongly associated with specific demographic characteristics,

health status, and employment status. Important disparities

in health care coverage exist for particular groups. Among

the groups especially at risk of lacking health care coverage

are young adults ages 19–24 and members of racial and

ethnic minorities (especially Hispanic Americans). Public

health insurance continues to play an important role in insuring

children, black Americans, and Hispanic Americans. Disparities

in the proportion with insurance coverage also exist by health

status, with non-elderly people in good or fair health more

likely than people in better health to be uninsured.

^top

References

Cohen J, Monheit

A, Beauregard K, et al. The Medical Expenditure Panel Survey:

a national health information

resource. Inquiry 1996;33:373–89.

Cohen S. Sample

design of the 1996 Medical Expenditure Panel Survey Household

Component. Rockville (MD):

Agency for Health Care Policy and Research; 1997. MEPS Methodology

Report No. 2. AHCPR Pub. No. 97–0027.

Lefkowitz D,

Monheit A. Health insurance, use of health services, and

health care expenditures. Rockville

(MD): Agency for Health Care Policy and Research; 1991. National

Medical Expenditure Survey Research Findings 14. AHCPR Pub.

No. 92–0017.

Rhoades J,

Brown E, Vistnes J. Health insurance status of the civilian

noninstitutionalized population:

1998. Rockville (MD): Agency for Healthcare Research and Quality;

2000. MEPS Research Findings No. 11. AHRQ Pub. No. 00–0023.

U.S. Congress, Office of Technology Assessment.

Does health insurance make a difference? Background paper.

Washington: U.S. Government Printing Office; 1992. Report

No. OTA-BP-H-99.

Vistnes J,

Monheit A. Health insurance status of the civilian noninstitutionalized

population: 1996.

Rockville (MD): Agency for Health Care Policy and Research;

1997. MEPS Research Findings No. 1. AHCPR Pub. No. 97–0030.

Vistnes J,

Zuvekas S. Health insurance status of the civilian noninstitutionalized

population: 1997.

Rockville (MD): Agency for Health Care Policy and Research;

1999. MEPS Research Findings No. 8. AHCPR Pub. No. 99–0030.

^top

Tables

a Includes persons with unknown

employment status and marital status.

b For individuals age 16 and over.

* Relative standard error is greater than

or equal to 30 percent.

Note: Percents may not add to 100

because of rounding.

Source: Center for Financing, Access,

and Cost Trends, Agency for Healthcare Research and Quality:

Medical Expenditure Panel Survey Household Component, 1999.

a Includes persons with unknown

employment status and marital status.

b For individuals age 16 and over.

Note: Percents may not add to 100

because of rounding.

Source: Center for Financing, Access,

and Cost Trends, Agency for Healthcare Research and Quality:

Medical Expenditure Panel Survey Household Component, 1999.

a Total includes persons with

unknown perceived health status.

* Relative standard error is greater than

or equal to 30 percent.

Note: Percents may not add to 100

because of rounding.

Source: Center for Financing, Access,

and Cost Trends, Agency for Healthcare Research and Quality:

Medical Expenditure Panel Survey Household Component, 1999.

a Total

includes persons with unknown perceived health status and

marital status.

b For individuals age 16 and over. Excludes unknown

marital status. As a result, percents do not sum to 100.

- Sample

size too small to produce reliable estimates.

Note: Percent

distributions may not add to 100 because of rounding.

Source: Center

for Financing, Access, and Cost Trends, Agency for Healthcare

Research and Quality: Medical Expenditure Panel Survey Household

Component, 1999.

^top

Technical Appendix

This data in this report were obtained

in the first round of interviews for the Household Component

(HC) of the 1999 Medical Expenditure Panel Survey (MEPS).

MEPS is cosponsored by the Agency for Healthcare Research

and Quality (AHRQ) and the National Center for Health Statistics

(NCHS). The MEPS HC is a nationally representative survey

of the U.S. civilian noninstitutionalized population that

collects medical expenditure data at both the person and household

levels. The focus of the MEPS HC is to collect detailed data

on demographic characteristics, health conditions, health

status, use of medical care services, charges and payments,

access to care, satisfaction with care, health insurance coverage,

income, and employment. In other components of MEPS, data

are collected on the use, charges, and payments reported by

providers; residents of licensed or certified nursing homes;

and the supply side of the health insurance market.

The sample for the MEPS HC was selected

from respondents to the National Health Interview Survey (NHIS),

which was conducted by NCHS. NHIS provides a nationally representative

sample of the U.S. civilian noninstitutionalized population

and reflects an oversampling of Hispanics and blacks. The

MEPS HC collects data through an overlapping panel design.

In this design, data are collected through a precontact interview

that is followed by a series of five rounds of interviews

over 2 1/2 years. Two calendar years of medical expenditure

and utilization data are collected from each household and

captured using computer-assisted personal interviewing (CAPI).

This series of data collection rounds is launched again each

subsequent year on a new sample of households to provide overlapping

panels of survey data which, when combined with other ongoing

panels, will provide continuous and current estimates of health

care expenditures. The reference period for Round 1 of the

1999 MEPS HC (Panel 4) was from January 1, 1999, to the date

of the Round 1 interview. Interviews for Panel 4 (Round 1)

were conducted from March to July 1999.

Derivation of Insurance Status Information

The household respondent was asked if

during the interview period anyone in the family was covered

by any of the sources of public and private health insurance

coverage discussed in the following paragraphs. Coverage by

Medicare and TRICARE, formerly known as CHAMPUS/CHAMPVA, was

measured at the time of the interview. (CHAMPUS and CHAMPVA

were the Civilian Health and Medical Programs for the Uniformed

Services and Veterans' Affairs.) All other sources of insurance

were measured for any time between January 1999 and the interview

date. Persons counted as uninsured were uninsured throughout

this time period.

Public Coverage

For this report, individuals were considered

to have public coverage only if they met both of the following

criteria:

- They were not covered by private insurance.

- They were covered by one of the public

programs discussed below.

Medicare

Medicare is a federally financed health

insurance plan for the elderly, persons receiving Social Security

disability payments, and most persons with end-stage renal

disease. Medicare Part A, which provides hospital insurance,

is automatically given to those who are eligible for Social

Security. Medicare Part B provides supplementary medical insurance

that pays for medical expenses and can be purchased for a

monthly premium.

Tricare

TRICARE covers active-duty and retired

members of the Uniformed Services and the spouses and children

of active-duty, retired, and deceased members. Spouses and

children of veterans who died from a service-connected disability,

or who are permanently disabled and are not eligible for Medicare,

are covered by TRICARE. In this report, TRICARE coverage is

considered to be public coverage. When persons covered by

TRICARE reach age 65, their coverage generally ends and enrollees

are eligible for Medicare.

Medicaid and State Children's Health

Insurance Program

Medicaid and the State Children's Health

Insurance Program (SCHIP) are means-tested government programs

jointly financed by Federal and State funds that provide health

care to those who are eligible. Eligibility criteria vary

significantly by State. Medicaid is designed to provide health

insurance coverage to families and individuals who are unable

to afford necessary medical care, while SCHIP is designed

to provide health insurance coverage for uninsured low-income

children. Respondents who did not report Medicaid or SCHIP

coverage were asked if they were covered by any other public

hospital/physician coverage. These questions were asked in

an attempt to identify Medicaid or SCHIP recipients who might

not have recognized their coverage as Medicaid or SCHIP. In

this report, all coverage reported in this manner is considered

public coverage.

Private Health Insurance

Private health insurance was defined for

this report as insurance that provides coverage for hospital and

physician care (including Medigap coverage). Insurance that provides

coverage for a single service only, such as dental or vision coverage,

was not counted. Private health insurance could have been obtained

through an employer, union, self-employed business, directly from

an insurance company or a health maintenance organization (HMO),

through a group or association, or from someone outside the household. Uninsured

The uninsured were defined as persons

not covered by Medicare, TRICARE, Medicaid, other public hospital/physician

programs, or private hospital/physician insurance (including

Medigap coverage) during the period from January 1999 through

the time of the interview. Individuals covered only by noncomprehensive

State-specific programs (e.g., Maryland Kidney Disease Program)

or private single-service plans (e.g., coverage for dental

or vision care only, coverage for accidents or specific diseases)

were not considered to be insured.

Health Insurance Edits

For the Round 1 (Panel 4) sample, minimal

editing was performed on sources of public coverage and no

edits were performed on the private coverage variables. Health

insurance data were edited as described below.

Medicare

Medicare coverage was edited for persons

age 65 and over but not for persons under age 65. Persons

age 65 and over were assigned Medicare coverage if they met

one of the following criteria:

- They answered "yes" to

a follow-up question on whether they had received Social

Security benefits.

- They were covered by Medicaid, other

public hospital/physician coverage, or Medigap coverage.

- Their spouse was age 65 or over and covered

by Medicare.

- They were covered by TRICARE.

Medicaid

This report does not distinguish among

sources of public insurance. Medicaid or other public hospital/physician

coverage was included when considering whether an individual

was covered only by public insurance.

Tricare

Respondents age 65 and over who reported

TRICARE coverage were instead classified as covered by Medicare.

Private Health Insurance

Private insurance coverage was unedited

and unimputed for Round 1 (Panel 4). Individuals were considered

to be covered by private insurance if the insurance provided

coverage for hospital/physician care. Medigap plans were included.

Individuals covered by single-service plans only (e.g., dental,

vision, or drug plans) were not considered to be privately

insured. Sources of insurance with missing information regarding

the type of coverage were assumed to contain hospital/physician

coverage.

Population Characteristics

Place of Residence

Individuals were identified as residing

either inside or outside a metropolitan statistical area (MSA)

as designated by the U.S. Office of Management and Budget

(OMB), which applied 1990 standards using population counts

from the 1990 U.S. census. An MSA is a large population nucleus

combined with adjacent communities that have a high degree

of economic and social integration within the nucleus. Each

MSA has one or more central counties containing the area's

main population concentration. In New England, metropolitan

areas consist of cities and towns rather than whole counties.

Regions of residence are in accordance with the U.S. Bureau

of the Census definition.

Race/Ethnicity

Classification by race and ethnicity was

based on information reported for each household member. Respondents

were asked if their race was best described as American Indian,

Alaska Native, Asian or Pacific Islander, black, white, or

other. They were also asked if their main national origin

or ancestry was Puerto Rican; Cuban; Mexican, Mexicano, Mexican

American, or Chicano; other Latin American; or other Spanish.

All persons who claimed main national origin or ancestry in

one of these Hispanic groups, regardless of racial background,

were classified as Hispanic. Since the Hispanic grouping can

include black Hispanic, white Hispanic, and other Hispanic,

the race categories of black, white, and other do not include

Hispanic.

Employment Status

Persons were considered to be employed

if they were age 16 and over, and had a job for pay, owned

a business, or worked without pay in a family business at

the time of the Round 1 interview.

Sample Design and Accuracy of Estimates

MEPS is designed

to produce estimates at the national and regional level

over time for the civilian

noninstitutionalized population of the United States and some

subpopulations of interest. Each MEPS panel collects data

covering a 2-year period, with the first four MEPS panels

spanning 1996–97, 1997–98, 1998–99, and 1999–2000.

The data in this report are from the first round of data collection

for the MEPS Panel 4 sample.

The statistics presented in this report

are affected by both sampling error and sources of nonsampling

error, which include nonresponse bias, respondent reporting

errors, interviewer effects, and data processing misspecifications.

For a detailed description of the MEPS survey design, the

adopted sample design, and methods used to minimize sources

of nonsampling error, see Cohen (1997) and Cohen, Monheit,

Beauregard, et al. (1996). The MEPS person-level estimation

weights include nonresponse adjustments and poststratification

adjustments to population estimates derived from the March

1999 Current Population Survey (CPS) based on cross-classifications

by region, MSA status, age, race/ethnicity, and sex.

Tests of statistical significance were

used to determine whether the differences between populations

exist at specified levels of confidence or whether they occurred

by chance. Differences were tested using Z-scores having asymptotic

normal properties at the 0.05 level of significance. Unless

otherwise noted, only statistical differences between estimates

are discussed in the text.

At its beginning

in 1999, MEPS Panel 4 consisted of a sample of 6,875 households,

a nationally representative

subsample of the households responding to the 1998 National

Health Interview Survey. Like earlier MEPS panels, the Panel

4 sample reflects the oversampling of Hispanic and black households

resulting from the NHIS sample design.

The overall MEPS Panel 4 response rate

at the end of Round 1 (which collects data for the first part

of 1999) was 73.0 percent. This overall rate reflects response

to both the 1998 NHIS interview and the MEPS Round 1 interview.

Rounding

Estimates presented in the tables were

rounded to the nearest 0.1 percent. Standard errors, presented

in Tables B–E, were rounded

to the nearest 0.01, while for Table

F they were rounded to the nearest whole number. Population

estimates in Tables 1–4 and Table

A were rounded to the nearest thousand. Therefore, some

of the estimates presented in the tables for population totals

of subgroups will not add exactly to the overall estimated

population total.

Comparisons With Other Data Sources

Because of

methodological differences, caution should be used when

comparing these data with data

from other sources. For example, CPS measures persons who

are uninsured for a full year; NHIS measures persons who lack

insurance at a given point in time—the month before the

interview. The CPS interview that contains information on

the health insurance status of the population is conducted

annually, and NHIS collects insurance data on a continuous

basis each year. In addition, unlike MEPS, CPS counts as insured

military veterans whose source of health care is the Department

of Veterans Affairs. CPS also counts children of adults covered

by Medicaid as insured. For these preliminary estimates, MEPS

did not consider these children insured unless their families

reported them as such.

a Includes

persons with unknown employment status and marital status.

b For individuals age 16 and over.

- Sample

size too small to produce reliable estimates.

Source: Center

for Financing, Access, and Cost Trends, Agency for Healthcare

Research and Quality: Medical Expenditure Panel Survey Household

Component, 1999.

a Includes

persons with unknown employment status and marital status.

b For individuals age 16 and over.

* Relative standard error is greater than

or equal to 30 percent.

Source: Center for Financing, Access,

and Cost Trends, Agency for Healthcare Research and Quality:

Medical Expenditure Panel Survey Household Component, 1999.

a Includes

persons with unknown employment status and marital status.

b For individuals age 16 and over.

Source: Center for Financing, Access,

and Cost Trends, Agency for Healthcare Research and Quality:

Medical Expenditure Panel Survey Household Component, 1999.

a Includes

persons with unknown perceived health status.

* Relative standard error is greater than

or equal to 30 percent.

Source: Center for Financing, Access,

and Cost Trends, Agency for Healthcare Research and Quality:

Medical Expenditure Panel Survey Household Component, 1999.

a Total

includes persons with unknown perceived health status and

marital status.

b Not applicable.

c For individuals age 16 and over.

- Sample

size too small to produce reliable estimates.

Source: Center

for Financing, Access, and Cost Trends, Agency for Healthcare

Research and Quality: Medical Expenditure Panel Survey Household

Component, 1999.

a Includes

persons with unknown employment status and marital status.

b For individuals age 16 and over.

- Sample

size too small to produce reliable estimates.

Source: Center

for Financing, Access, and Cost Trends, Agency for Healthcare

Research and Quality: Medical Expenditure Panel Survey Household

Component, 1999.

^top

Suggested

Citation:

Rhoades, J. A. and Chu, M. C. Research

Findings #14: Health Insurance Status of the Civilian Noninstitutionalized

Population: 1999. December 2000. Agency

for Healthcare Research and Quality, Rockville,

MD.

http://www.meps.ahrq.gov/data_files/publications/rf14/rf14.shtml |

|