Chartbook #23: Medical Expenditure Panel Survey Insurance Component 2018 Chartbook

Acknowledgments

This chartbook was prepared by Jessica Vistnes, G. Edward Miller, Philip Cooper, Patricia Keenan, and Asako Moriya of the Center for Financing, Access, and Cost Trends (CFACT) in the Agency for Healthcare Research and Quality (AHRQ). Primary editing was performed by Jessica Vistnes and Edward Miller.

The authors appreciate the efforts of Eneli Coakley, Zhengyi Fang, and Bidong Liu of Social and Scientific Systems in preparing the exhibits in the chartbook, the data production work of Brandon Flanders of the U.S. Census Bureau, and the production assistance of Doreen Bonnett, Nicole Shulman, and Michelle Roberts of AHRQ.

Reviewers of this publication were Joel W. Cohen, Director of CFACT; Steve Machlin, Director, David Kashihara, Senior Health Statistician, and Pradip Muhuri, Survey Statistician (Division of Statistical Research and Methods in CFACT); Tom Selden, Director, Steve Hill, Senior Economist, and Sandy Decker, Yao Ding, Paul Jacobs, and Chandler McClellan (Service Fellows) (Division of Research and Modeling in CFACT).

Introduction

Background

Data Presentation

References

Executive Summary

Section 1: Health Insurance Offer Rates

Section 2: Employee Eligibility and Enrollment

Section 3: Health Insurance Premiums

Section 4: Employee and Employer Premium Contributions

Section 5: Employee Cost Sharing

The data used in this report are from the Insurance Component of the Medical Expenditure Panel Survey. Information about this survey, including sample design, data collection, sample sizes, and response rates, can be found

at https://meps.ahrq.gov/survey_comp/Insurance.jsp.

This product is in the public domain and may be used and reprinted without permission in the United States for noncommercial purposes, unless materials are clearly noted as copyrighted in the document. No one may reproduce copyrighted materials without the permission of the copyright holders. Users outside the United States must get permission from AHRQ to reprint or translate this product.

Anyone wanting to reproduce this product for sale must contact AHRQ for permission.

Agency for Healthcare Research and Quality

5600 Fishers Lane

Rockville, MD 20857

www.ahrq.gov

Suggested Citation

Medical Expenditure Panel Survey Insurance Component 2018 Chartbook.

Rockville, MD: Agency for Healthcare Research and Quality;

September 2019. AHRQ Publication No. 19-0077.

https://meps.ahrq.gov/mepsweb/data_files/publications/cb23/cb23.shtml.

The Medical Expenditure Panel Survey Insurance Component (MEPS-IC) is an annual survey of private employers and State and local governments. The MEPS-IC produces national and State-level estimates of employer-sponsored insurance, including offered plans, costs, employee eligibility, and number of enrollees. The MEPS-IC is sponsored by the Agency for Healthcare Research and Quality and is fielded by the U.S. Census Bureau.

This chartbook provides both single-year and multiyear trend analyses using private-sector MEPS-IC data from 2005 to 2018. To best convey key information from the MEPS-IC, the report is presented in five sections: Health Insurance Offer Rates; Employee Eligibility and Enrollment; Health Insurance Premiums; Employee and Employer Premium Contributions; and Employee Cost Sharing. Each section provides charts and discussion with links to MEPS-IC data tables that contain the estimates and standard errors for each exhibit.

Many of the estimates in this publication are categorized by firm sizes that are relevant to recent changes in national healthcare policy. The firm-size categories used in the charts and tables are based on actual employment counts rather than full-time equivalent (FTE) counts, because the MEPS-IC does not collect FTE employment figures.

Each section discusses the estimates to highlight trends and differences by employer and workforce characteristics. If a comparison of estimates is presented in the discussion, any differences are statistically significant at the 0.05 level, unless otherwise noted. In some cases, differences noted in the text, in estimates as well as statistical significance of comparisons, may vary slightly from calculations performed using data in the exhibits, MEPS-IC data available on the MEPS website, or MEPS-IC Statistical Briefs due to rounding. All dollar estimates are nominal (not adjusted for inflation).

Return to Table of Contents

The IC is one of three annual component surveys that make up MEPS. The other two components are the Household Component (HC) and the Medical Provider Component (MPC). The HC is a nationally representative survey of the U.S. civilian noninstitutionalized population that collects data at both the person and household levels. The MPC collects information from a sample of physicians, hospitals, home health agencies, and pharmacies that provided services to HC respondents.

The MEPS-IC uses two independent samples: the private sector and the public sector. The private-sector sample is composed of about 42,000 business establishments from more than 7 million establishments found on the Business Register at the U.S. Census Bureau, with 5.5 percent of the sample determined during the data collection process to be out of scope. In 2018, the response rate for the private sector was 67.8 percent of the remaining in-scope sample units.

An establishment is a single business entity or location. Firms (also often referred to as companies) can include one or more establishments. An example of a multi-establishment firm is a chain of grocery stores, where the establishments of the firm are the sites of the individual grocery stores. The charts and tables in this publication report characteristics within firm-based size categories.

The public-sector sample of the MEPS-IC selects almost 3,000 State and local government agencies. However, this report focuses only on the private sector.

Additional information on MEPS-IC sampling can be found in Sample Design of the 2014 Medical Expenditure Panel Survey Insurance Component (Davis, 2015; PDF).

There was no MEPS-IC survey to collect 2007 data due to the transition from retrospective to current-year data collection. This methodological change improved the accuracy and timeliness of the IC estimates. More information about this design change can be found in

Switching From Retrospective to Current-Year Data Collection in the Medical Expenditure Panel Survey – Insurance Component (Kearney & Sommers, 2007). References to changes in all years from 2005 to 2018 in the text refer to 1-year changes except for changes in 2008, which refer to the period from 2006 to 2008.

Return to Table of Contents

For purposes of the analyses presented in this chartbook, the District of Columbia is treated as a State.

In addition, exhibits are organized by category (e.g., premium type, firm size), so

references to exhibits in the text may not be in numeric order (e.g., Exhibits 3.1, 3.3, and 3.5 instead of 3.1, 3.2, and 3.3).

Return to Table of Contents

Davis K. Sample design of

the 2017 Medical Expenditure Panel Survey Insurance Component. Methodology

Report #31. Rockville, MD: Agency for Healthcare Research and Quality; July

2018. https://meps.ahrq.gov/data_files/publications/mr31/mr31.shtml.

Accessed August 23, 2019.

Kearney A, Sommers J. Switching from retrospective to current-year data collection in

the Medical Expenditure Panel Survey - Insurance Component. ICES-III: Third

International Conference on Establishment Surveys, Conference Proceedings, Montréal, Québec, Canada; June 2007.

Return to Table of Contents

Overview

Employer-sponsored insurance (ESI) is the primary source of health insurance coverage for individuals under age 65. This chartbook uses data for private-sector establishments in the Medical Expenditure Panel Survey-Insurance Component (MEPS-IC) to describe trends in employer coverage, premiums, and benefits from 2005 to 2018.

The MEPS-IC is an annual survey of private employers and State and local governments and is designed to be representative of all 50 States and the District of Columbia. The large sample size (about 42,000 private-sector establishments), combined with a response rate of 67.8 percent in 2018, permits analyses of variations in ESI by firm size and across States that are not readily available from other sources.

Examining trends by firm size and across States is important due to variation in insurance markets along these dimensions. Historically, insurance markets have differed by firm size due to smaller firms' more limited ability to pool risk and their higher administrative costs compared with larger firms. State variation in ESI markets may reflect differences in employment patterns, healthcare prices, and utilization, as well as differences in State approaches to regulating private insurance and administering Medicaid.

This chartbook describes trends and patterns in ESI overall, by firm size, and by State from 2005 to 2018. All differences noted are at the 0.05 significance level unless otherwise specified. All dollar estimates are nominal (not adjusted for inflation).

Summary of Findings

Employee Enrollment in Health Insurance

Between 2017 and 2018, there was no significant change in the overall percentage of private-sector employees (47.8 percent in 2018) enrolled in a health insurance plan offered by their employers ("enrollment rate"). There was also no significant change in the enrollment rate in any firm-size category.

The enrollment rate reflects the combination of employers' decisions about offering health insurance and employee eligibility for such coverage, as well as employees' decisions to take up coverage if eligible. Offer rates, eligibility rates, and take-up rates, as well as coverage rates among employees offered insurance, are described further below.

Availability of Coverage: Offer Rates

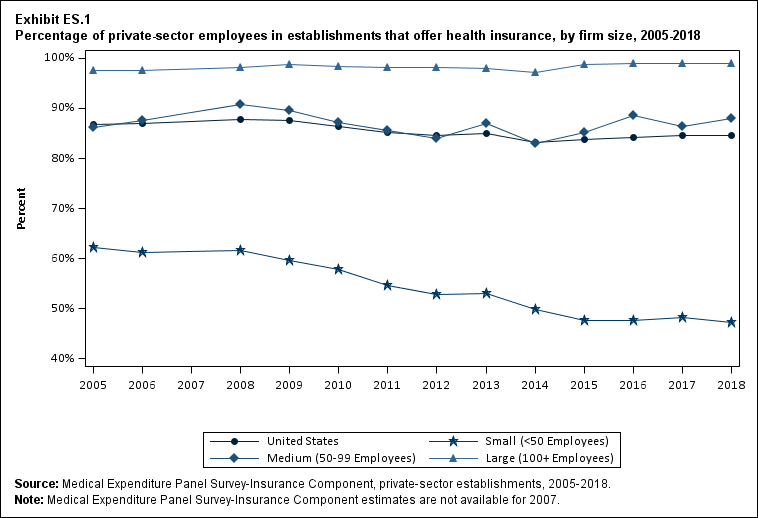

There was no significant change in the overall percentage of employees working at establishments where insurance was offered ("the offer rate") between 2017 (84.5 percent) and 2018 (84.6 percent) (Exhibit ES.1).

In 2018, almost all employees (99.0 percent) in firms with 100 or more employees worked at establishments that offered health insurance. In comparison, about half (47.3 percent) of employees at firms with fewer than 50 employees worked where health insurance was offered.

Return to Table of Contents

Exhibit ES.1 Percentage (standard error) of private-sector employees in establishments that offer health insurance, by firm size, 2005‑2018

| Number of Employees |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| U.S. |

86.9% |

86.9% |

87.7% |

87.6% |

86.5% |

85.3% |

84.7% |

84.9% |

83.2% |

83.8% |

84.3% |

84.5% |

84.6% |

| (Standard Error) |

(0.5%) |

(0.2%) |

(0.3%) |

(0.2%) |

(0.2%) |

(0.2%) |

(0.3%) |

(0.3%) |

(0.3%) |

(0.2%) |

(0.2%) |

(0.2%) |

(0.2%) |

| <50 |

62.2% |

61.2% |

61.6% |

59.6% |

57.8% |

54.7% |

52.9% |

53.1% |

49.8% |

47.6% |

47.7% |

48.3% |

47.3% |

| (Standard Error) |

(0.6%) |

(0.4%) |

(0.5%) |

(0.5%) |

(0.5%) |

(0.4%) |

(0.6%) |

(0.7%) |

(0.6%) |

(0.6%) |

(0.6%) |

(0.6%) |

(0.6%) |

| 50-99 |

86.2% |

87.6% |

90.7% |

89.6% |

87.3% |

85.6% |

84.1% |

87.0% |

83.0% |

85.3% |

88.6% |

86.3% |

88.0% |

| (Standard Error) |

(1.7%) |

(1.2%) |

(0.9%) |

(1.3%) |

(0.9%) |

(1.0%) |

(1.4%) |

(1.0%) |

(1.3%) |

(1.2%) |

(1.0%) |

(1.2%) |

(1.1%) |

| 100+ |

97.5% |

97.7% |

98.2% |

98.8% |

98.5% |

98.1% |

98.2% |

98.0% |

97.3% |

98.8% |

98.9% |

98.9% |

99.0% |

| (Standard Error) |

(0.7%) |

(0.4%) |

(0.3%) |

(0.1%) |

(0.2%) |

(0.2%) |

(0.2%) |

(0.2%) |

(0.2%) |

(0.2%) |

(0.1%) |

(0.2%) |

(0.2%) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

There was no significant change in the offer rate at small employers (fewer than 50 employees) between 2017 (48.3 percent) and 2018 (47.3 percent) (Exhibit ES.1). There was also no significant year-to-year change in offer rates at medium employers (50 to 99 employees) or at large firms (100 or more employees).

Return to Table of Contents

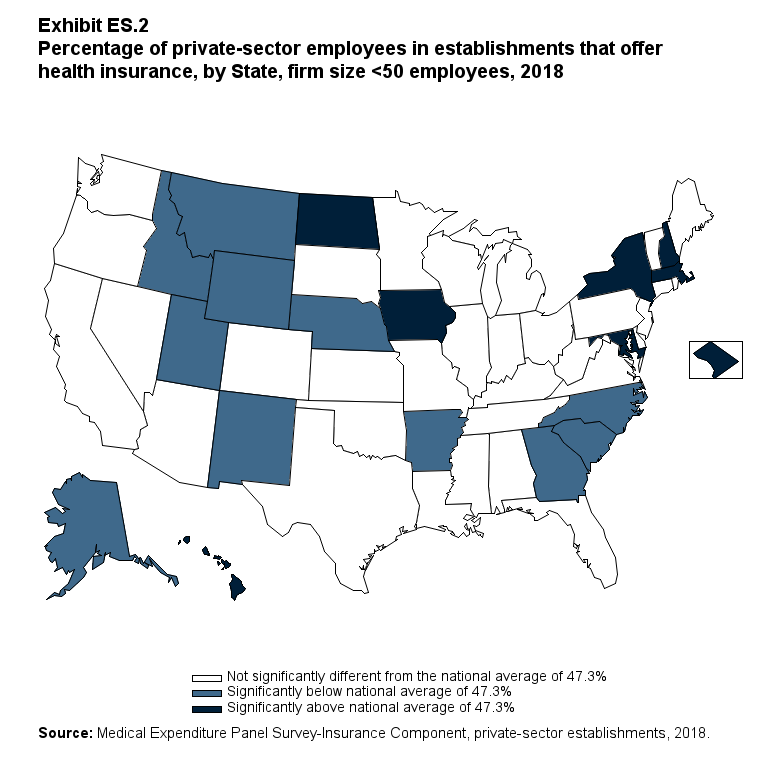

Since almost all large firms offer health insurance coverage, offer rates among small firms are an important factor contributing to overall State ESI offer rates, along with the distribution of employers by firm size in the State. Eight States had small-employer offer rates above the national average (47.3 percent): District of Columbia, Hawaii, Iowa, Maryland, Massachusetts, New Hampshire, New York, and North Dakota (Exhibit ES.2). Eleven States had small-employer offer rates below the national average: Alaska, Arkansas, Georgia, Idaho, Montana, Nebraska, New Mexico, North Carolina, South Carolina, Utah, and Wyoming (Exhibit ES.2).

Exhibit ES.2 Percentage (standard error) of private-sector employees in establishments that offer health insurance, by State, firm size <50 employees, 2018

| Alabama |

53.7% |

Kentucky |

50.7% |

North Dakota |

55.8%* |

| (Standard Error) |

(3.9%) |

(Standard Error) |

(3.9%) |

(Standard Error) |

(3.6%) |

| Alaska |

32.3%* |

Louisiana |

50.2% |

Ohio |

46.1% |

| (Standard Error) |

(3.8%) |

(Standard Error) |

(3.8%) |

(Standard Error) |

(3.5%) |

| Arizona |

50.0% |

Maine |

42.4% |

Oklahoma |

47.1% |

| (Standard Error) |

(3.9%) |

(Standard Error) |

(4.3%) |

(Standard Error) |

(3.9%) |

| Arkansas |

36.9%* |

Maryland |

58.4%* |

Oregon |

47.9% |

| (Standard Error) |

(3.7%) |

(Standard Error) |

(3.9%) |

(Standard Error) |

(3.5%) |

| California |

49.3% |

Massachusetts |

59.1%* |

Pennsylvania |

52.8% |

| (Standard Error) |

(2.0%) |

(Standard Error) |

(3.9%) |

(Standard Error) |

(2.9%) |

| Colorado |

43.4% |

Michigan |

48.9% |

Rhode Island |

53.8% |

| (Standard Error) |

(3.9%) |

(Standard Error) |

(3.8%) |

(Standard Error) |

(4.2%) |

| Connecticut |

53.8% |

Minnesota |

46.4% |

South Carolina |

33.3%* |

| (Standard Error) |

(3.9%) |

(Standard Error) |

(3.8%) |

(Standard Error) |

(3.4%) |

| Delaware |

45.6% |

Mississippi |

45.7% |

South Dakota |

47.2% |

| (Standard Error) |

(4.7%) |

(Standard Error) |

(4.2%) |

(Standard Error) |

(3.4%) |

| District of Columbia |

71.4%* |

Missouri |

47.7% |

Tennessee |

46.0% |

| (Standard Error) |

(4.1%) |

(Standard Error) |

(4.2%) |

(Standard Error) |

(4.1%) |

| Florida |

41.8% |

Montana |

28.9%* |

Texas |

43.1% |

| (Standard Error) |

(3.3%) |

(Standard Error) |

(3.1%) |

(Standard Error) |

(2.8%) |

| Georgia |

38.2%* |

Nebraska |

35.7%* |

Utah |

30.3%* |

| (Standard Error) |

(3.6%) |

(Standard Error) |

(3.7%) |

(Standard Error) |

(3.4%) |

| Hawaii |

87.8%* |

Nevada |

45.3% |

Vermont |

43.6% |

| (Standard Error) |

(2.7%) |

(Standard Error) |

(4.4%) |

(Standard Error) |

(3.5%) |

| Idaho |

35.4%* |

New Hampshire |

54.9%* |

Virginia |

49.4% |

| (Standard Error) |

(3.7%) |

(Standard Error) |

(3.6%) |

(Standard Error) |

(3.6%) |

| Illinois |

46.8% |

New Jersey |

49.1% |

Washington |

50.4% |

| (Standard Error) |

(4.0%) |

(Standard Error) |

(3.1%) |

(Standard Error) |

(3.8%) |

| Indiana |

45.4% |

New Mexico |

39.6%* |

West Virginia |

42.6% |

| (Standard Error) |

(3.6%) |

(Standard Error) |

(3.7%) |

(Standard Error) |

(4.0%) |

| Iowa |

56.3%* |

New York |

56.5%* |

Wisconsin |

41.7% |

| (Standard Error) |

(3.5%) |

(Standard Error) |

(3.0%) |

(Standard Error) |

(3.9%) |

| Kansas |

51.0% |

North Carolina |

32.3%* |

Wyoming |

35.3%* |

| (Standard Error) |

(3.7%) |

(Standard Error) |

(3.3%) |

(Standard Error) |

(3.1%) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2018.

Note: * Statistically different from the national average of 47.3 percent at p < 0.05.

Note that the standard error on the national estimate of 47.3 percent is 0.62 percent.

|

Return to Table of Contents

Employee Coverage, Eligibility, and Take-Up Rates

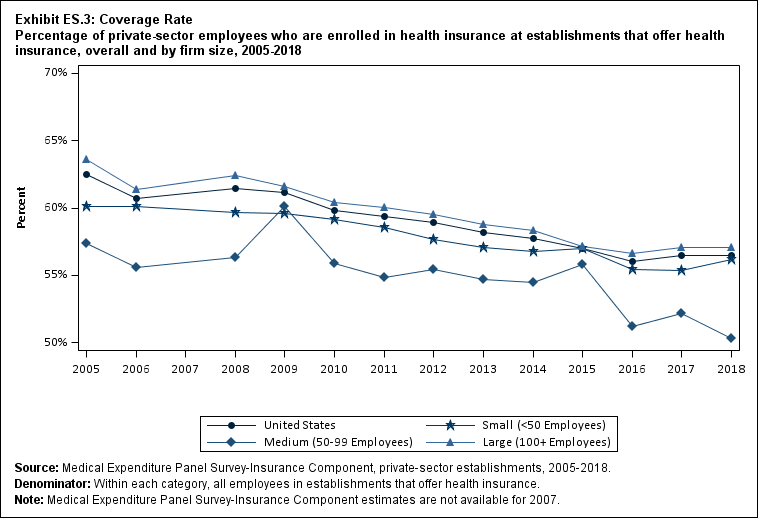

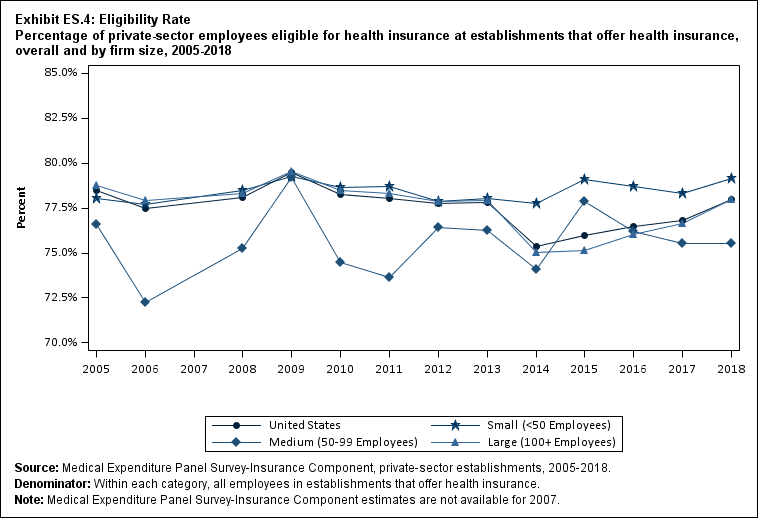

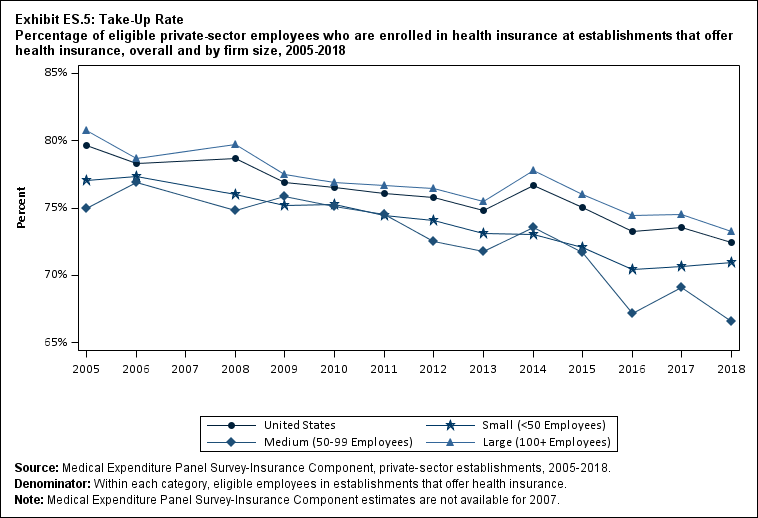

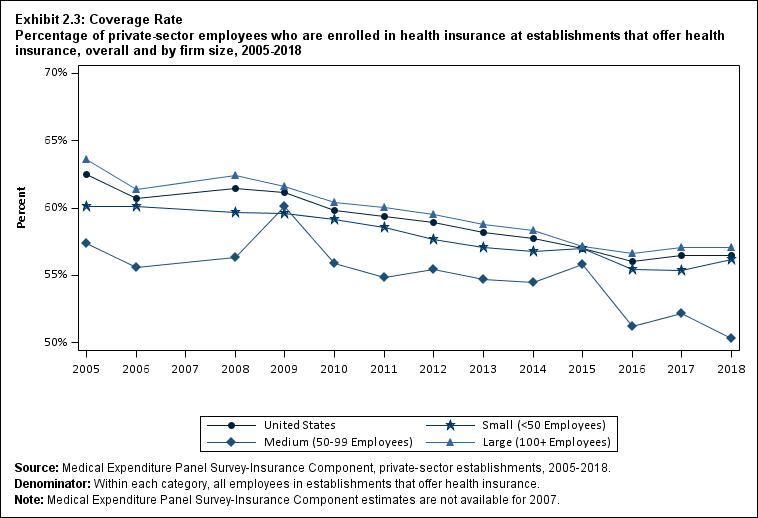

Among establishments that offered insurance, 56.5 percent of employees were enrolled in coverage through their employer (the "coverage rate") and 78.0 percent were eligible for health insurance (the "eligibility rate"). Among eligible employees, 72.4 percent were enrolled in their employer's health insurance (the "take-up rate") (Exhibits ES.3, ES.4, and ES.5).

There was no significant change in the coverage rate between 2017 and 2018 overall or in any firm-size category (Exhibit ES.3).

Exhibit ES.3: Coverage Rate Percentage (standard error) of private-sector employees who are enrolled in health insurance at establishments that offer health insurance, overall and by firm size, 2005‑2018

| Number of Employees |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| U.S. |

62.5% |

60.7% |

61.4% |

61.1% |

59.8% |

59.4% |

58.9% |

58.2% |

57.8% |

57.0% |

56.0% |

56.5% |

56.5% |

| (Standard Error) |

(0.4%) |

(0.3%) |

(0.4%) |

(0.4%) |

(0.5%) |

(0.2%) |

(0.4%) |

(0.3%) |

(0.4%) |

(0.4%) |

(0.4%) |

(0.4%) |

(0.4%) |

| <50 |

60.1% |

60.1% |

59.7% |

59.6% |

59.2% |

58.6% |

57.7% |

57.1% |

56.8% |

57.0% |

55.5% |

55.4% |

56.2% |

| (Standard Error) |

(0.5%) |

(0.6%) |

(0.2%) |

(0.4%) |

(0.6%) |

(0.5%) |

(0.5%) |

(0.5%) |

(0.6%) |

(0.6%) |

(0.6%) |

(0.6%) |

(0.6%) |

| 50-99 |

57.4% |

55.6% |

56.3% |

60.1% |

55.9% |

54.9% |

55.4% |

54.7% |

54.5% |

55.8% |

51.2% |

52.2% |

50.3% |

| (Standard Error) |

(1.5%) |

(1.6%) |

(1.0%) |

(1.0%) |

(0.8%) |

(1.0%) |

(1.2%) |

(0.8%) |

(1.3%) |

(1.2%) |

(1.2%) |

(1.2%) |

(1.2%) |

| 100+ |

63.6% |

61.4% |

62.4% |

61.6% |

60.4% |

60.0% |

59.5% |

58.8% |

58.3% |

57.1% |

56.6% |

57.1% |

57.1% |

| (Standard Error) |

(0.6%) |

(0.5%) |

(0.5%) |

(0.6%) |

(0.6%) |

(0.3%) |

(0.4%) |

(0.3%) |

(0.5%) |

(0.5%) |

(0.5%) |

(0.5%) |

(0.5%) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Denominator: Within each category, all employees in establishments that offer health insurance.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

Return to Table of Contents

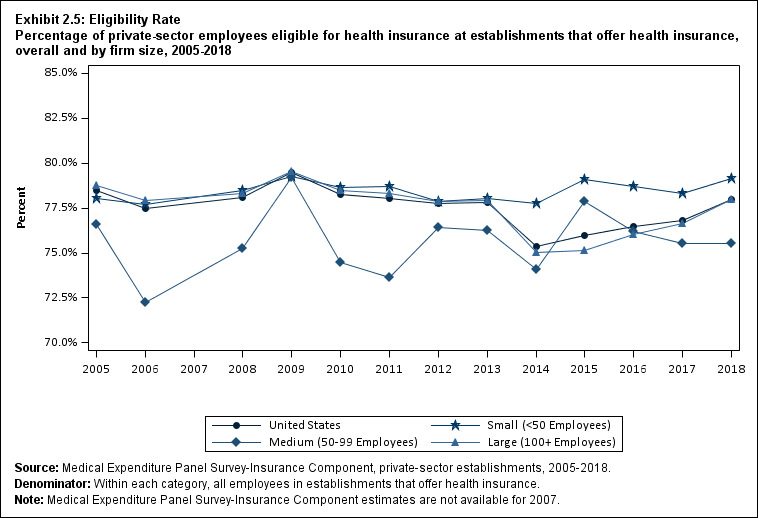

Among employees in establishments that offered health insurance, the eligibility rate increased from 76.8 percent in 2017 to 78.0 percent in 2018 (Exhibit ES.4). The rate in 2018 was higher than eligibility rates observed from 2014 to 2017.

Exhibit ES.4: Eligibility Rate Percentage (standard error) of private-sector employees eligible for health insurance at establishments that offer health insurance, overall and by firm size, 2005‑2018

| Number of Employees |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| U.S. |

78.5% |

77.5% |

78.1% |

79.5% |

78.2% |

78.0% |

77.8% |

77.8% |

75.4% |

76.0% |

76.5% |

76.8% |

78.0% |

| (Standard Error) |

(0.5%) |

(0.4%) |

(0.4%) |

(0.3%) |

(0.5%) |

(0.4%) |

(0.3%) |

(0.2%) |

(0.4%) |

(0.4%) |

(0.4%) |

(0.4%) |

(0.4%) |

| <50 |

78.0% |

77.7% |

78.5% |

79.3% |

78.6% |

78.7% |

77.9% |

78.0% |

77.7% |

79.1% |

78.7% |

78.3% |

79.1% |

| (Standard Error) |

(0.7%) |

(0.6%) |

(0.4%) |

(0.5%) |

(0.5%) |

(0.6%) |

(0.5%) |

(0.4%) |

(0.6%) |

(0.6%) |

(0.6%) |

(0.6%) |

(0.6%) |

| 50-99 |

76.6% |

72.3% |

75.3% |

79.2% |

74.5% |

73.6% |

76.4% |

76.2% |

74.1% |

77.8% |

76.2% |

75.5% |

75.6% |

| (Standard Error) |

(1.4%) |

(1.5%) |

(1.3%) |

(0.8%) |

(0.6%) |

(1.0%) |

(1.2%) |

(0.8%) |

(1.4%) |

(1.2%) |

(1.2%) |

(1.2%) |

(1.2%) |

| 100+ |

78.8% |

77.9% |

78.3% |

79.6% |

78.5% |

78.3% |

77.9% |

77.9% |

75.0% |

75.2% |

76.0% |

76.6% |

78.0% |

| (Standard Error) |

(0.6%) |

(0.6%) |

(0.4%) |

(0.5%) |

(0.6%) |

(0.4%) |

(0.3%) |

(0.3%) |

(0.5%) |

(0.5%) |

(0.4%) |

(0.5%) |

(0.5%) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Denominator: Within each category, all employees in establishments that offer health insurance.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

Return to Table of Contents

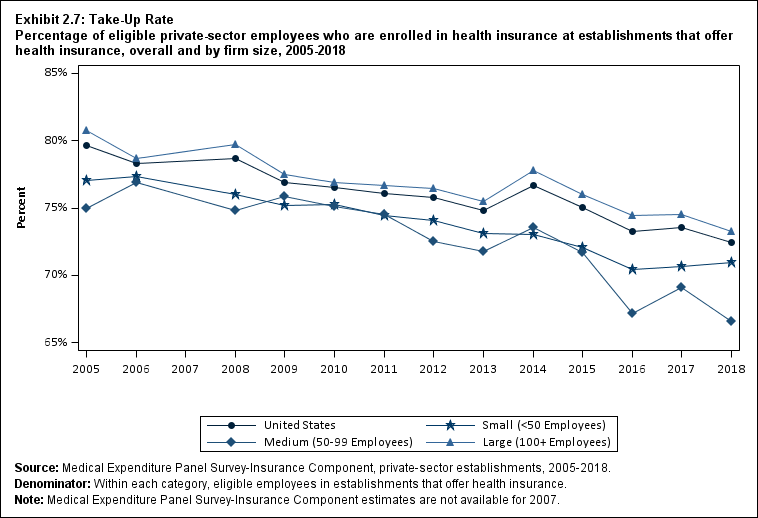

The take-up rate declined from 73.5 percent to 72.4 percent between 2017 and 2018 (Exhibit ES.5). The rate in 2018 was significantly lower than take-up rates in almost all years in the 2005 to 2017 period.

Exhibit ES.5: Take-Up Rate Percentage (standard error) of eligible private-sector employees who are enrolled in health insurance at establishments that offer health insurance, overall and by firm size, 2005‑2018

| Number of Employees |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| U.S. |

79.6% |

78.3% |

78.7% |

76.9% |

76.5% |

76.1% |

75.8% |

74.8% |

76.7% |

75.0% |

73.3% |

73.5% |

72.4% |

| (Standard Error) |

(0.3%) |

(0.3%) |

(0.3%) |

(0.3%) |

(0.2%) |

(0.3%) |

(0.3%) |

(0.2%) |

(0.3%) |

(0.3%) |

(0.3%) |

(0.3%) |

(0.4%) |

| <50 |

77.0% |

77.4% |

76.0% |

75.2% |

75.3% |

74.4% |

74.1% |

73.1% |

73.0% |

72.1% |

70.4% |

70.7% |

71.0% |

| (Standard Error) |

(0.6%) |

(0.7%) |

(0.3%) |

(0.3%) |

(0.6%) |

(0.4%) |

(0.4%) |

(0.6%) |

(0.5%) |

(0.5%) |

(0.5%) |

(0.6%) |

(0.6%) |

| 50-99 |

74.9% |

76.9% |

74.9% |

75.9% |

75.1% |

74.5% |

72.5% |

71.8% |

73.5% |

71.7% |

67.2% |

69.1% |

66.6% |

| (Standard Error) |

(1.2%) |

(1.3%) |

(0.5%) |

(0.9%) |

(0.7%) |

(0.6%) |

(0.8%) |

(1.0%) |

(1.0%) |

(1.1%) |

(1.2%) |

(1.1%) |

(1.1%) |

| 100+ |

80.7% |

78.7% |

79.7% |

77.5% |

76.9% |

76.7% |

76.4% |

75.5% |

77.8% |

76.0% |

74.4% |

74.5% |

73.3% |

| (Standard Error) |

(0.5%) |

(0.4%) |

(0.4%) |

(0.5%) |

(0.3%) |

(0.3%) |

(0.4%) |

(0.3%) |

(0.3%) |

(0.3%) |

(0.4%) |

(0.4%) |

(0.4%) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Denominator: Within each category, eligible employees in establishments that offer health insurance.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

Return to Table of Contents

Choice of Plans

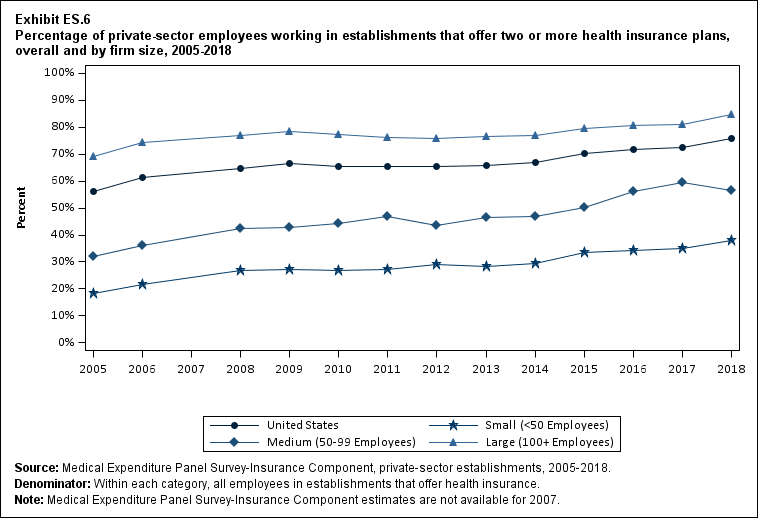

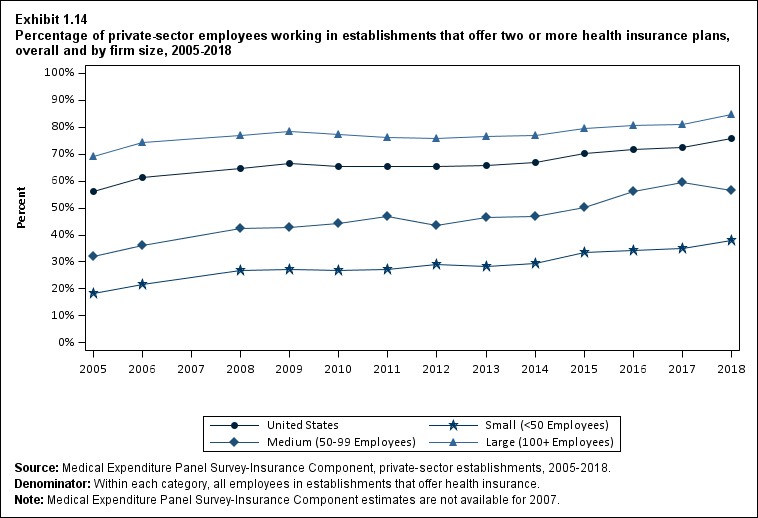

The percentage of employees with a choice of plans increased between 2017 and 2018, from 72.4 percent in 2017 to 75.7 percent in 2018. The availability of plan choice was significantly higher in 2018 than in 2005 for small employers (37.8 percent vs. 18.2 percent),

medium employers (56.4 percent vs. 32.1 percent), and large employers (84.7 percent vs. 69.0 percent) (Exhibit ES.6).

Exhibit ES.6 Percentage (standard error) of private-sector employees working in establishments that offer two or more health insurance plans, overall and by firm size, 2005‑2018

| Number of Employees |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| U.S. |

56.3% |

61.4% |

64.8% |

66.5% |

65.6% |

65.5% |

65.3% |

66.0% |

67.0% |

70.2% |

71.7% |

72.4% |

75.7% |

| (Standard Error) |

(0.8%) |

(0.7%) |

(0.6%) |

(0.7%) |

(0.8%) |

(0.5%) |

(0.7%) |

(0.6%) |

(0.6%) |

(0.5%) |

(0.5%) |

(0.5%) |

(0.5%) |

| <50 |

18.2% |

21.5% |

26.8% |

27.3% |

26.7% |

27.2% |

29.3% |

28.4% |

29.6% |

33.6% |

34.2% |

34.9% |

37.8% |

| (Standard Error) |

(1.1%) |

(1.1%) |

(0.7%) |

(0.9%) |

(0.8%) |

(0.9%) |

(0.8%) |

(1.0%) |

(0.9%) |

(1.1%) |

(1.0%) |

(1.0%) |

(1.0%) |

| 50-99 |

32.1% |

36.0% |

42.5% |

42.8% |

44.1% |

46.8% |

43.7% |

46.6% |

46.8% |

50.2% |

56.2% |

59.3% |

56.4% |

| (Standard Error) |

(2.5%) |

(2.4%) |

(1.7%) |

(2.0%) |

(1.9%) |

(2.2%) |

(1.7%) |

(2.2%) |

(2.1%) |

(2.2%) |

(2.0%) |

(1.9%) |

(1.9%) |

| 100+ |

69.0% |

74.3% |

76.9% |

78.5% |

77.3% |

76.3% |

75.7% |

76.5% |

77.0% |

79.7% |

80.7% |

81.0% |

84.7% |

| (Standard Error) |

(0.9%) |

(0.6%) |

(0.7%) |

(0.7%) |

(1.0%) |

(0.7%) |

(0.7%) |

(0.7%) |

(0.6%) |

(0.6%) |

(0.6%) |

(0.6%) |

(0.5%) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Denominator: Within each category, all employees in establishments that offer health insurance.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

Return to Table of Contents

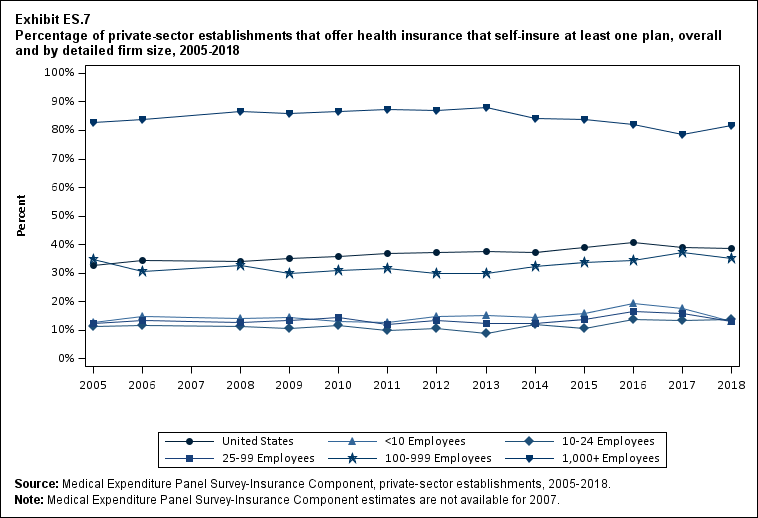

Self-Insured Plans

Between 2017 and 2018, there was no significant change in the percentage of offering establishments that self-insured at least one plan overall. However, this percentage declined at establishments in firms with fewer than 10 employees (from 17.7 percent to 13.1 percent) and with 25 to 99 employees (from 16.0 percent to 12.9 percent) and increased at

establishments in firms with 1,000 or more employees (from 78.6 percent to 81.6 percent) (Exhibit ES.7).

Exhibit ES.7 Percentage (standard error) of private-sector establishments that offer health insurance that self-insure at least one plan, overall and by detailed firm size, 2005‑2018

| Number of Employees |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| U.S. |

32.7% |

34.4% |

34.2% |

35.1% |

35.8% |

36.9% |

37.2% |

37.6% |

37.2% |

39.0% |

40.7% |

39.2% |

38.7% |

| (Standard Error) |

(0.5%) |

(0.5%) |

(0.4%) |

(0.4%) |

(0.5%) |

(0.5%) |

(0.5%) |

(0.5%) |

(0.5%) |

(0.5%) |

(0.6%) |

(0.6%) |

(0.6%) |

| <10 |

12.7% |

14.9% |

14.0% |

14.6% |

13.1% |

12.6% |

14.9% |

15.2% |

14.4% |

15.8% |

19.3% |

17.7% |

13.1% |

| (Standard Error) |

(0.8%) |

(0.9%) |

(0.8%) |

(0.7%) |

(0.5%) |

(0.8%) |

(0.9%) |

(0.4%) |

(0.8%) |

(1.0%) |

(1.4%) |

(1.4%) |

(1.1%) |

| 10-24 |

11.2% |

11.6% |

11.1% |

10.4% |

11.6% |

9.9% |

10.7% |

9.0% |

12.0% |

10.6% |

13.6% |

13.3% |

13.8% |

| (Standard Error) |

(0.5%) |

(0.6%) |

(0.9%) |

(0.4%) |

(0.8%) |

(0.7%) |

(0.7%) |

(0.7%) |

(1.0%) |

(1.0%) |

(1.1%) |

(1.2%) |

(1.2%) |

| 25-99 |

12.2% |

13.5% |

12.6% |

13.4% |

14.3% |

12.2% |

13.5% |

12.4% |

12.2% |

13.7% |

16.6% |

16.0% |

12.9% |

| (Standard Error) |

(0.9%) |

(0.7%) |

(0.8%) |

(0.7%) |

(0.7%) |

(0.7%) |

(0.7%) |

(0.7%) |

(0.8%) |

(0.9%) |

(0.9%) |

(0.9%) |

(0.8%) |

| 100-999 |

34.9% |

30.6% |

32.7% |

29.9% |

30.9% |

31.7% |

30.1% |

30.1% |

32.5% |

33.7% |

34.4% |

37.2% |

35.1% |

| (Standard Error) |

(1.4%) |

(0.9%) |

(1.3%) |

(0.7%) |

(0.9%) |

(1.1%) |

(0.8%) |

(1.0%) |

(1.2%) |

(1.2%) |

(1.2%) |

(1.3%) |

(1.2%) |

| 1,000+ |

82.7% |

83.8% |

86.5% |

85.8% |

86.6% |

87.5% |

87.1% |

88.0% |

84.2% |

83.8% |

81.9% |

78.6% |

81.6% |

| (Standard Error) |

(0.5%) |

(0.7%) |

(0.5%) |

(0.4%) |

(0.6%) |

(0.5%) |

(0.7%) |

(0.5%) |

(0.8%) |

(0.8%) |

(0.8%) |

(0.8%) |

(0.8%) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

Return to Table of Contents

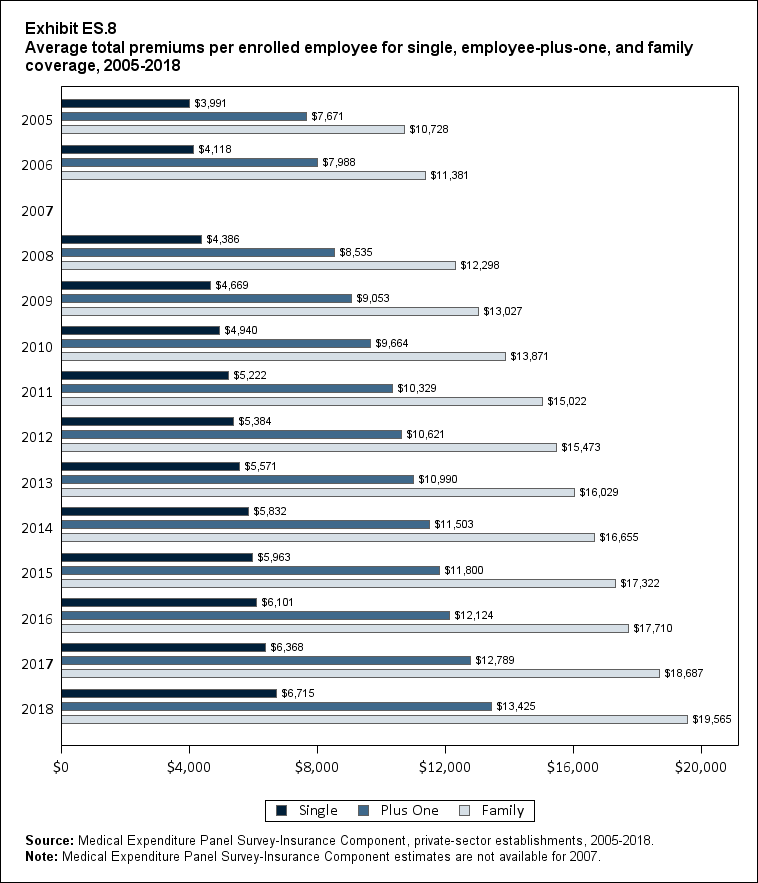

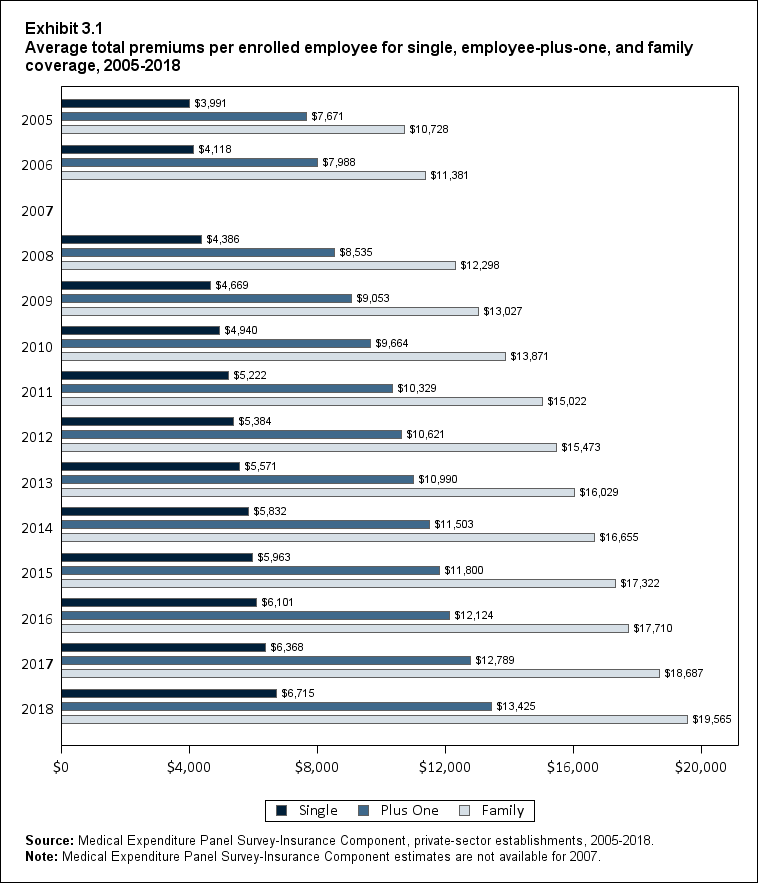

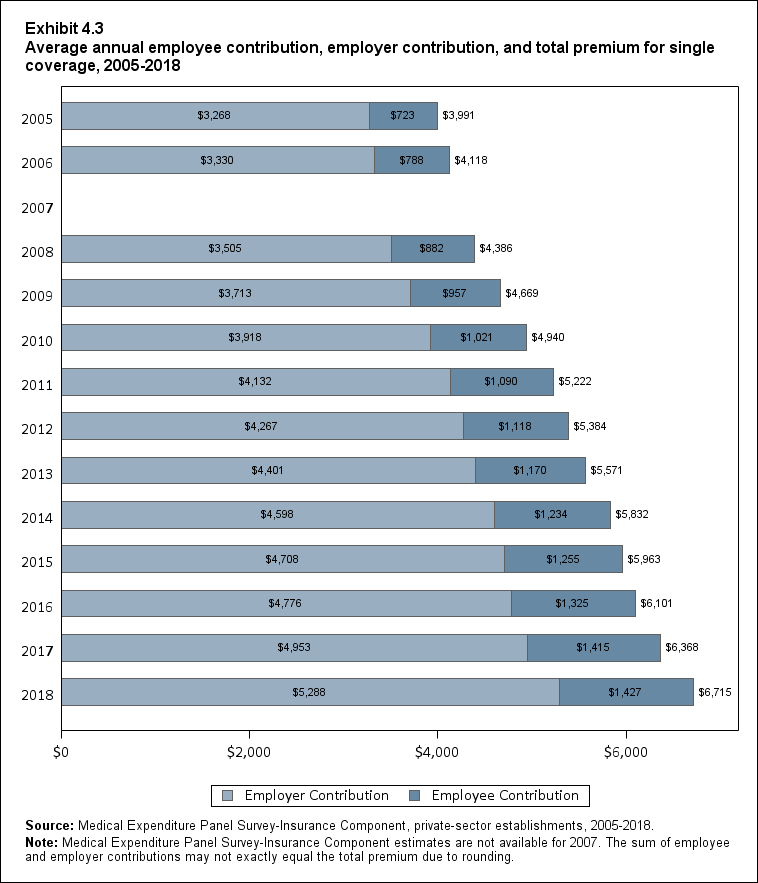

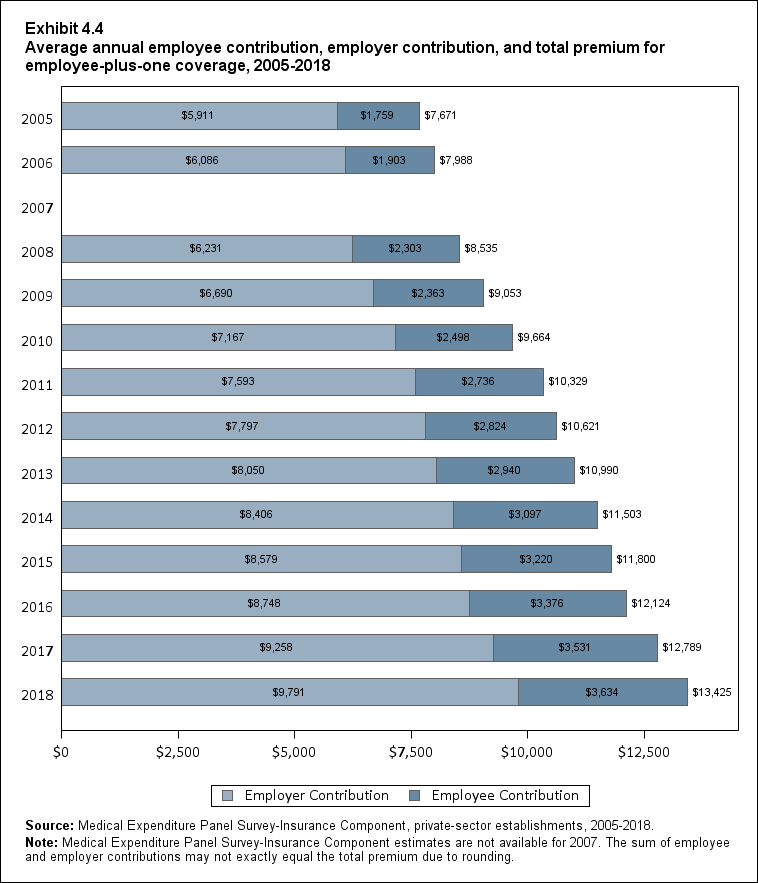

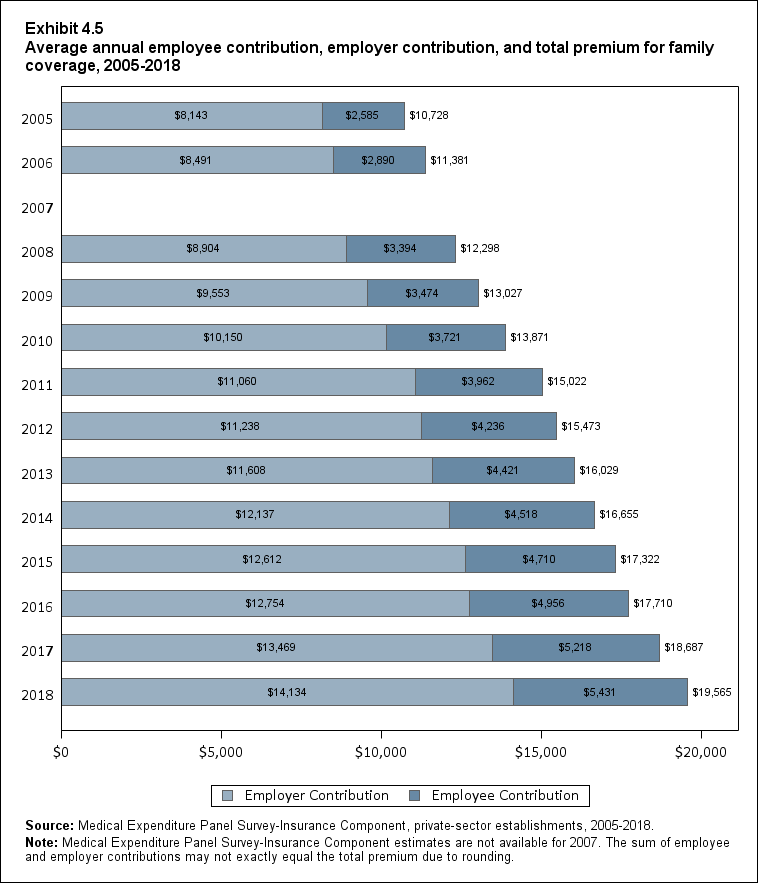

Premiums

In 2018, average annual health insurance premiums per enrolled employee with private-sector employer coverage were $6,715 for single coverage, $13,425 for employee-plus-one coverage, and $19,565 for family coverage. These amounts represent increases of 5.4 percent for single coverage, 5.0 percent for employee-plus-one coverage, and 4.7 percent for family coverage over 2017 levels (Exhibit ES.8). Between 2005 and 2018, premiums for the three types of coverage grew by

between 68.3 percent and 82.4 percent, with average annual growth rates between 4.1 percent and 4.7 percent (data not shown).

Exhibit ES.8 Average total premiums (standard error) per enrolled employee for single, employee-plus-one and family coverage, 2005‑2018

| Coverage |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| Single |

$3,991 |

$4,118 |

$4,386 |

$4,669 |

$4,940 |

$5,222 |

$5,384 |

$5,571 |

$5,832 |

$5,963 |

$6,101 |

$6,368 |

$6,715 |

| (Standard Error) |

($24) |

($25) |

($15) |

($21) |

($22) |

($26) |

($28) |

($23) |

($25) |

($26) |

($27) |

($28) |

($31) |

| Plus One |

$7,671 |

$7,988 |

$8,535 |

$9,053 |

$9,664 |

$10,329 |

$10,621 |

$10,990 |

$11,503 |

$11,800 |

$12,124 |

$12,789 |

$13,425 |

| (Standard Error) |

($44) |

($48) |

($43) |

($34) |

($60) |

($105) |

($56) |

($54) |

($60) |

($58) |

($60) |

($70) |

($70) |

| Family |

$10,728 |

$11,381 |

$12,298 |

$13,027 |

$13,871 |

$15,022 |

$15,473 |

$16,029 |

$16,655 |

$17,322 |

$17,710 |

$18,687 |

$19,565 |

| (Standard Error) |

($41) |

($32) |

($81) |

($25) |

($75) |

($98) |

($95) |

($61) |

($79) |

($95) |

($84) |

($105) |

($104) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

Return to Table of Contents

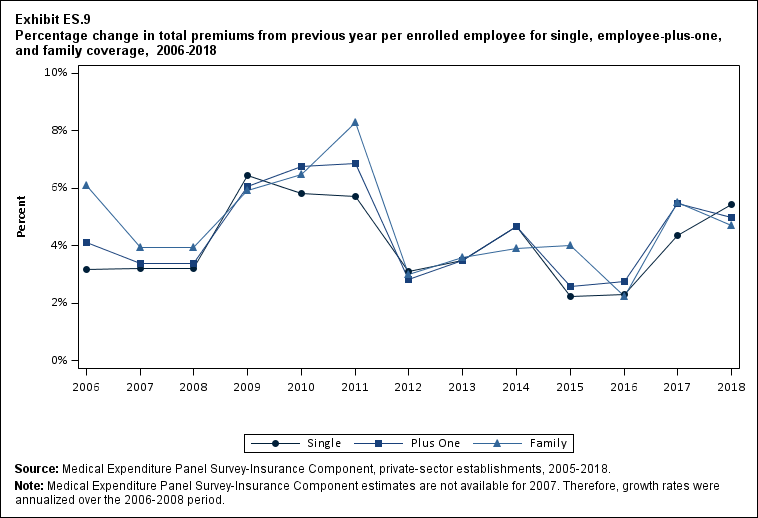

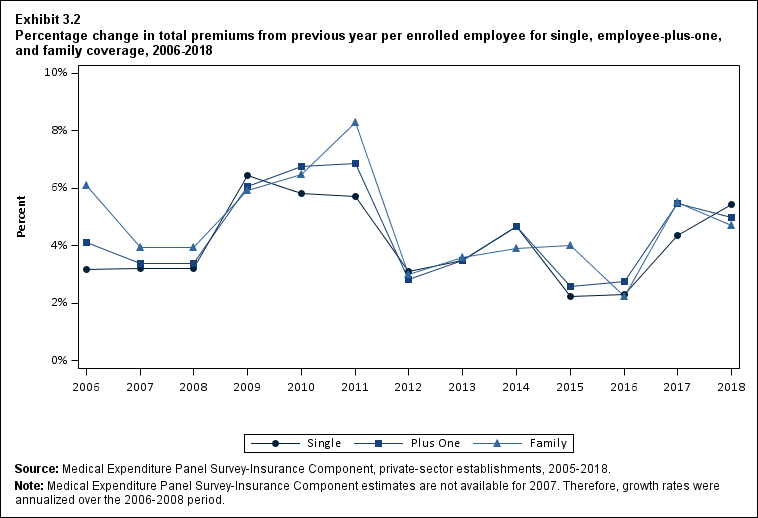

There were no significant differences between the 2017 to 2018 and the 2016 to 2017 premium growth rates for single coverage (5.4 percent vs. 4.4 percent), employee-plus-one coverage (5.0 percent vs. 5.5 percent), or family coverage (4.7 percent vs. 5.5 percent). In the 13 years from 2005 to 2018, annual premium growth rates ranged from 2.2 percent to 8.3 percent for family coverage, from 2.6 percent to 6.9 percent for employee-plus-one coverage, and from 2.2 percent to 6.5 percent for single coverage (Exhibit ES.9).

Exhibit ES.9 Percentage change (standard error) in total premiums from previous year per enrolled employee for single, employee-plus-one, and family coverage, 2006‑2018

| Year |

Single |

Employee-Plus-One |

Family |

| 2006 |

3.2% |

4.1% |

6.1% |

| (Standard Error) |

(0.9%) |

(0.9%) |

(0.5%) |

| 2007 |

3.2% |

3.4% |

4.0% |

| (Standard Error) |

(0.8%) |

(0.8%) |

(0.8%) |

| 2008 |

3.2% |

3.4% |

4.0% |

| (Standard Error) |

(0.8%) |

(0.8%) |

(0.8%) |

| 2009 |

6.5% |

6.1% |

5.9% |

| (Standard Error) |

(0.6%) |

(0.7%) |

(0.7%) |

| 2010 |

5.8% |

6.7% |

6.5% |

| (Standard Error) |

(0.7%) |

(0.8%) |

(0.6%) |

| 2011 |

5.7% |

6.9% |

8.3% |

| (Standard Error) |

(0.7%) |

(1.3%) |

(0.9%) |

| 2012 |

3.1% |

2.8% |

3.0% |

| (Standard Error) |

(0.7%) |

(1.2%) |

(0.9%) |

| 2013 |

3.5% |

3.5% |

3.6% |

| (Standard Error) |

(0.7%) |

(0.7%) |

(0.7%) |

| 2014 |

4.7% |

4.7% |

3.9% |

| (Standard Error) |

(0.6%) |

(0.7%) |

(0.6%) |

| 2015 |

2.2% |

2.6% |

4.0% |

| (Standard Error) |

(0.6%) |

(0.7%) |

(0.8%) |

| 2016 |

2.3% |

2.7% |

2.2% |

| (Standard Error) |

(0.6%) |

(0.7%) |

(0.7%) |

| 2017 |

4.4% |

5.5% |

5.5% |

| (Standard Error) |

(0.7%) |

(0.8%) |

(0.8%) |

| 2018 |

5.4% |

5.0% |

4.7% |

| (Standard Error) |

(0.7%) |

(0.8%) |

(0.8%) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

Therefore, growth rates were annualized over the 2006‑2008 period.

|

Return to Table of Contents

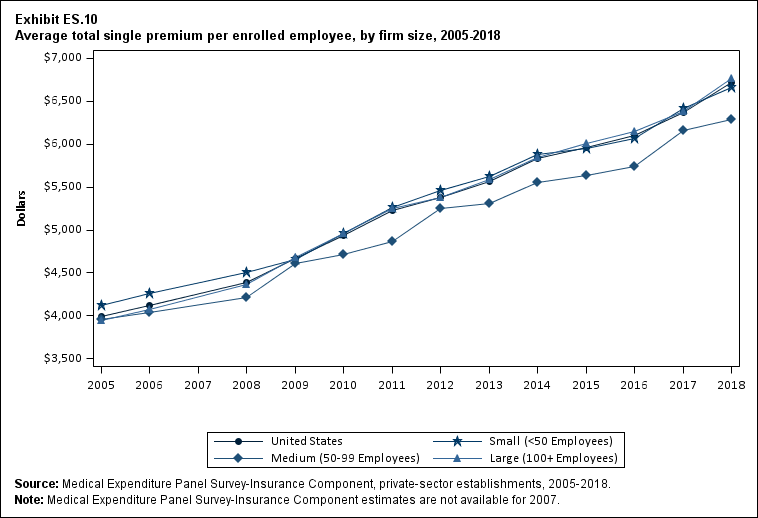

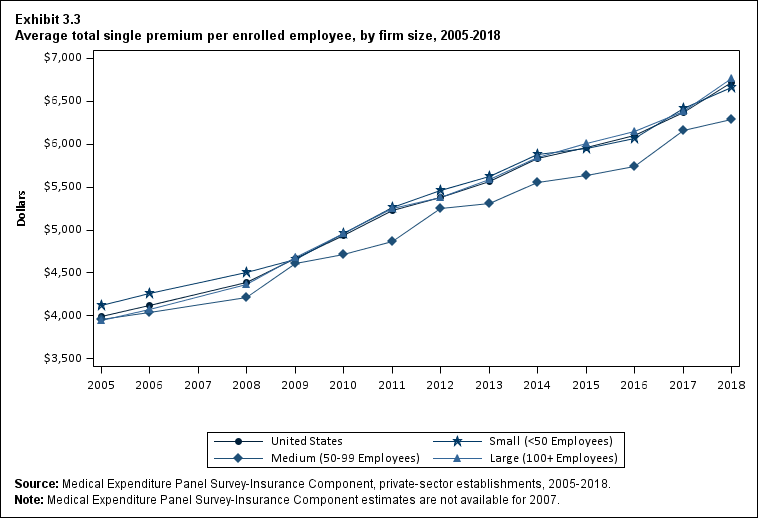

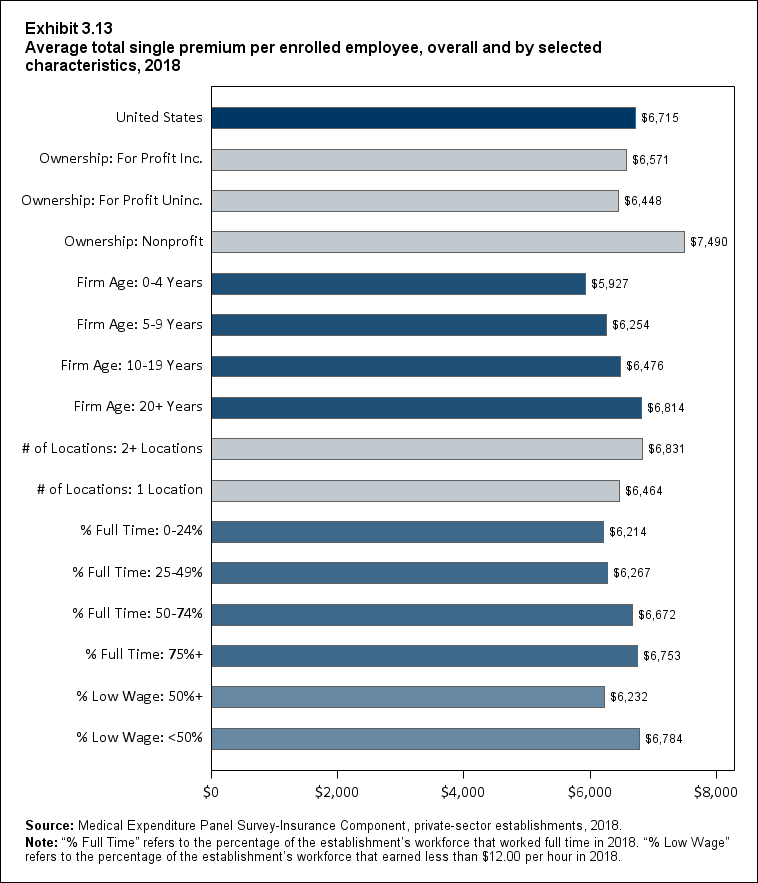

In 2018, average single premiums were lower in medium firms ($6,287) than in small ($6,667) or large firms ($6,770) (Exhibit ES.10).

Exhibit ES.10 Average total single premium (standard error) per enrolled employee, by firm size, 2005‑2018

| Number of Employees |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| U.S. |

$3,991 |

$4,118 |

$4,386 |

$4,669 |

$4,940 |

$5,222 |

$5,384 |

$5,571 |

$5,832 |

$5,963 |

$6,101 |

$6,368 |

$6,715 |

| (Standard Error) |

($24) |

($25) |

($15) |

($21) |

($22) |

($26) |

($28) |

($23) |

($25) |

($26) |

($27) |

($28) |

($31) |

| <50 |

$4,121 |

$4,260 |

$4,501 |

$4,652 |

$4,956 |

$5,258 |

$5,460 |

$5,628 |

$5,886 |

$5,947 |

$6,070 |

$6,421 |

$6,667 |

| (Standard Error) |

($45) |

($34) |

($31) |

($31) |

($34) |

($39) |

($60) |

($39) |

($55) |

($55) |

($53) |

($61) |

($63) |

| 50-99 |

$3,962 |

$4,045 |

$4,215 |

$4,614 |

$4,713 |

$4,861 |

$5,246 |

$5,314 |

$5,549 |

$5,642 |

$5,743 |

$6,163 |

$6,287 |

| (Standard Error) |

($70) |

($66) |

($37) |

($82) |

($52) |

($75) |

($39) |

($73) |

($82) |

($104) |

($96) |

($121) |

($111) |

| 100+ |

$3,950 |

$4,080 |

$4,370 |

$4,681 |

$4,959 |

$5,252 |

$5,378 |

$5,584 |

$5,851 |

$6,006 |

$6,146 |

$6,377 |

$6,770 |

| (Standard Error) |

($32) |

($32) |

($26) |

($38) |

($23) |

($31) |

($28) |

($29) |

($30) |

($31) |

($32) |

($33) |

($37) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

Return to Table of Contents

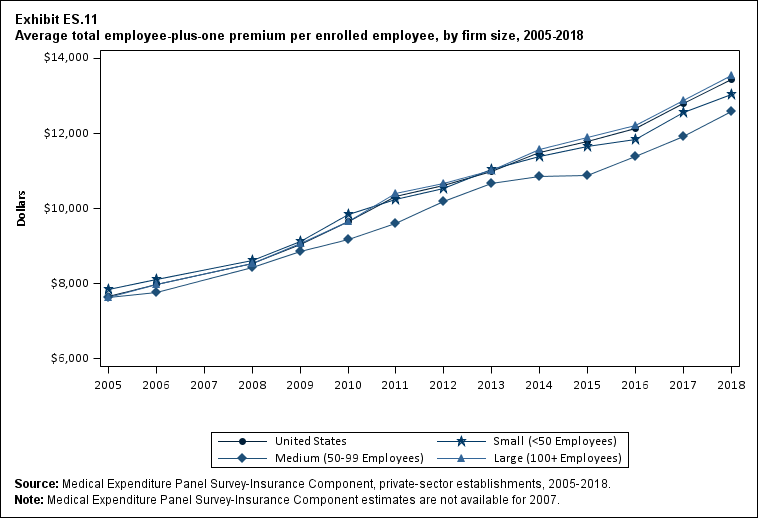

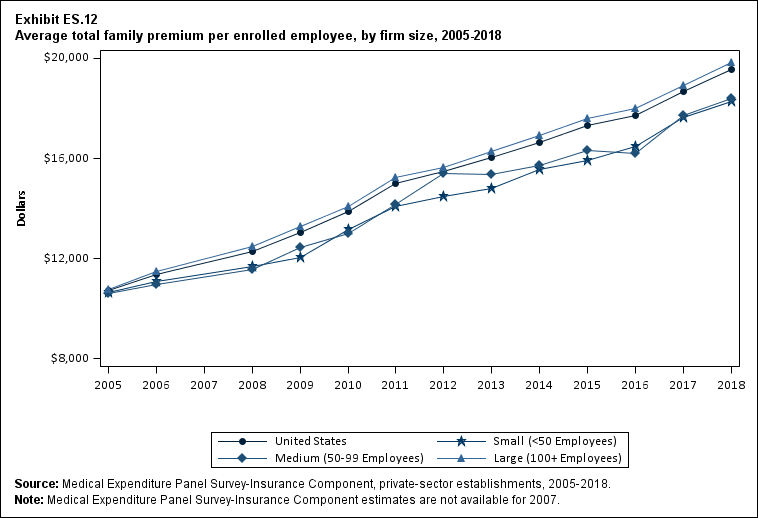

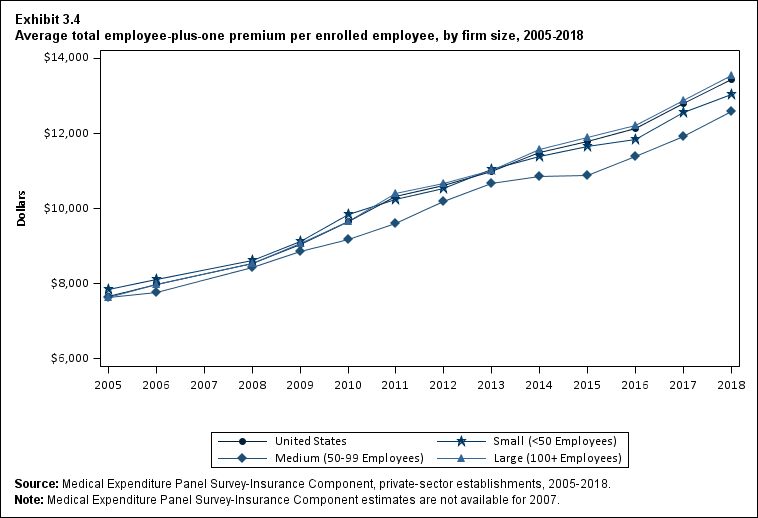

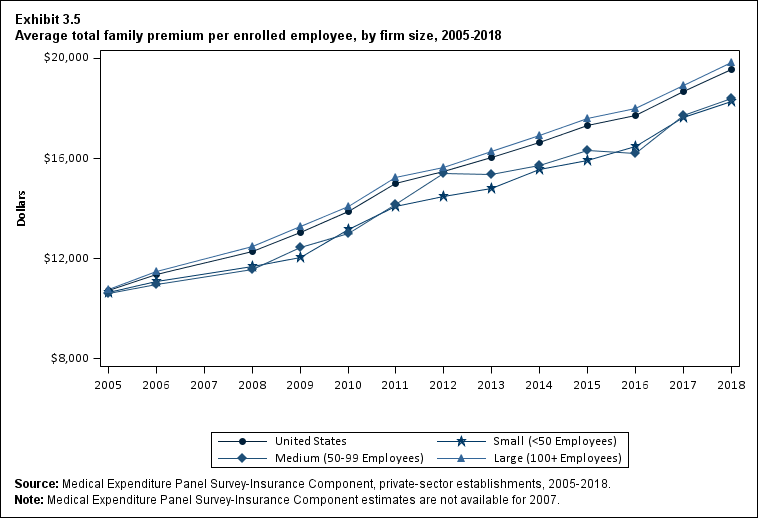

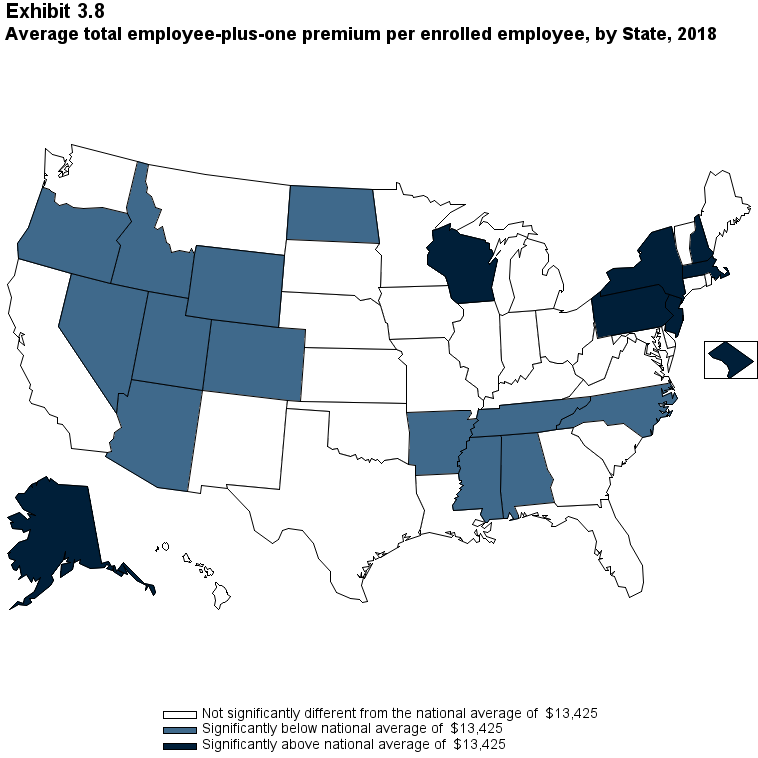

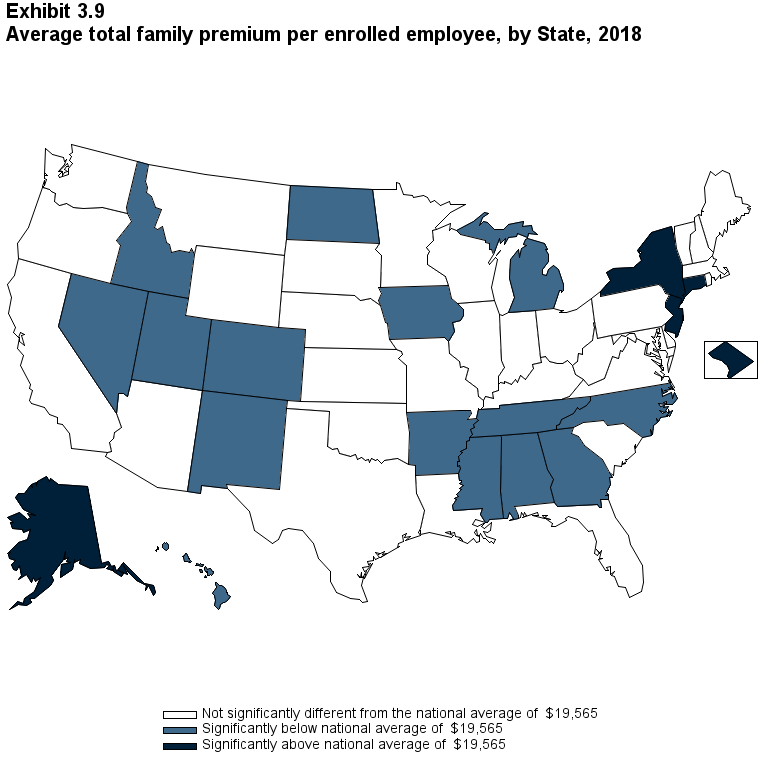

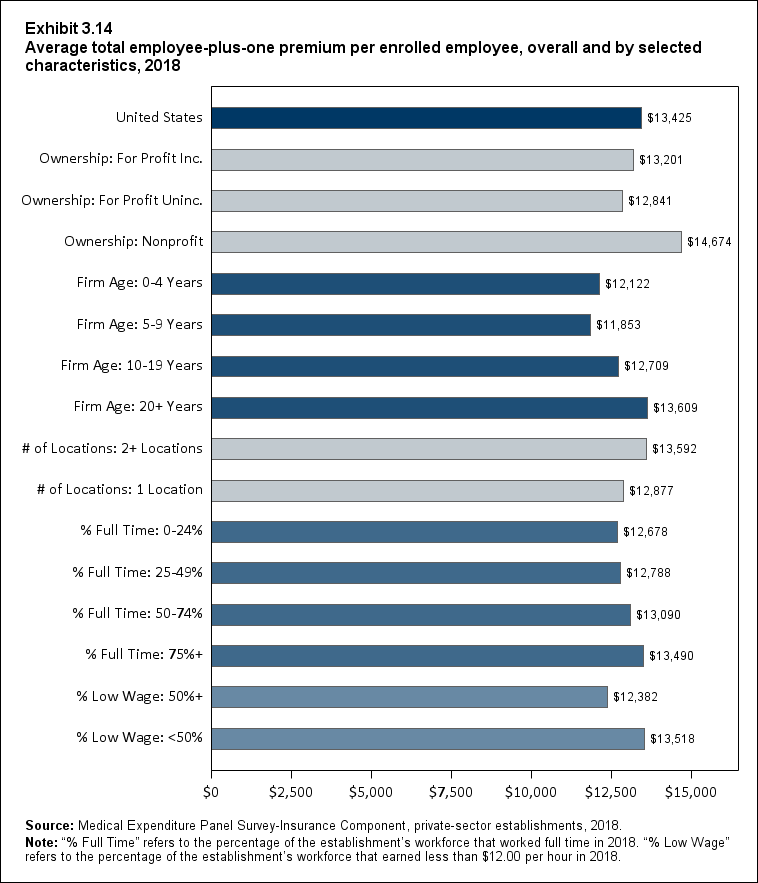

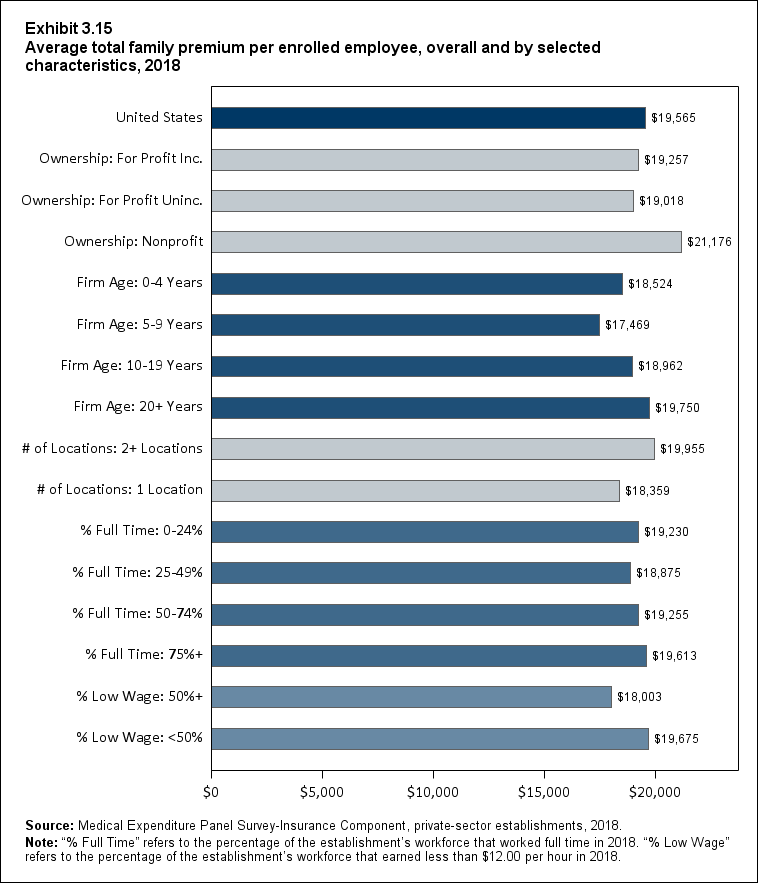

Premiums for dependent coverage were highest in large firms in 2018. Specifically, premiums were higher in large firms than in medium and small firms for employee-plus-one coverage ($13,537 vs. $12,593 and $13,044, respectively) and family coverage ($19,824 vs. $18,386 and $18,296, respectively) (Exhibits ES.11 and ES.12).

Exhibit ES.11 Average total employee-plus-one premium (standard error) per enrolled employee, by firm size, 2005‑2018

| Number of Employees |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| U.S. |

$7,671 |

$7,988 |

$8,535 |

$9,053 |

$9,664 |

$10,329 |

$10,621 |

$10,990 |

$11,503 |

$11,800 |

$12,124 |

$12,789 |

$13,425 |

| (Standard Error) |

($44) |

($48) |

($43) |

($34) |

($60) |

($105) |

($56) |

($54) |

($60) |

($58) |

($60) |

($70) |

($70) |

| <50 |

$7,841 |

$8,105 |

$8,631 |

$9,124 |

$9,850 |

$10,253 |

$10,524 |

$11,050 |

$11,386 |

$11,666 |

$11,833 |

$12,558 |

$13,044 |

| (Standard Error) |

($115) |

($113) |

($110) |

($119) |

($80) |

($104) |

($121) |

($92) |

($163) |

($158) |

($156) |

($170) |

($176) |

| 50-99 |

$7,645 |

$7,774 |

$8,421 |

$8,852 |

$9,166 |

$9,615 |

$10,178 |

$10,673 |

$10,845 |

$10,885 |

$11,389 |

$11,931 |

$12,593 |

| (Standard Error) |

($138) |

($167) |

($88) |

($148) |

($124) |

($192) |

($185) |

($330) |

($187) |

($198) |

($227) |

($232) |

($236) |

| 100+ |

$7,640 |

$7,981 |

$8,527 |

$9,058 |

$9,669 |

$10,394 |

$10,672 |

$11,006 |

$11,571 |

$11,892 |

$12,225 |

$12,878 |

$13,537 |

| (Standard Error) |

($60) |

($61) |

($60) |

($34) |

($62) |

($113) |

($70) |

($59) |

($68) |

($66) |

($68) |

($79) |

($79) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

Return to Table of Contents

Exhibit ES.12 Average total family premium (standard error) per enrolled employee, by firm size, 2005‑2018

| Number of Employees |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| U.S. |

$10,728 |

$11,381 |

$12,298 |

$13,027 |

$13,871 |

$15,022 |

$15,473 |

$16,029 |

$16,655 |

$17,322 |

$17,710 |

$18,687 |

$19,565 |

| (Standard Error) |

($41) |

($32) |

($81) |

($25) |

($75) |

($98) |

($95) |

($61) |

($79) |

($95) |

($84) |

($105) |

($104) |

| <50 |

$10,632 |

$11,095 |

$11,679 |

$12,041 |

$13,170 |

$14,086 |

$14,496 |

$14,787 |

$15,575 |

$15,919 |

$16,471 |

$17,649 |

$18,296 |

| (Standard Error) |

($106) |

($116) |

($182) |

($129) |

($111) |

($145) |

($181) |

($89) |

($177) |

($212) |

($207) |

($192) |

($231) |

| 50-99 |

$10,619 |

$10,954 |

$11,578 |

$12,431 |

$13,019 |

$14,151 |

$15,421 |

$15,376 |

$15,732 |

$16,336 |

$16,214 |

$17,735 |

$18,386 |

| (Standard Error) |

($208) |

($301) |

($128) |

($229) |

($153) |

($168) |

($273) |

($268) |

($274) |

($335) |

($348) |

($327) |

($473) |

| 100+ |

$10,754 |

$11,471 |

$12,468 |

$13,271 |

$14,074 |

$15,245 |

$15,641 |

$16,284 |

$16,903 |

$17,612 |

$18,000 |

$18,911 |

$19,824 |

| (Standard Error) |

($55) |

($51) |

($95) |

($33) |

($85) |

($117) |

($114) |

($82) |

($91) |

($110) |

($95) |

($122) |

($118) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

Return to Table of Contents

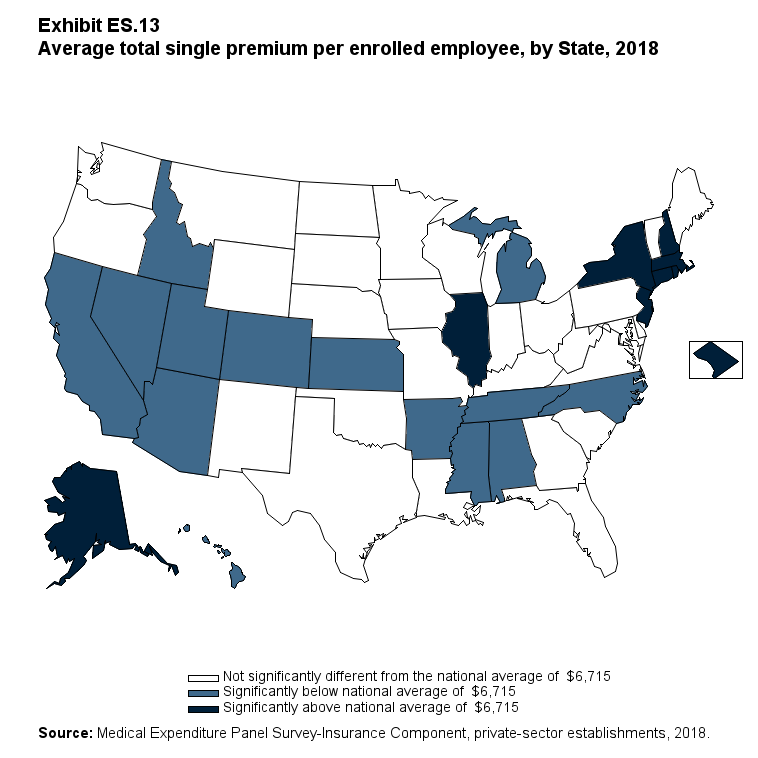

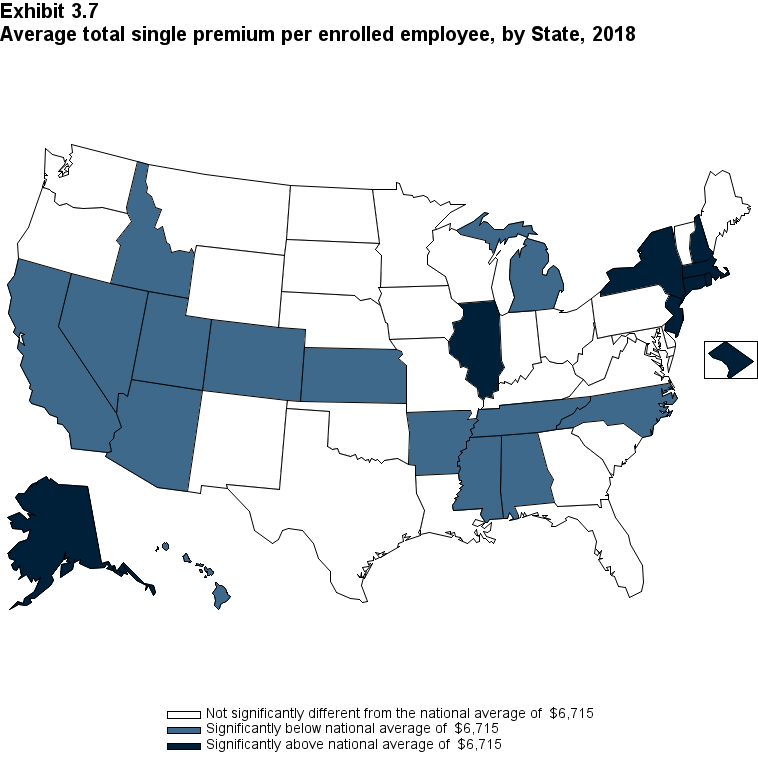

In total, 14 States had average annual premiums for single coverage that were significantly lower than the national average of $6,715: Alabama, Arizona, Arkansas, California, Colorado, Hawaii, Idaho, Kansas, Michigan, Mississippi, Nevada, North Carolina, Tennessee and Utah. Nine States had average annual single premiums that were significantly higher than the national average: Alaska, Connecticut, District of Columbia, Illinois, Massachusetts, New Hampshire, New Jersey, New York, and Rhode Island (Exhibit ES.13).

Exhibit ES.13 Average total single premium (standard error) per enrolled employee, by State, 2018

| Alabama |

$6,089* |

Kentucky |

$6,690 |

North Dakota |

$6,643 |

| (Standard Error) |

($138) |

(Standard Error) |

($221) |

(Standard Error) |

($132) |

| Alaska |

$8,432* |

Louisiana |

$6,537 |

Ohio |

$6,804 |

| (Standard Error) |

($199) |

(Standard Error) |

($197) |

(Standard Error) |

($129) |

| Arizona |

$6,229* |

Maine |

$6,866 |

Oklahoma |

$6,630 |

| (Standard Error) |

($140) |

(Standard Error) |

($144) |

(Standard Error) |

($156) |

| Arkansas |

$5,974* |

Maryland |

$6,695 |

Oregon |

$6,441 |

| (Standard Error) |

($167) |

(Standard Error) |

($194) |

(Standard Error) |

($160) |

| California |

$6,542* |

Massachusetts |

$7,443* |

Pennsylvania |

$6,769 |

| (Standard Error) |

($82) |

(Standard Error) |

($254) |

(Standard Error) |

($145) |

| Colorado |

$6,255* |

Michigan |

$6,322* |

Rhode Island |

$7,018* |

| (Standard Error) |

($121) |

(Standard Error) |

($147) |

(Standard Error) |

($143) |

| Connecticut |

$7,264* |

Minnesota |

$6,781 |

South Carolina |

$6,708 |

| (Standard Error) |

($149) |

(Standard Error) |

($157) |

(Standard Error) |

($145) |

| Delaware |

$6,848 |

Mississippi |

$5,993* |

South Dakota |

$6,931 |

| (Standard Error) |

($157) |

(Standard Error) |

($124) |

(Standard Error) |

($146) |

| District of Columbia |

$7,230* |

Missouri |

$6,664 |

Tennessee |

$5,971* |

| (Standard Error) |

($147) |

(Standard Error) |

($157) |

(Standard Error) |

($100) |

| Florida |

$6,674 |

Montana |

$6,862 |

Texas |

$6,589 |

| (Standard Error) |

($189) |

(Standard Error) |

($161) |

(Standard Error) |

($134) |

| Georgia |

$6,799 |

Nebraska |

$6,851 |

Utah |

$6,125* |

| (Standard Error) |

($163) |

(Standard Error) |

($219) |

(Standard Error) |

($162) |

| Hawaii |

$6,475* |

Nevada |

$6,032* |

Vermont |

$6,919 |

| (Standard Error) |

($114) |

(Standard Error) |

($166) |

(Standard Error) |

($148) |

| Idaho |

$6,175* |

New Hampshire |

$7,405* |

Virginia |

$6,635 |

| (Standard Error) |

($162) |

(Standard Error) |

($301) |

(Standard Error) |

($155) |

| Illinois |

$7,123* |

New Jersey |

$7,507* |

Washington |

$6,646 |

| (Standard Error) |

($166) |

(Standard Error) |

($126) |

(Standard Error) |

($154) |

| Indiana |

$6,778 |

New Mexico |

$6,624 |

West Virginia |

$6,898 |

| (Standard Error) |

($200) |

(Standard Error) |

($238) |

(Standard Error) |

($272) |

| Iowa |

$6,796 |

New York |

$7,741* |

Wisconsin |

$6,816 |

| (Standard Error) |

($160) |

(Standard Error) |

($211) |

(Standard Error) |

($142) |

| Kansas |

$6,262* |

North Carolina |

$6,339* |

Wyoming |

$6,779 |

| (Standard Error) |

($151) |

(Standard Error) |

($129) |

(Standard Error) |

($183) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2018.

Note: * Statistically different from national average of $6,715 at p < 0.05. Note that the standard error on the national estimate of $6,715 is $31.18.

|

Return to Table of Contents

Employee Premium Contributions

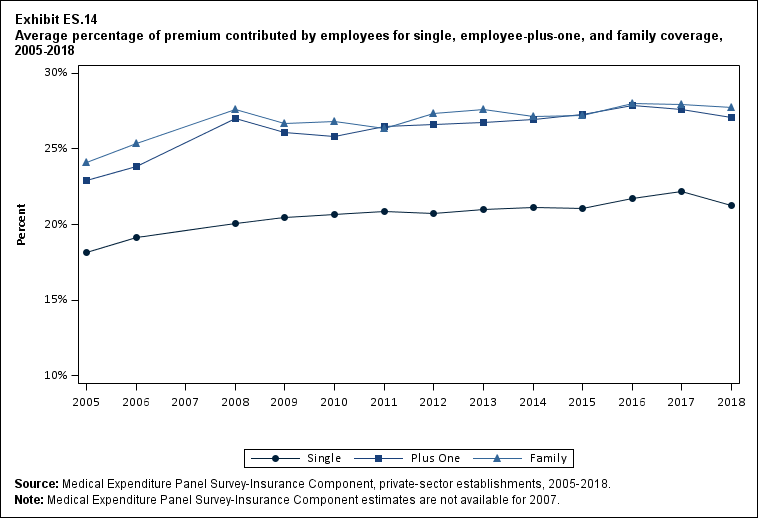

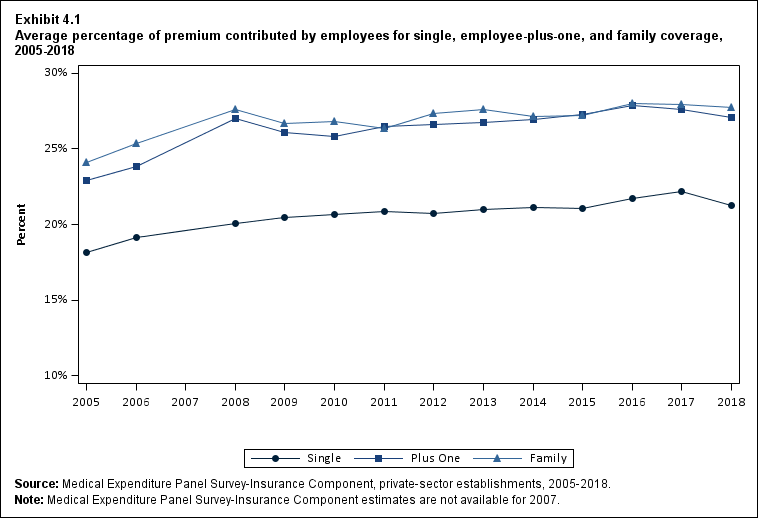

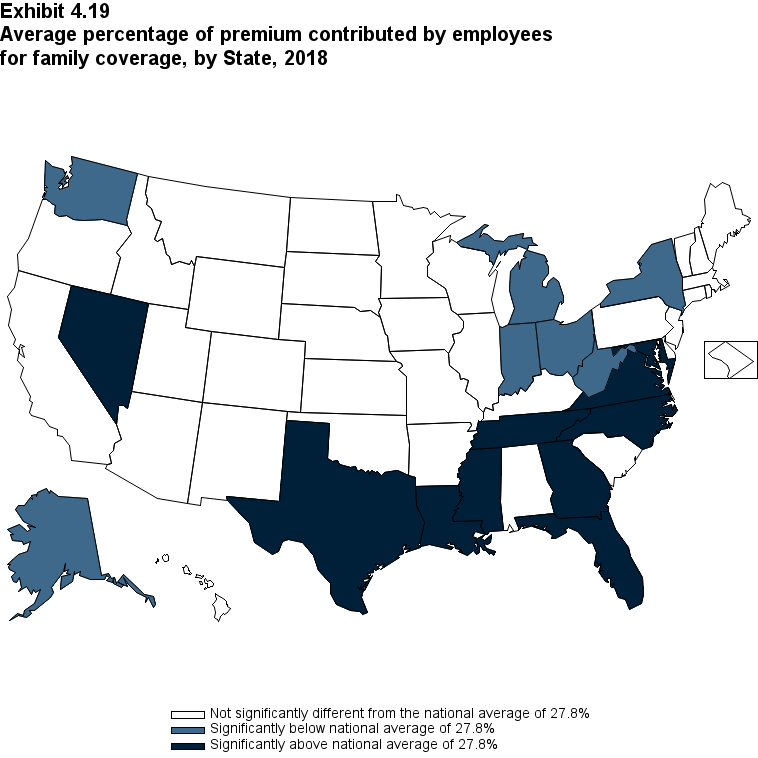

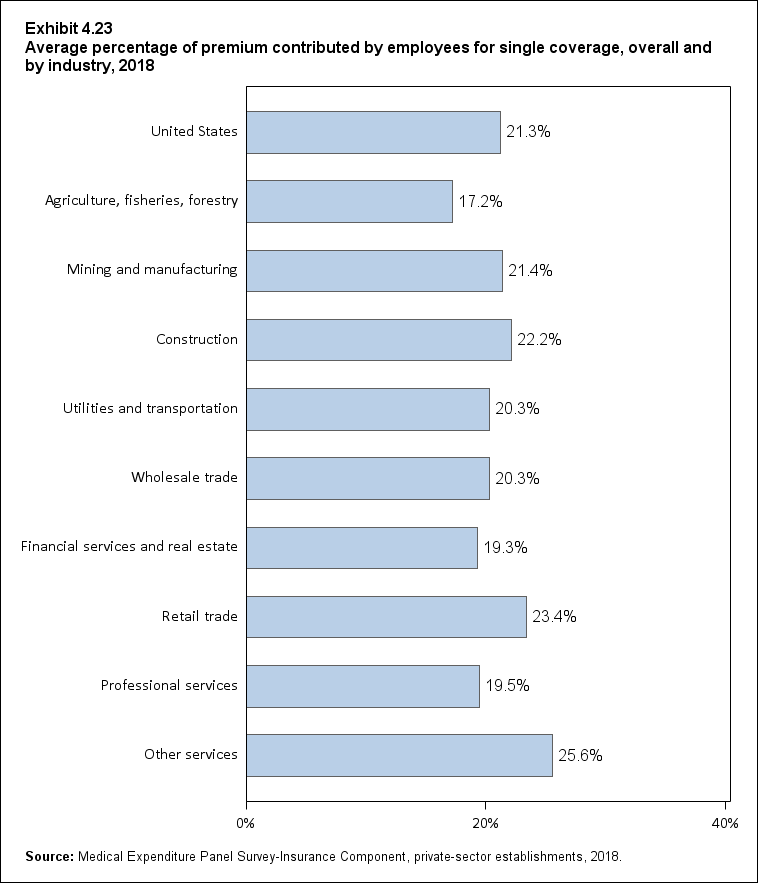

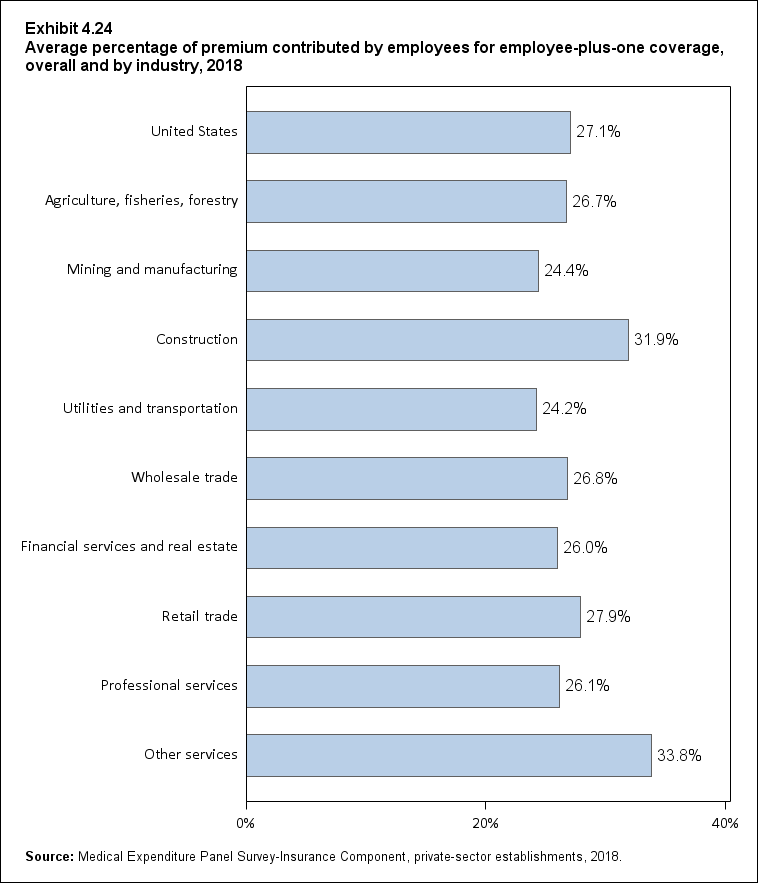

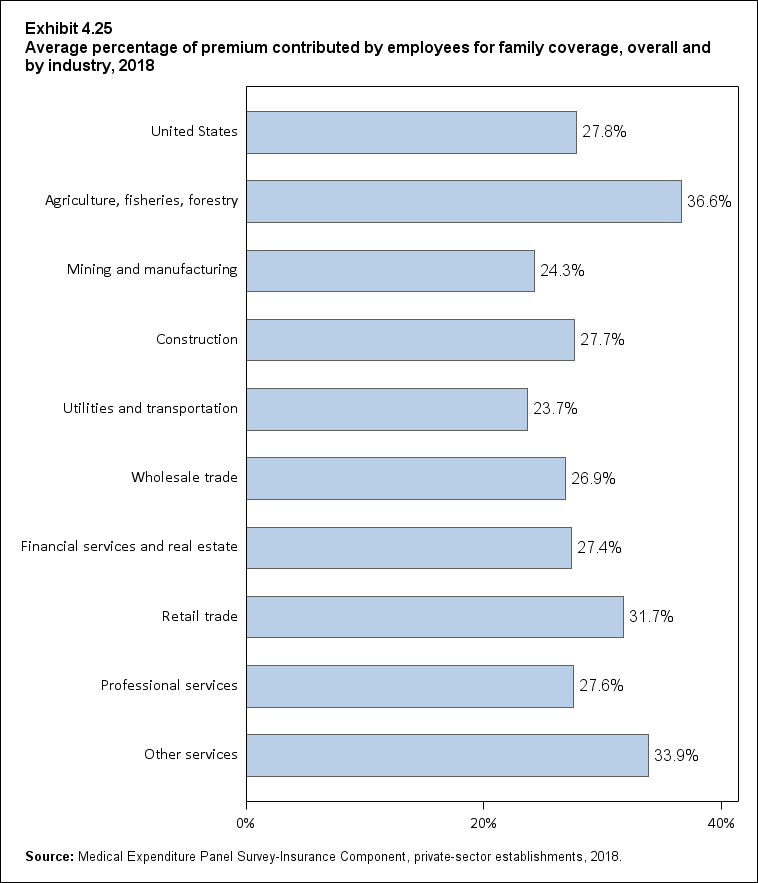

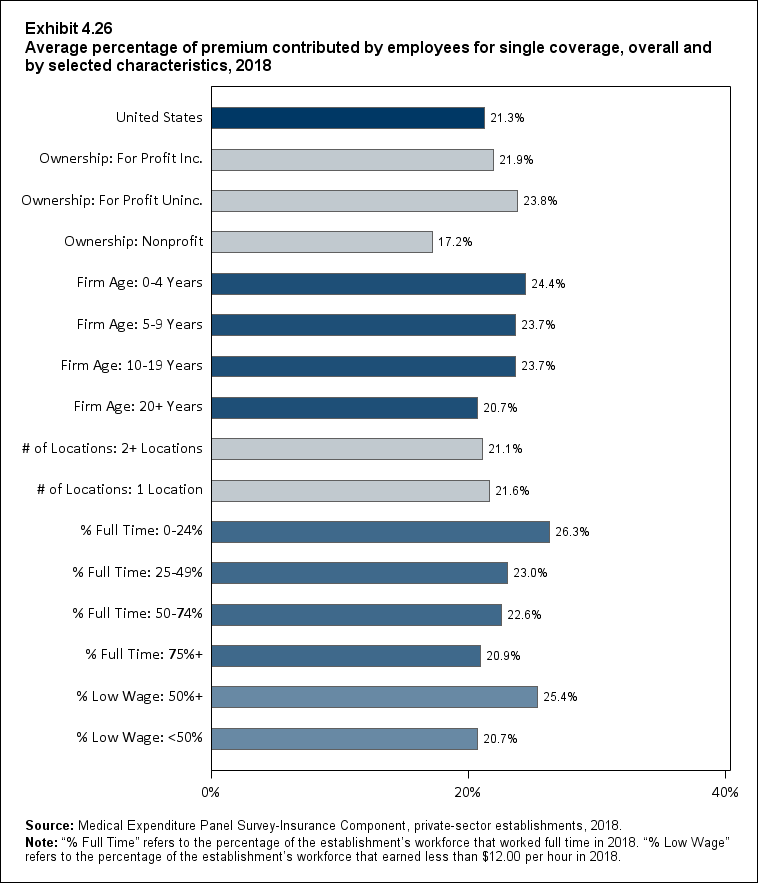

In 2018, enrolled employees paid 21.3 percent of total premiums for single coverage, 27.1 percent for employee-plus-one coverage, and 27.8 percent for family coverage (Exhibit ES.14). The employee share of total premiums in 2018 for single coverage decreased by 0.9 percentage points from its 2017 level, while the employee shares for the other two coverage types were not significantly different from their 2017 levels.

Exhibit ES.14 Average percentage (standard error) of premium contributed by employees for single, employee-plus-one, and family coverage, 2005‑2018

| Coverage |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| Single |

18.1% |

19.1% |

20.1% |

20.5% |

20.7% |

20.9% |

20.8% |

21.0% |

21.2% |

21.1% |

21.7% |

22.2% |

21.3% |

| (Standard Error) |

(0.4%) |

(0.4%) |

(0.2%) |

(0.3%) |

(0.2%) |

(0.2%) |

(0.3%) |

(0.3%) |

(0.2%) |

(0.2%) |

(0.2%) |

(0.2%) |

(0.2%) |

| Plus One |

22.9% |

23.8% |

27.0% |

26.1% |

25.8% |

26.5% |

26.6% |

26.7% |

26.9% |

27.3% |

27.8% |

27.6% |

27.1% |

| (Standard Error) |

(0.4%) |

(0.4%) |

(0.3%) |

(0.3%) |

(0.3%) |

(0.3%) |

(0.4%) |

(0.2%) |

(0.3%) |

(0.3%) |

(0.3%) |

(0.3%) |

(0.3%) |

| Family |

24.1% |

25.4% |

27.6% |

26.7% |

26.8% |

26.4% |

27.4% |

27.6% |

27.1% |

27.2% |

28.0% |

27.9% |

27.8% |

| (Standard Error) |

(0.4%) |

(0.3%) |

(0.4%) |

(0.3%) |

(0.4%) |

(0.3%) |

(0.4%) |

(0.3%) |

(0.3%) |

(0.3%) |

(0.3%) |

(0.4%) |

(0.3%) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

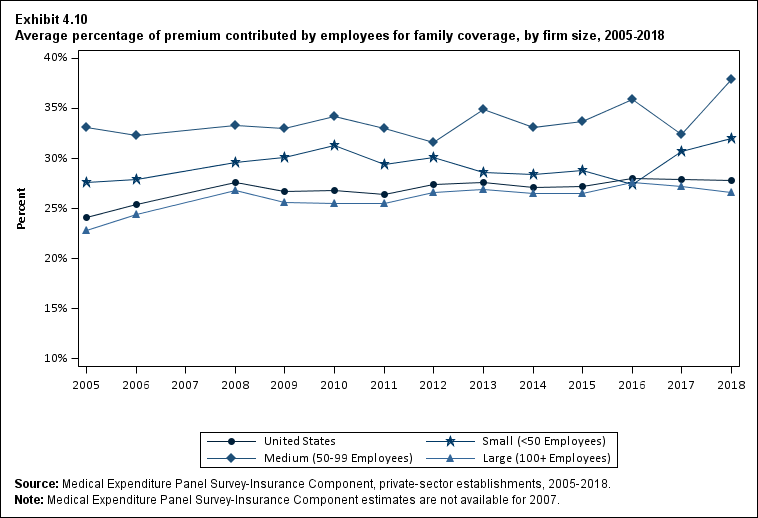

From 2005 to 2018, the percentage of premiums contributed by employees increased by 3.2 percentage points, 4.2 percentage points, and 3.7 percentage points for single, employee-plus-one, and family coverage, respectively (Exhibit ES.14). These increases occurred because employee contributions increased more rapidly than employer contributions over the entire period for each type of coverage (Section 4, Exhibits 4.1, 4.3, 4.4, and 4.5).

Return to Table of Contents

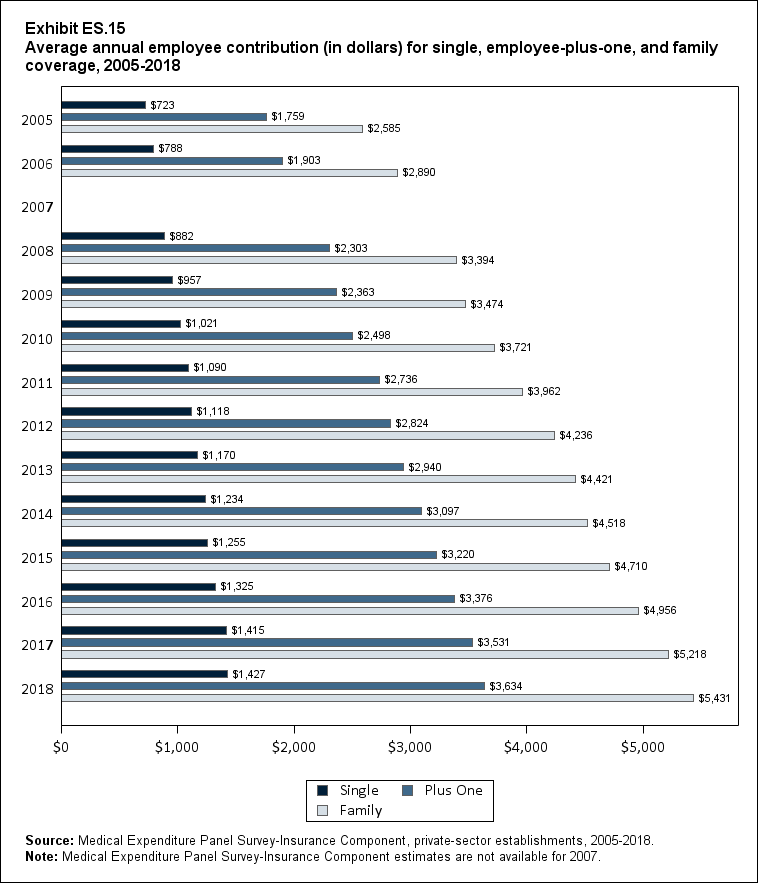

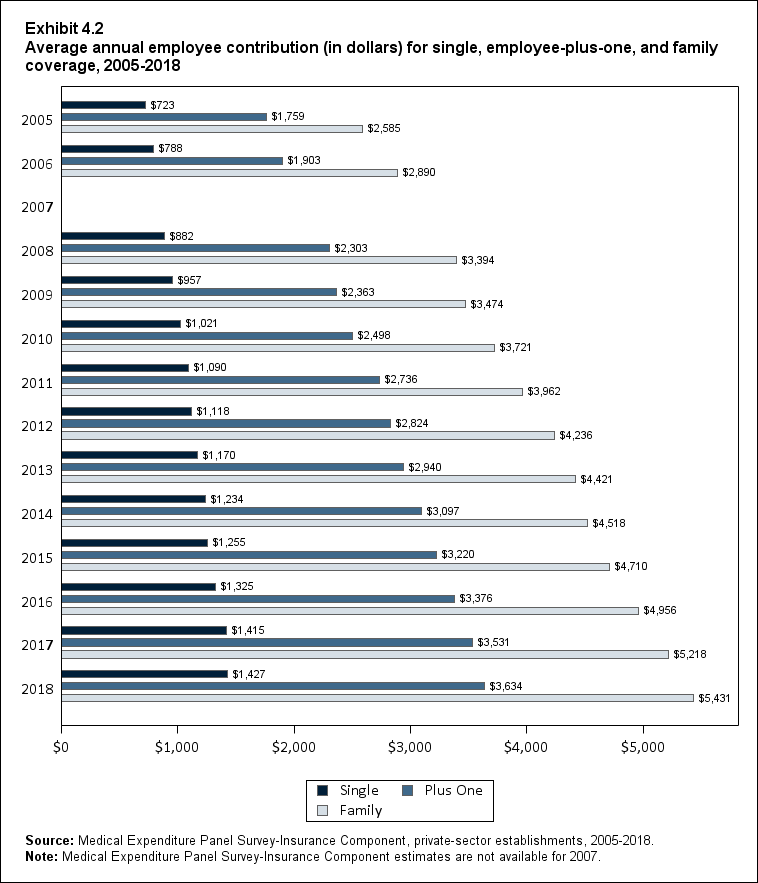

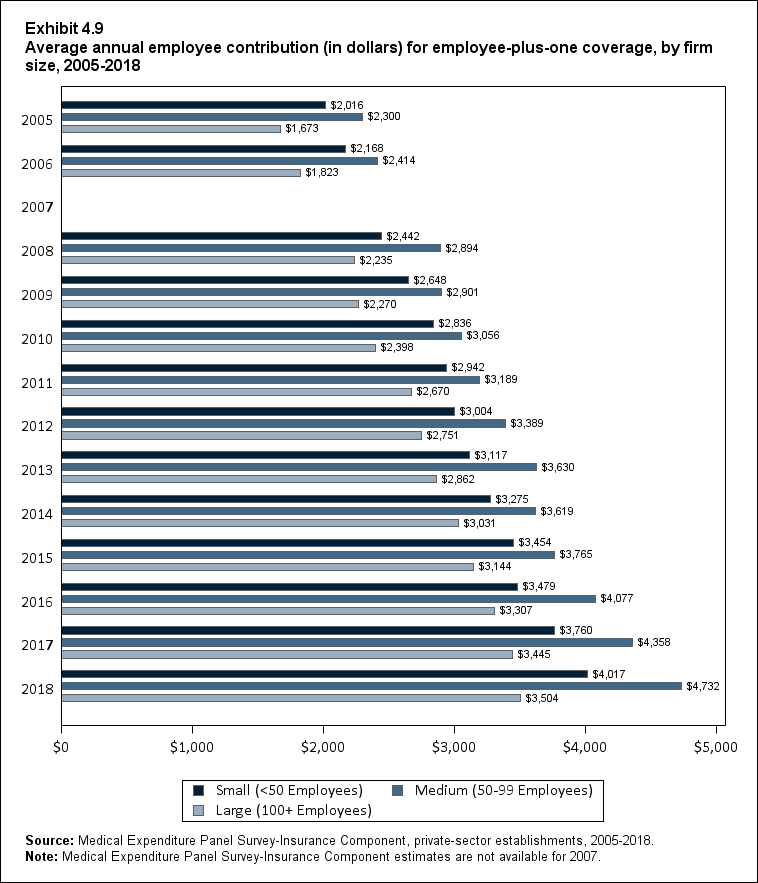

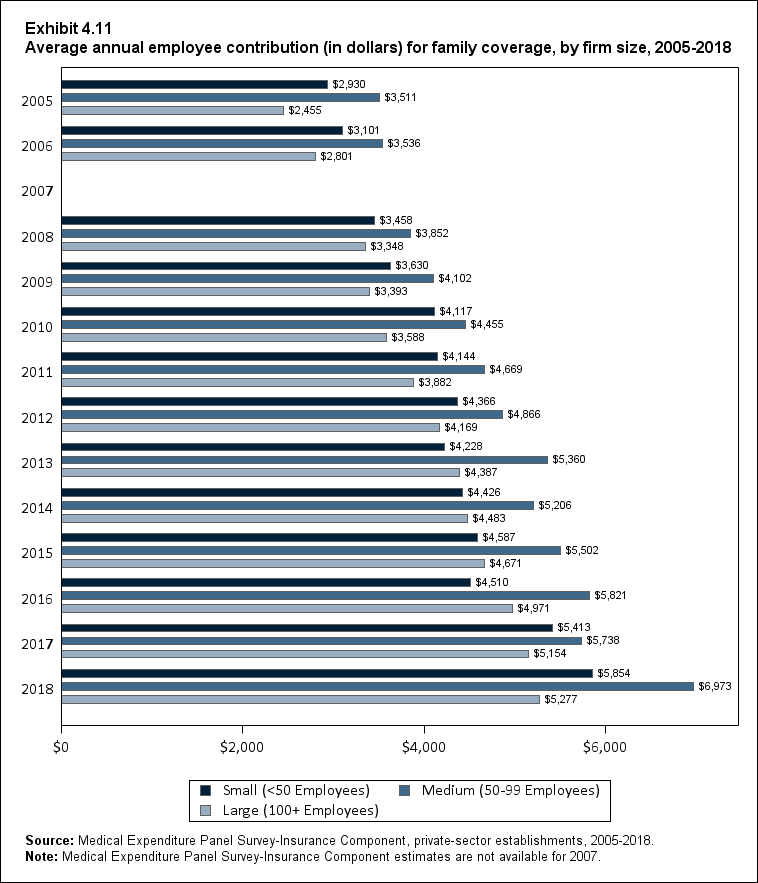

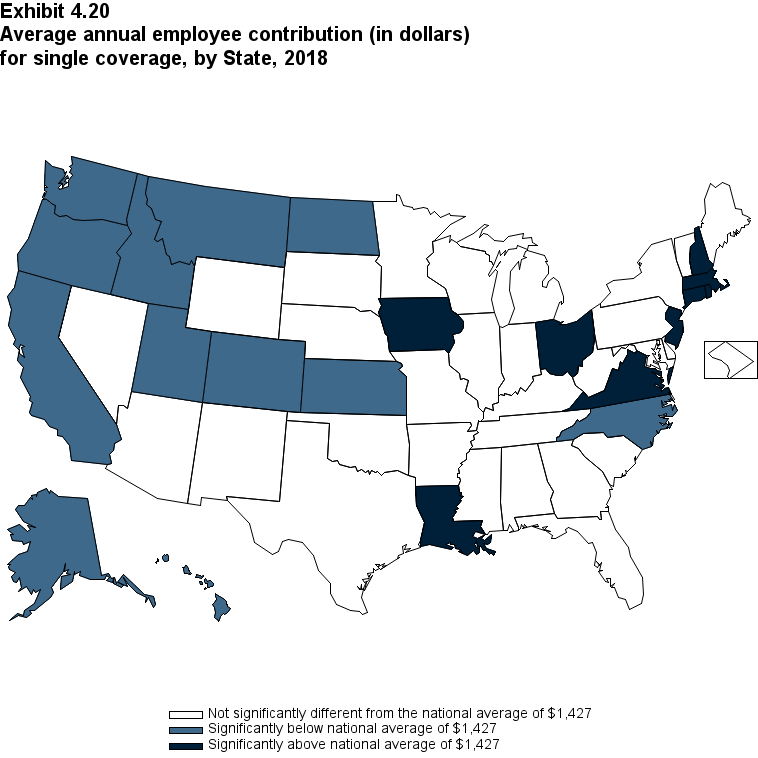

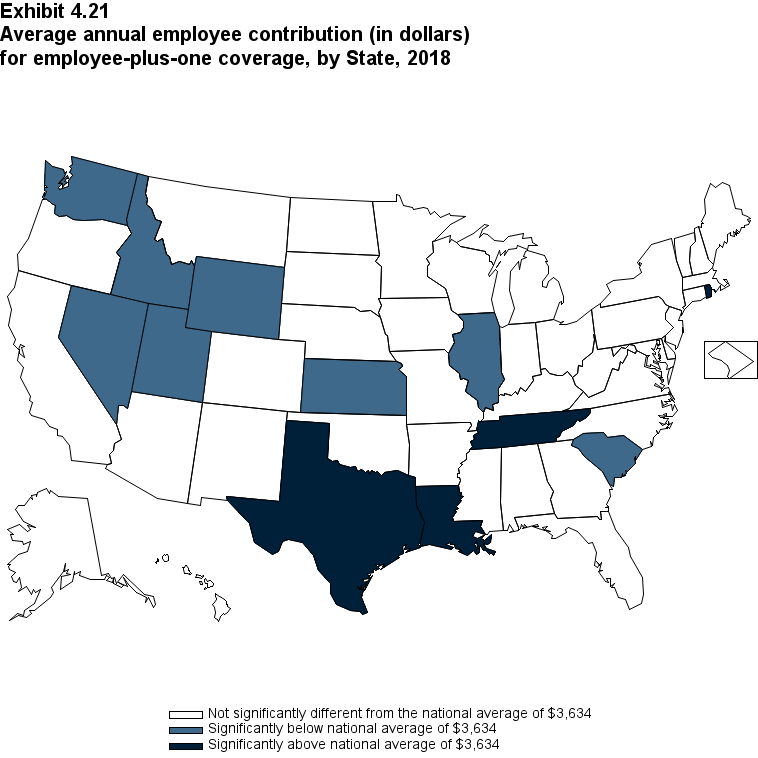

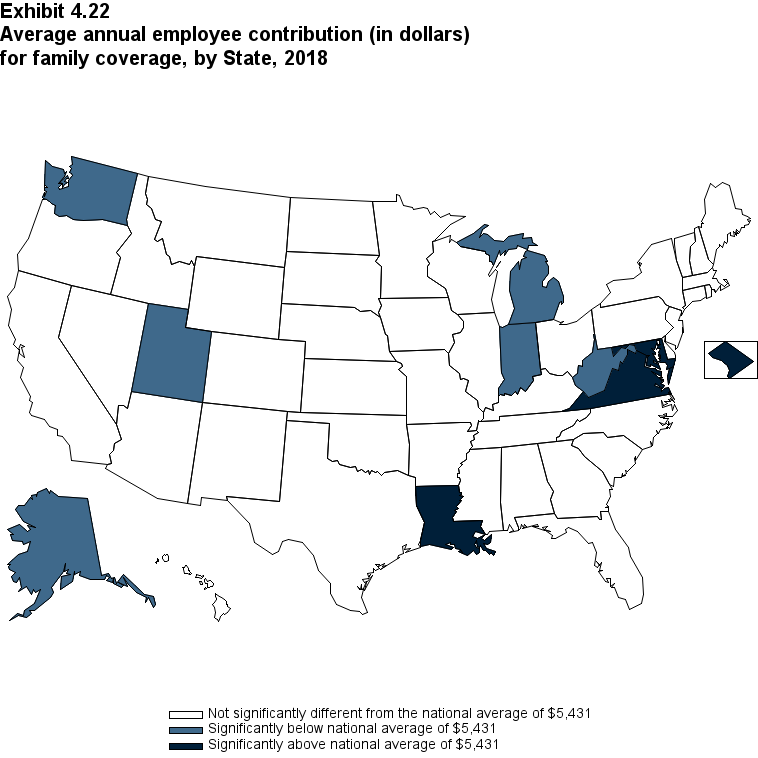

Average employee contributions in 2018 were $3,634 for employee-plus-one coverage and $5,431 for family coverage, representing increases of 2.9 percent and 4.1 percent, respectively, over 2017 levels (p <0.10 for employee-plus-one coverage). Employee contributions for single coverage in 2018 ($1,427) were not significantly different from average contributions in 2017 (Exhibit ES.15).

Exhibit ES.15 Average annual employee contribution (in dollars) (standard error) for single, employee-plus-one, and family coverage, 2005‑2018

| Coverage |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| Single |

$723 |

$788 |

$882 |

$957 |

$1,021 |

$1,090 |

$1,118 |

$1,170 |

$1,234 |

$1,255 |

$1,325 |

$1,415 |

$1,427 |

| (Standard Error) |

($14) |

($16) |

($6) |

($13) |

($14) |

($9) |

($14) |

($16) |

($13) |

($14) |

($13) |

($15) |

($14) |

| Plus One |

$1,759 |

$1,903 |

$2,303 |

$2,363 |

$2,498 |

$2,736 |

$2,824 |

$2,940 |

$3,097 |

$3,220 |

$3,376 |

$3,531 |

$3,634 |

| (Standard Error) |

($29) |

($24) |

($22) |

($27) |

($42) |

($36) |

($46) |

($23) |

($40) |

($35) |

($36) |

($39) |

($39) |

| Family |

$2,585 |

$2,890 |

$3,394 |

$3,474 |

$3,721 |

$3,962 |

$4,236 |

$4,421 |

$4,518 |

$4,710 |

$4,956 |

$5,218 |

$5,431 |

| (Standard Error) |

($38) |

($34) |

($54) |

($44) |

($53) |

($42) |

($69) |

($50) |

($48) |

($56) |

($56) |

($64) |

($63) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

Return to Table of Contents

Plan Benefits: Deductibles

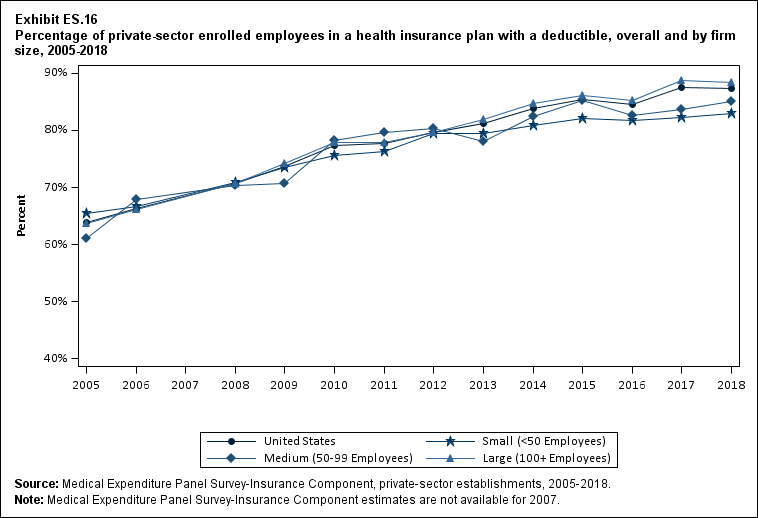

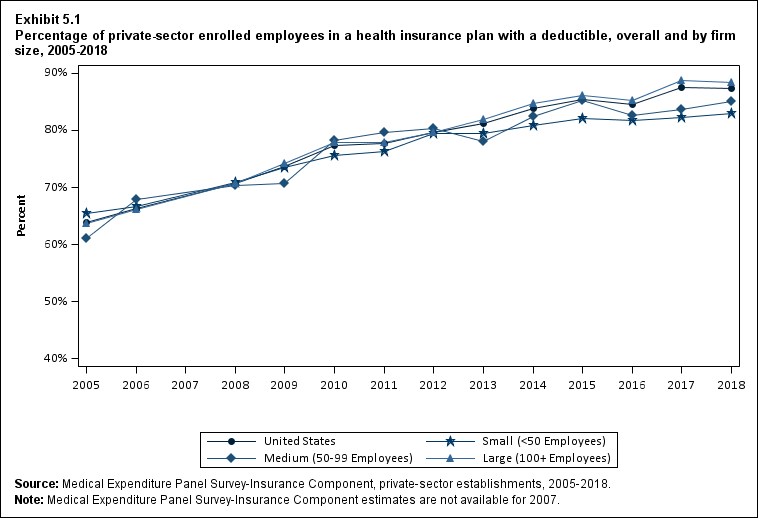

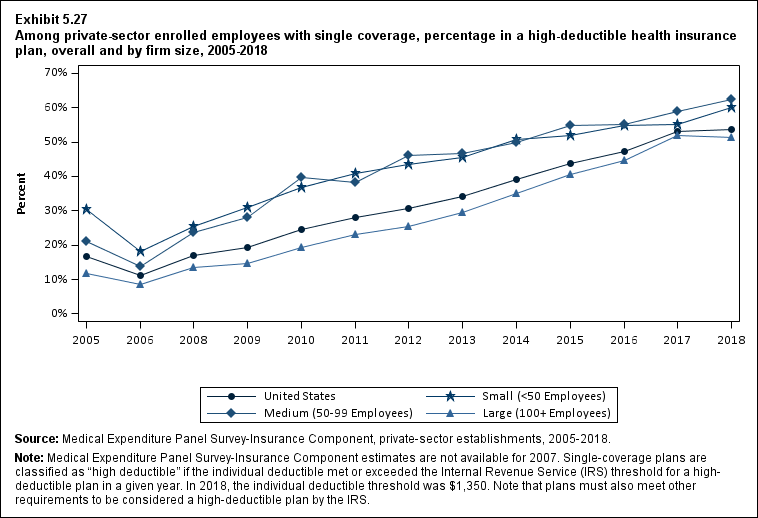

There was no significant change in the percentage of enrolled employees in a health insurance plan with a deductible from 2017 (87.5 percent) to 2018 (87.3 percent) (Exhibit ES.16). From 2005 to 2018, the percentage of enrollees in plans with deductibles increased from 63.9 percent to 87.3 percent.

Exhibit ES.16 Percentage (standard error) of private-sector enrolled employees in a health insurance plan with a deductible, overall and by firm size, 2005‑2018

| Number of Employees |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| U.S. |

63.9% |

66.4% |

70.7% |

73.8% |

77.5% |

77.8% |

79.6% |

81.3% |

83.9% |

85.4% |

84.5% |

87.5% |

87.3% |

| (Standard Error) |

(0.9%) |

(0.6%) |

(0.5%) |

(0.5%) |

(0.3%) |

(0.7%) |

(0.6%) |

(0.7%) |

(0.5%) |

(0.5%) |

(0.5%) |

(0.4%) |

(0.4%) |

| <50 |

65.5% |

66.6% |

70.9% |

73.5% |

75.7% |

76.3% |

79.5% |

79.5% |

80.8% |

82.1% |

81.7% |

82.3% |

83.0% |

| (Standard Error) |

(1.0%) |

(0.7%) |

(0.7%) |

(0.7%) |

(0.7%) |

(0.4%) |

(1.0%) |

(0.8%) |

(0.8%) |

(0.8%) |

(0.8%) |

(0.8%) |

(0.8%) |

| 50-99 |

61.1% |

67.9% |

70.3% |

70.6% |

78.2% |

79.6% |

80.3% |

78.0% |

82.4% |

85.3% |

82.5% |

83.7% |

85.1% |

| (Standard Error) |

(2.6%) |

(2.6%) |

(1.4%) |

(1.9%) |

(1.5%) |

(1.7%) |

(1.4%) |

(1.1%) |

(1.5%) |

(1.5%) |

(1.5%) |

(1.6%) |

(1.4%) |

| 100+ |

63.8% |

66.2% |

70.7% |

74.2% |

77.8% |

77.9% |

79.6% |

81.9% |

84.6% |

86.1% |

85.2% |

88.8% |

88.3% |

| (Standard Error) |

(1.0%) |

(0.8%) |

(0.6%) |

(0.6%) |

(0.3%) |

(1.0%) |

(0.7%) |

(0.7%) |

(0.6%) |

(0.6%) |

(0.6%) |

(0.4%) |

(0.5%) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007.

|

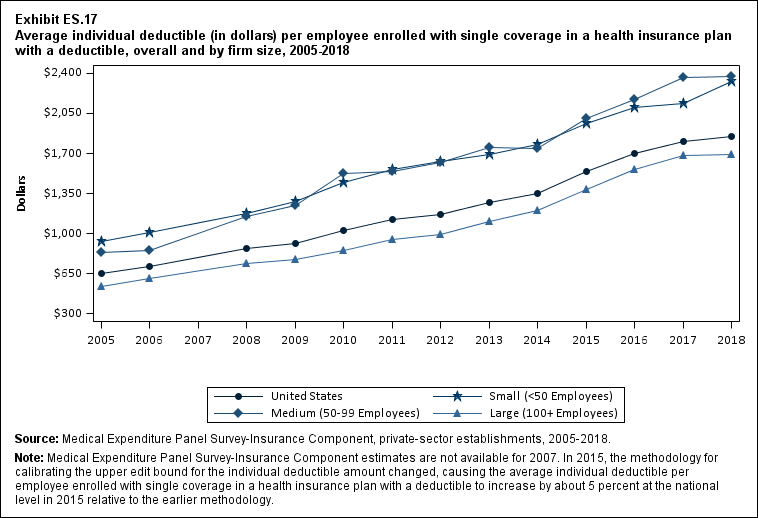

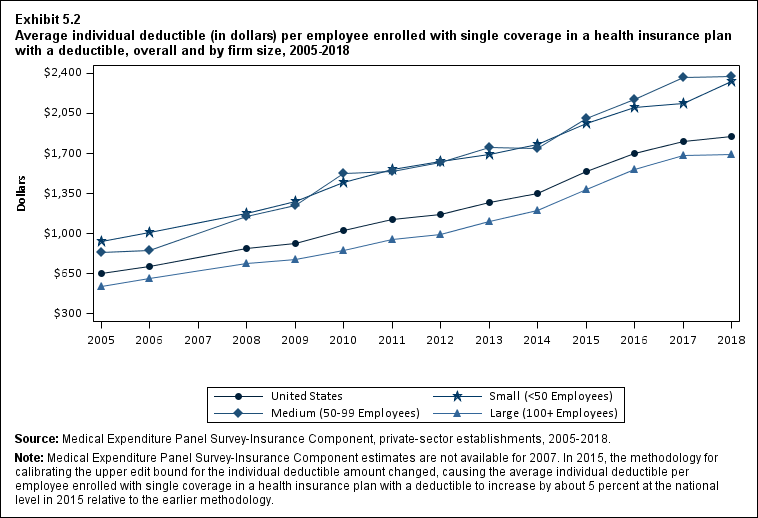

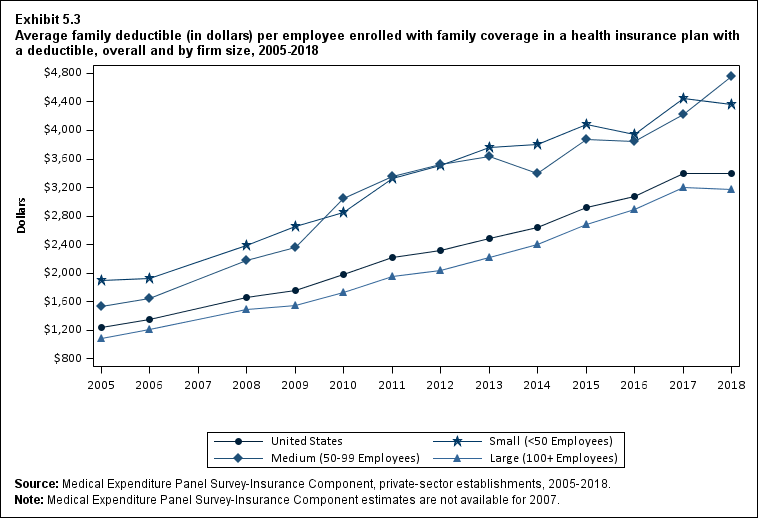

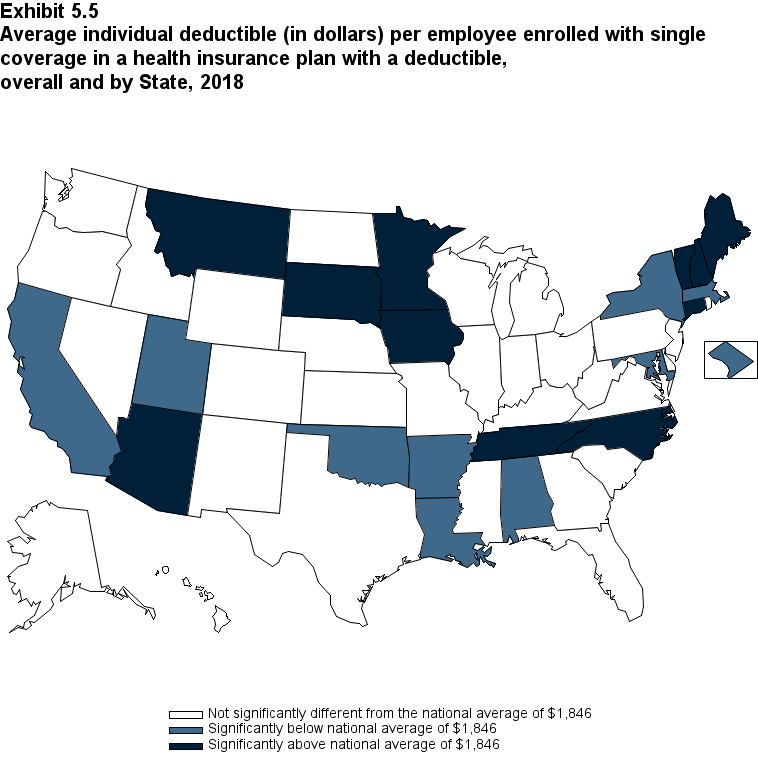

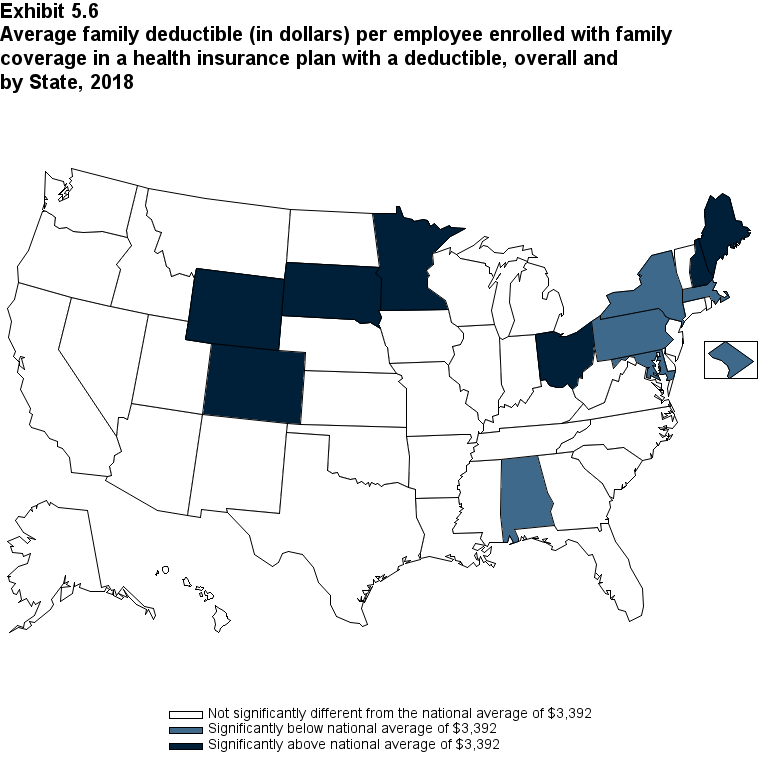

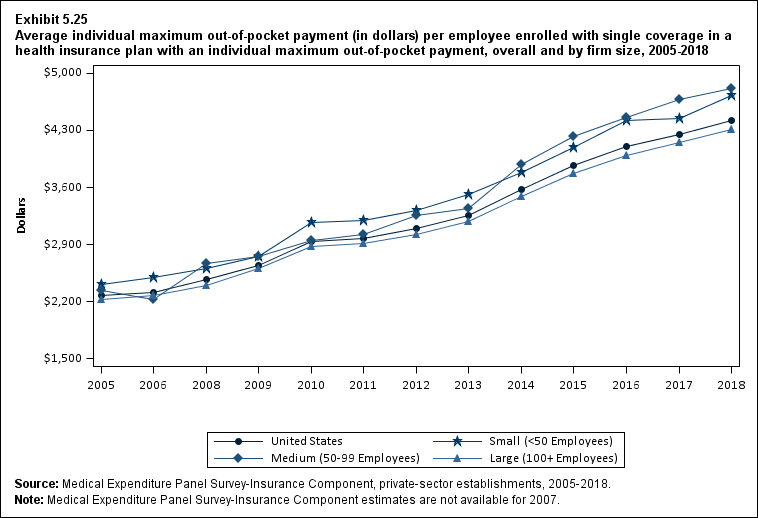

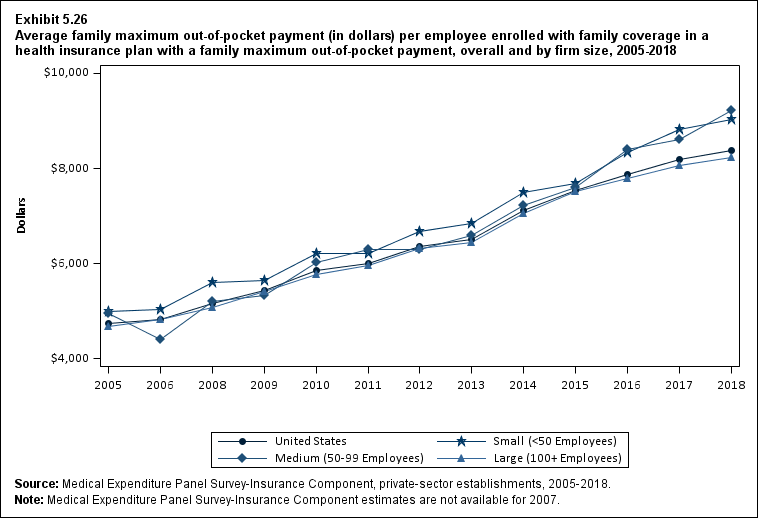

There was also no significant change in average deductible levels among single- and family-coverage enrollees in a plan with a deductible from 2017 to 2018, making 2018 the first year without a significant increase in the 2005 to 2018 period (Figure ES.17). Among enrollees with deductibles, average individual deductibles in 2018 were higher in small ($2,327) and medium ($2,369) firms than in large firms ($1,692) (Figure ES.17). Family deductibles in 2018 were higher in medium firms ($4,755) than in small firms ($4,364) and both were higher than in large firms ($3,179) (Section 5, Exhibit 5.3).

Return to Table of Contents

Exhibit ES.17 Average individual deductible (in dollars) (standard error) per employee enrolled with single coverage in a health insurance plan with a deductible, overall and by firm size, 2005‑2018

| Number of Employees |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| U.S. |

$652 |

$714 |

$869 |

$917 |

$1,025 |

$1,123 |

$1,167 |

$1,273 |

$1,353 |

$1,541 |

$1,696 |

$1,808 |

$1,846 |

| (Standard Error) |

($11) |

($9) |

($7) |

($9) |

($18) |

($12) |

($8) |

($20) |

($13) |

($16) |

($16) |

($17) |

($17) |

| <50 |

$929 |

$1,007 |

$1,177 |

$1,283 |

$1,447 |

$1,561 |

$1,628 |

$1,695 |

$1,777 |

$1,964 |

$2,105 |

$2,136 |

$2,327 |

| (Standard Error) |

($20) |

($20) |

($13) |

($24) |

($21) |

($26) |

($25) |

($24) |

($28) |

($35) |

($34) |

($35) |

($36) |

| 50-99 |

$836 |

$855 |

$1,149 |

$1,249 |

$1,522 |

$1,543 |

$1,622 |

$1,755 |

$1,744 |

$2,008 |

$2,173 |

$2,361 |

$2,369 |

| (Standard Error) |

($67) |

($71) |

($62) |

($46) |

($57) |

($49) |

($64) |

($49) |

($59) |

($62) |

($64) |

($85) |

($65) |

| 100+ |

$539 |

$605 |

$740 |

$774 |

$852 |

$951 |

$989 |

$1,106 |

$1,205 |

$1,383 |

$1,558 |

$1,681 |

$1,692 |

| (Standard Error) |

($9) |

($12) |

($8) |

($7) |

($20) |

($14) |

($10) |

($19) |

($14) |

($18) |

($18) |

($20) |

($19) |

|

Source: Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2005‑2018.

Note: Medical Expenditure Panel Survey-Insurance Component estimates are not available for 2007. In 2015, the methodology for calibrating the upper edit bound for the individual deductible amount changed,

causing the average individual deductible per employee enrolled with single coverage in a health insurance plan with a deductible to increase by about 5 percent at the national level in 2015 relative to the earlier methodology.

|

Conclusion

AHRQ produces this chartbook to make MEPS-IC data more readily usable by providing trends nationally and by firm size, by presenting national and State-level estimates in one document, and by providing additional firm-size cuts relevant to recent policy changes.

More information is available at meps.ahrq.gov.

AHRQ welcomes feedback on additional ways to make the data more usable to the public.

Return to Table of Contents

Availability of Coverage to Active Employees and Retirees

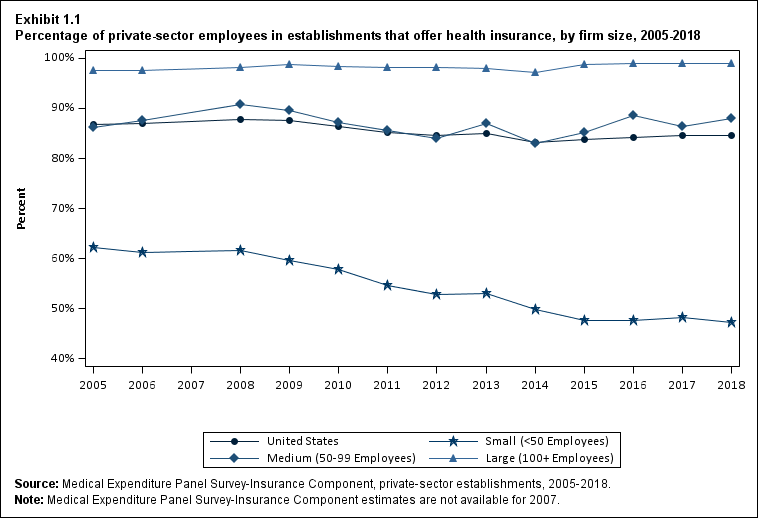

In 2018, almost all private-sector employees (99.0 percent) in firms with 100 or more employees worked at establishments that offered health insurance. In comparison, about half (47.3 percent) of employees at firms with fewer than 50 employees worked where health insurance was offered (Exhibit 1.1).

Historically, smaller employers have been less likely to offer health insurance coverage than larger employers for a number of reasons, including:

- Smaller risk pools, which result in higher premium costs (holding benefits constant),

- Higher administrative costs, and

- Lack of dedicated staff to select and administer health benefits.

This section presents estimates of the percentage of employees who work where coverage is offered (the "offer rate"). It also provides information on the characteristics of offered coverage, including the availability of dependent coverage, choice of plans, and retiree coverage. In addition, this section presents estimates of the percentage of offering establishments that self-insure at least one plan.

Offer Rates Overall and by Firm Size

- There was no significant change in the overall percentage of employees working at establishments where insurance was offered ("the offer rate") between 2017 (84.5 percent) and 2018 (84.6 percent) (Exhibit 1.1).

- There was no significant change in the offer rate at small employers (fewer than 50 employees) between 2017 (48.3 percent) and 2018 (47.3 percent). There was also no significant year-to-year change in offer rates at medium employers (50 to 99 employees) or at large firms (100 or more employees) (Exhibit 1.1).

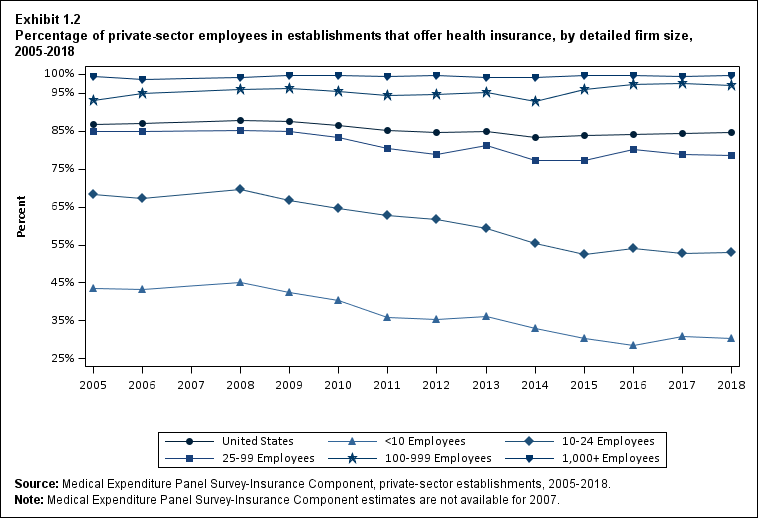

- The only significant change in offer rates by detailed firm size categories was for firms with 1,000 or more employees. For employees of such firms, the offer rate increased from 99.5 percent in 2017 to 99.8 percent in 2018 (Exhibit 1.2).

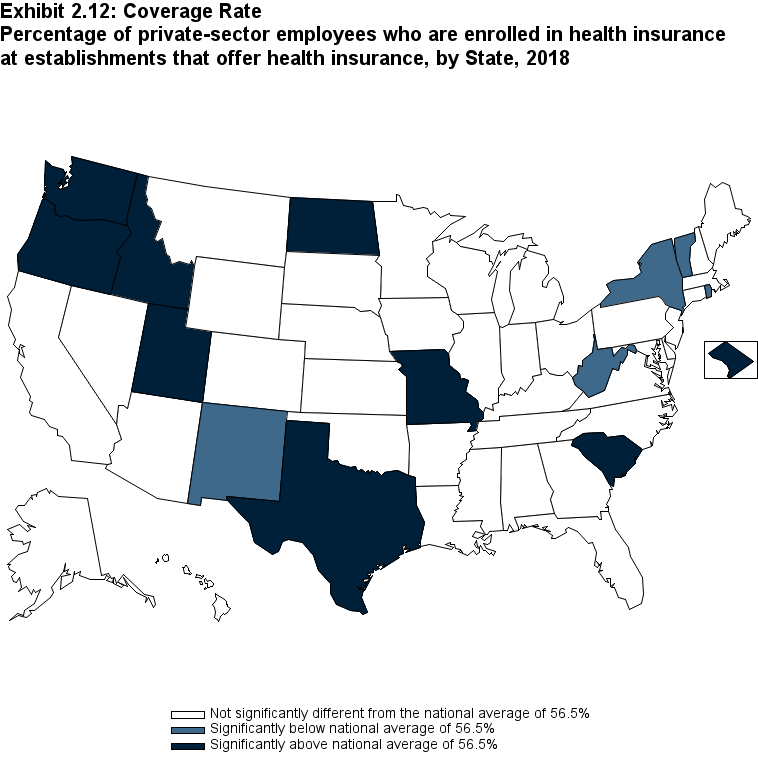

Offer Rates by State

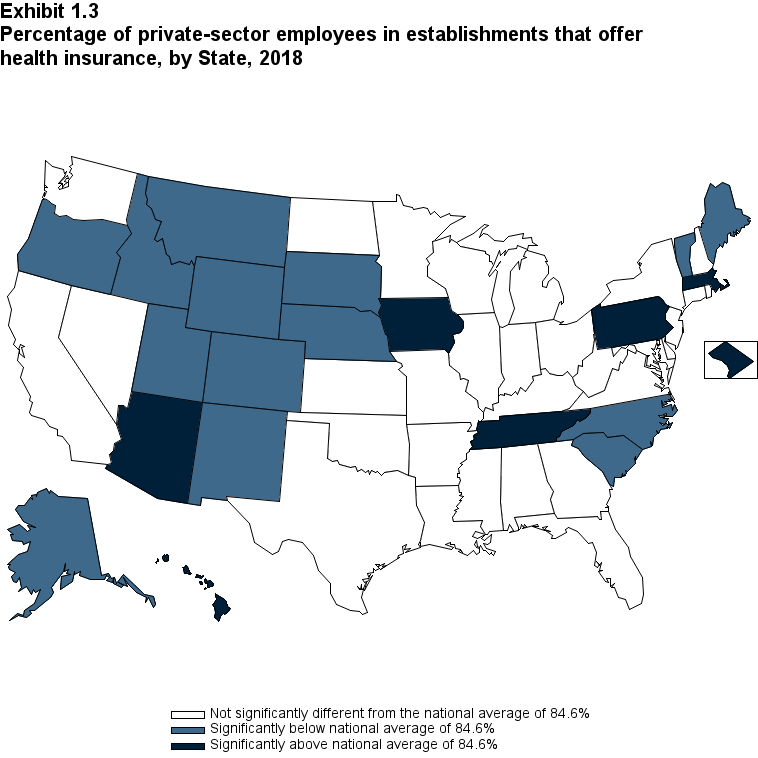

- Nationwide, 84.6 percent of all private-sector employees worked at establishments that offered insurance in 2018. The availability of workplace coverage varied substantially across the country (Exhibit 1.3). This variation was driven in part by differences in the distribution of workers by employer size across States (data not shown) and by differences across States in offer rates at smaller employers (Exhibit 1.4).

- States with offer rates exceeding the national average were Arizona, District of Columbia, Hawaii, Iowa, Massachusetts, Pennsylvania, and Tennessee (Exhibit 1.3).

- States with offer rates below the national average in 2018 were Alaska, Colorado, Idaho, Maine, Montana, Nebraska, New Mexico, North Carolina, Oregon, South Carolina, South Dakota, Utah, Vermont, and Wyoming (Exhibit 1.3).

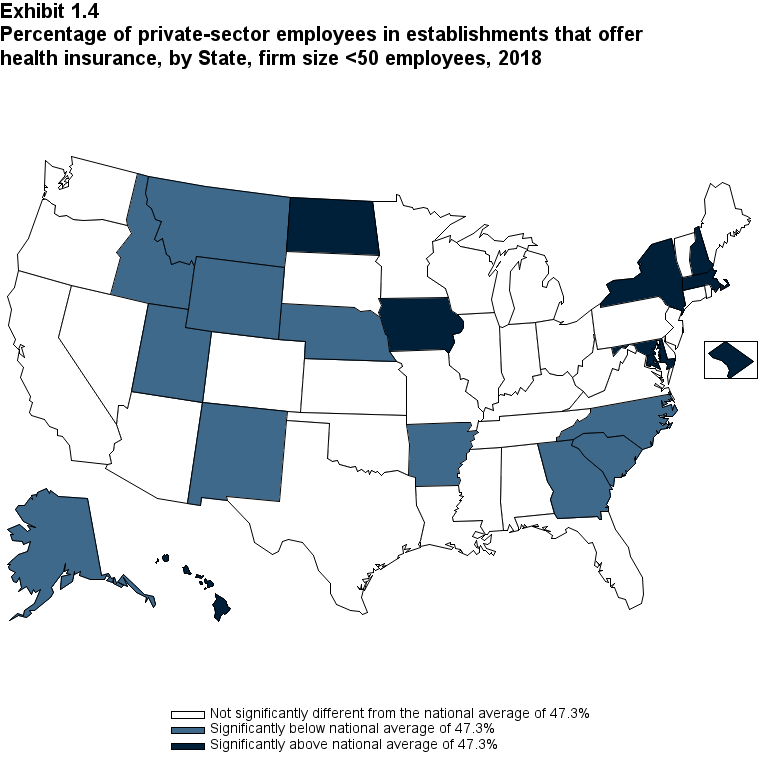

Offer Rates at Small Employers, by State

- Nationwide, less than half (47.3 percent) of employees of small firms (fewer than 50 employees) worked at establishments that offered insurance in 2018. However, the availability of workplace coverage at small firms varied substantially across the country (Exhibit 1.4).

- States with small-employer offer rates exceeding the national average were the District of Columbia, Hawaii, Iowa, Maryland, Massachusetts, New Hampshire, New York, and North Dakota (Exhibit 1.4).

- States with small-employer offer rates below the national average were Alaska, Arkansas, Georgia, Idaho, Montana, Nebraska, New Mexico, North Carolina, South Carolina, Utah, and Wyoming (Exhibit 1.4).

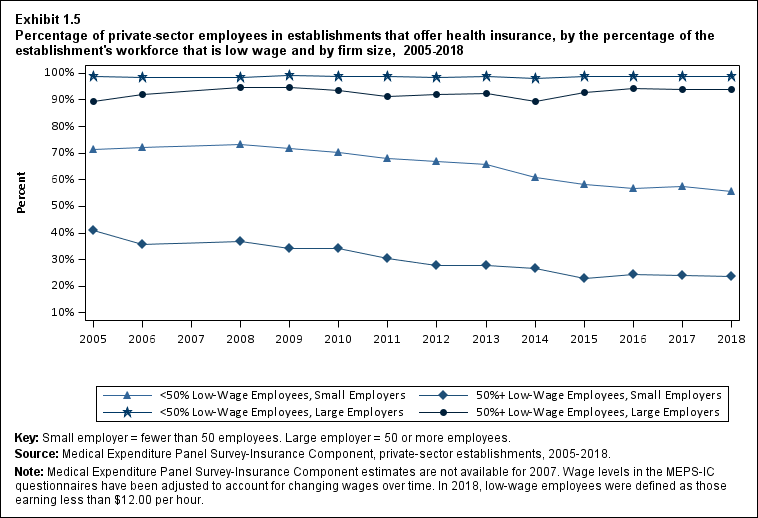

Offer Rates at Employers That Are Predominantly Low Wage vs. Higher Wage Establishments, by Firm Size

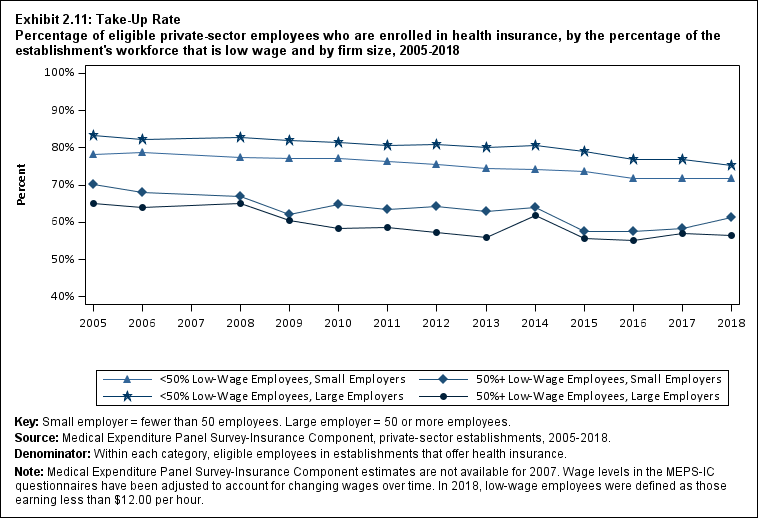

- In 2018, workers at predominantly low-wage small employers (fewer than 50 employees) faced offer rates that were less than half the rate at small employers with higher wages (23.6 percent vs. 55.5 percent) (Exhibit 1.5). (Predominantly low-wage establishments are defined as those where 50 percent or more of an establishment's workforce were low wage. Wage levels used in the question about the wage distribution in the MEPS-IC questionnaire have been adjusted to account for changing wages over time. In 2018, low-wage employees were defined as those earning less than $12.00 per hour.)

- Among the four subgroups of establishments jointly defined by firm size and wage level, the only significant change in offer rates occurred at small employers with higher wages (establishments that were not predominantly low wage). The offer rate at such employers declined from 57.6 percent in 2017 to 55.5 percent in 2018 (Exhibit 1.5).

Offer Rates by Industry

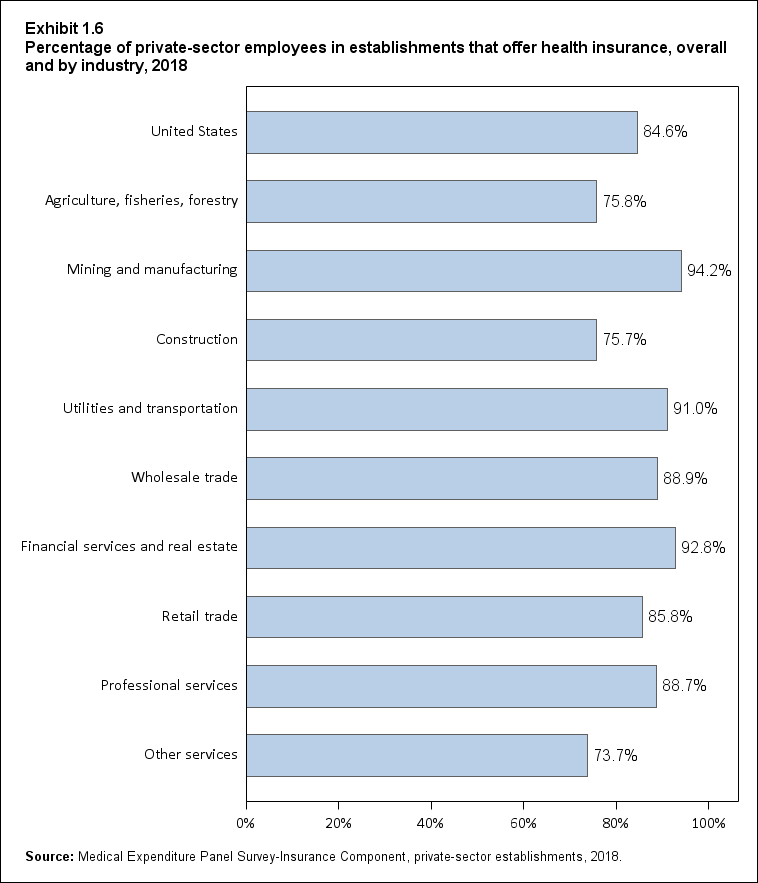

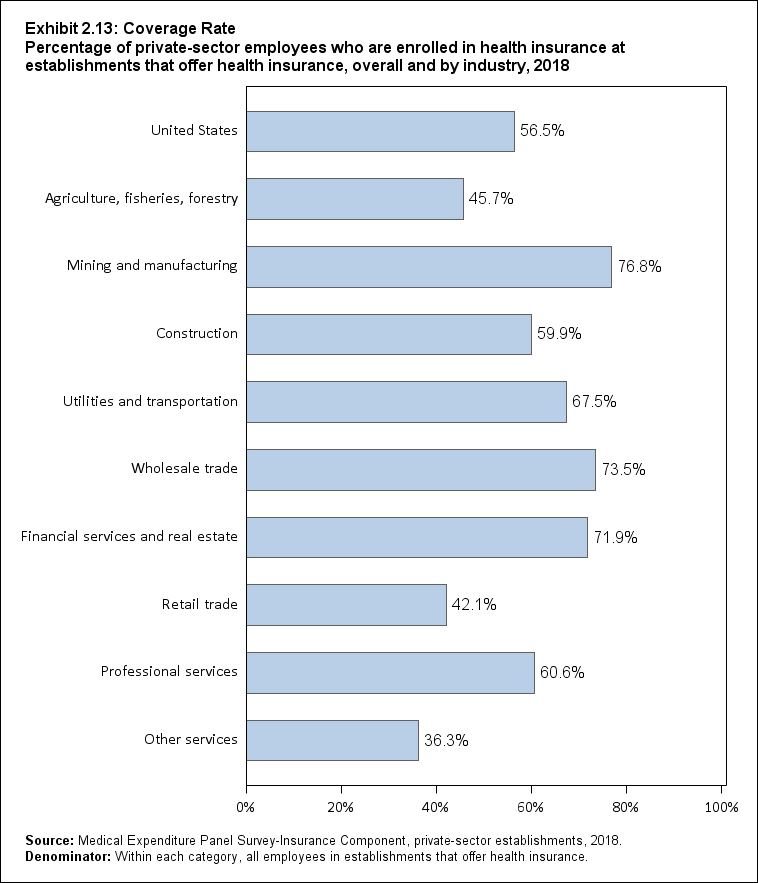

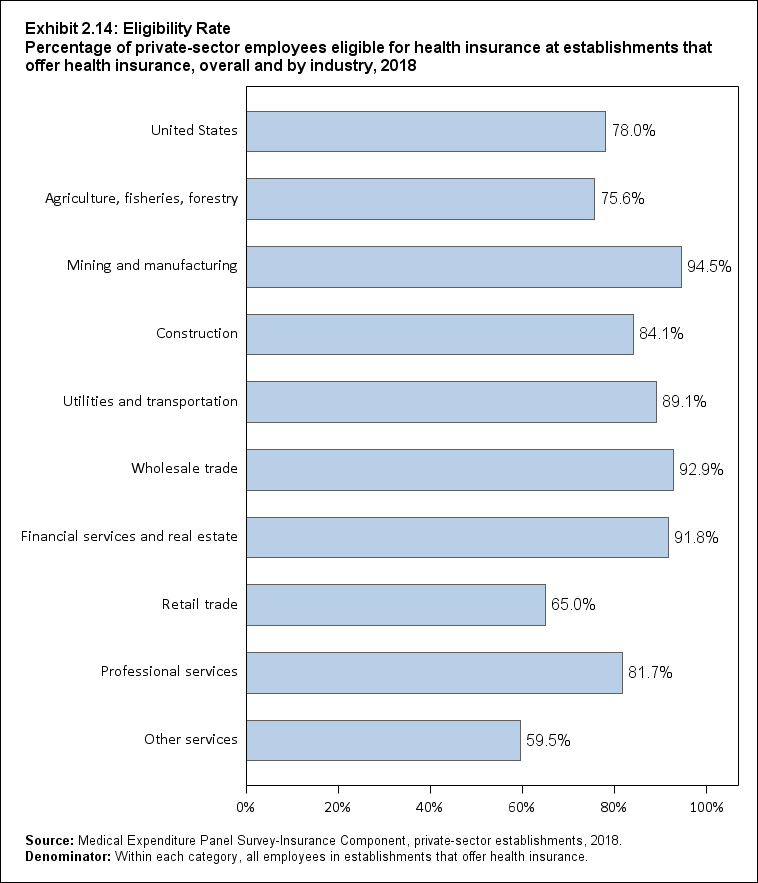

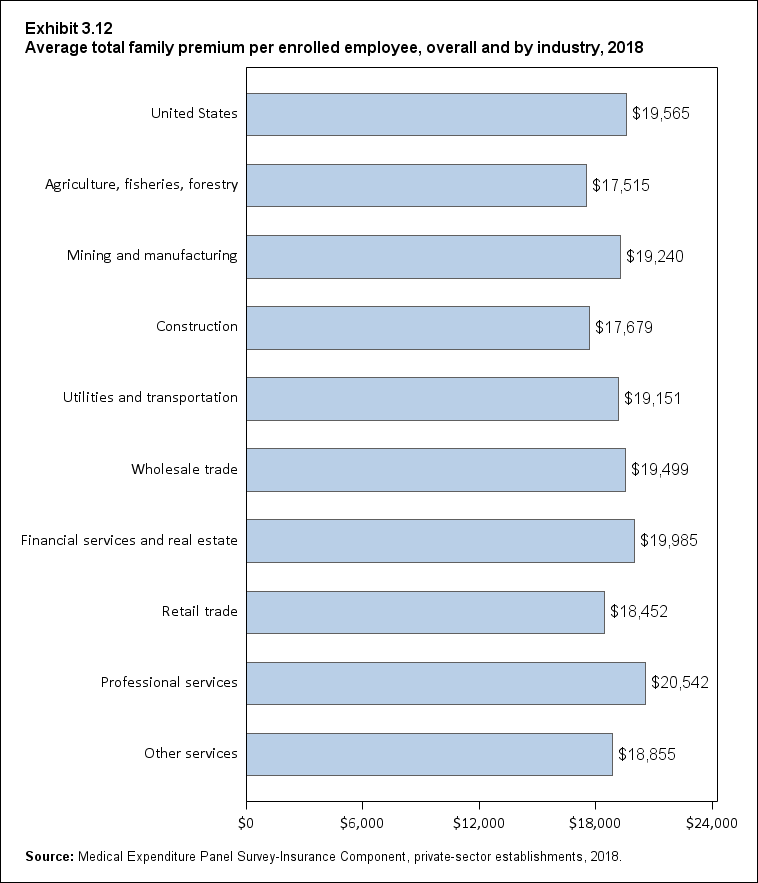

- In 2018, workers in mining and manufacturing had the highest likelihood of working where health insurance was offered (94.2 percent) while workers in the agriculture, fisheries, and forestry sector (75.8 percent), construction (75.7 percent), and other services (73.7 percent) had the lowest offer rates among all industry sectors (Exhibit 1.6).

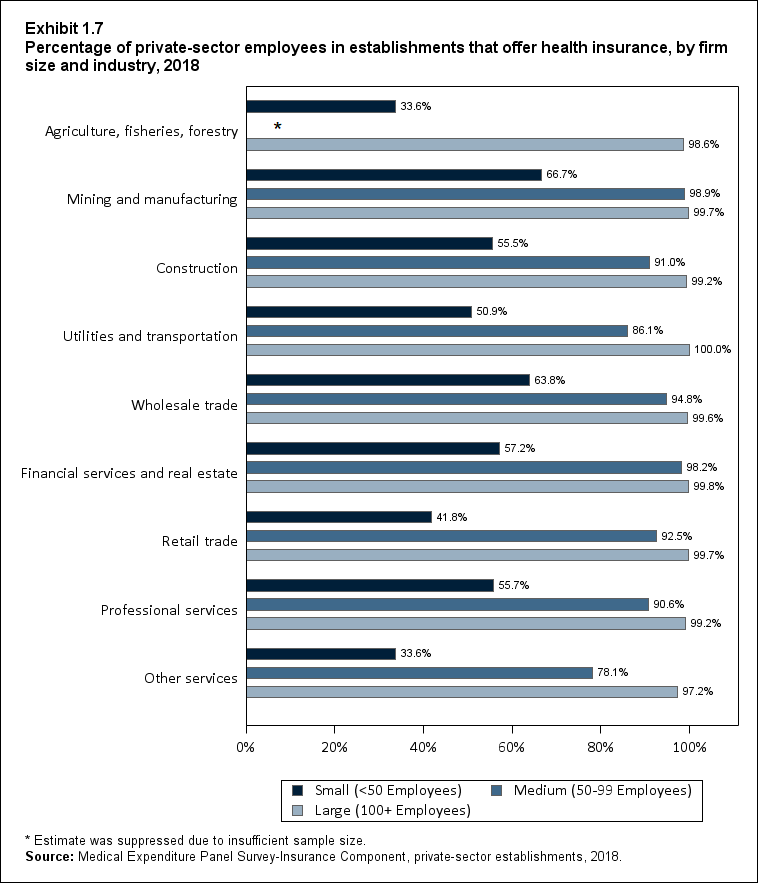

- Among workers at small firms (fewer than 50 employees), those employed in mining and manufacturing (66.7 percent) or wholesale trade (63.8 percent) had the highest likelihood of working where health insurance was offered (p <0.10 for the difference between wholesale trade and the financial services and real estate sector). Those employed in the agriculture, fisheries, and forestry sector and in other services had the lowest likelihood (33.6 percent), although there was no significant difference between the agriculture, fisheries, and forestry sector and the retail trade sector (Exhibit 1.7).

Offer Rates by Selected Employer Characteristics

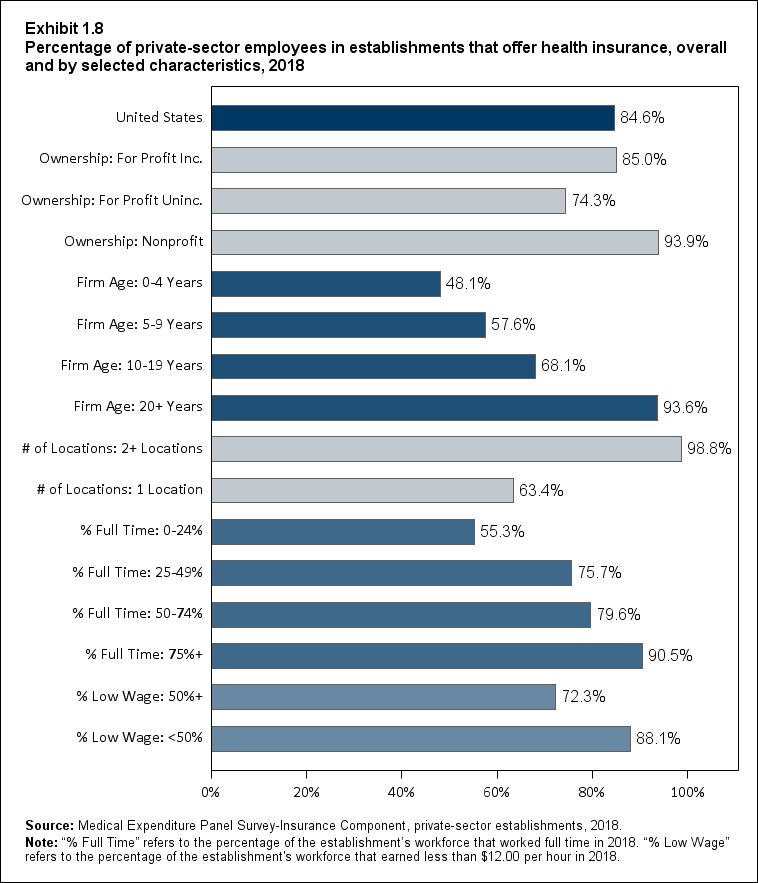

- Workers at nonprofit employers were more likely to work where health insurance was offered (93.9 percent) than workers at for-profit employers. Among for-profit employers, the offer rate was higher at incorporated employers (85.0 percent) than at unincorporated employers (74.3 percent) (Exhibit 1.8).

- Offer rates increased with the firm's age, from 48.1 percent at firms 0 to 4 years old to 57.6 percent, 68.1 percent, and 93.6 percent for firms ages 5-9 years, 10-19 years, and 20 or more years, respectively (Exhibit 1.8).

- Workers at establishments that were part of firms with two or more locations had higher offer rates than those with only one location (98.8 percent vs. 63.4 percent) (Exhibit 1.8).

- Offer rates increased with the percentage of workers at the establishment who worked full time. Workers at establishments where 75 percent or more of the employees worked full time had an offer rate of 90.5 percent, compared with 79.6 percent, 75.7 percent, and 55.3 percent for workers at establishments with 50 to 74 percent, 25 to 49 percent, and 0 to 24 percent full-time employees, respectively (Exhibit 1.8).

- Employees in higher wage establishments were more likely to work where health insurance was offered than those in predominantly low-wage establishments (88.1 percent vs. 72.3 percent) (Exhibit 1.8).

Offer Rates by Selected Employer Characteristics and Firm Size

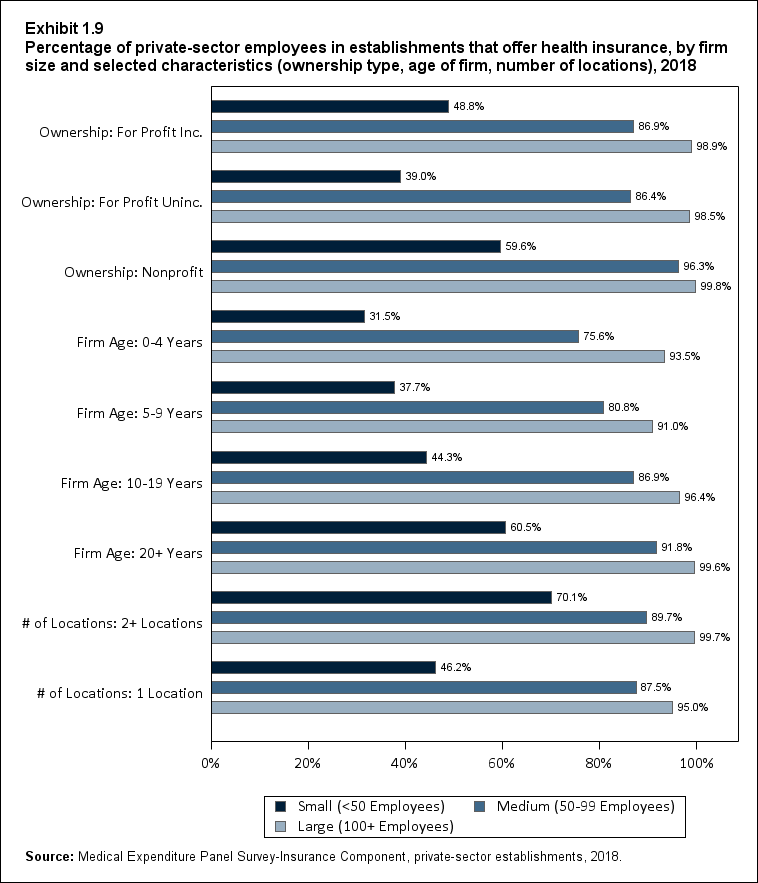

- Among large firms (100 or more employees), employees who worked at an employer that had been in business fewer than 20 years were less likely to be offered health insurance than employees at older firms. Offer rates ranged from 91.0 percent to 96.4 percent at employers in business fewer than 20 years versus 99.6 percent for employers in business 20 years or more (Exhibit 1.9).

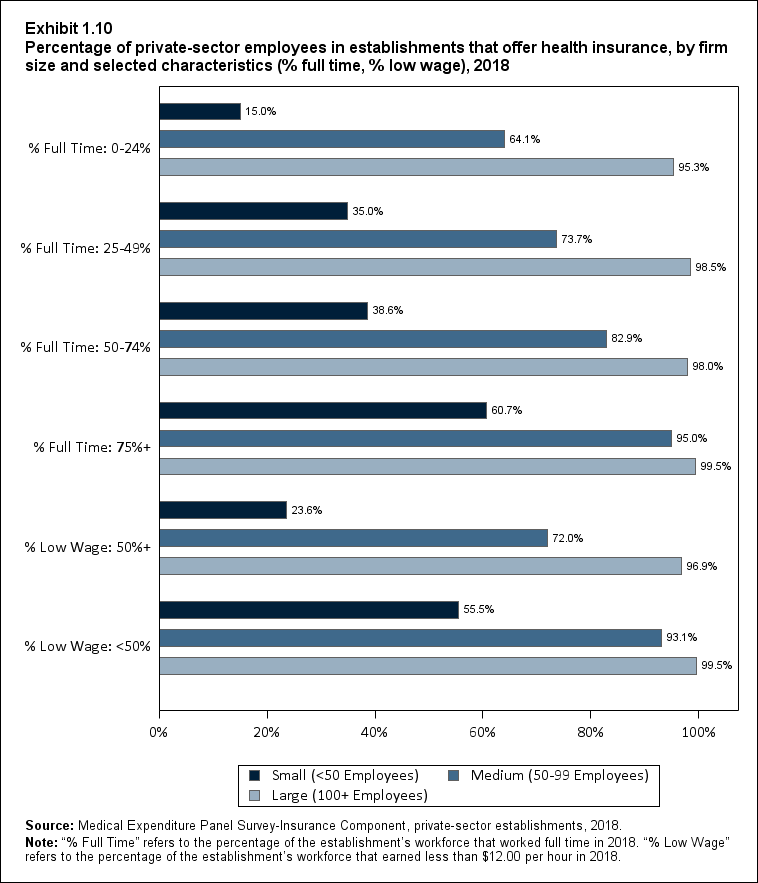

- Also among large firms, the offer rate was lower for employers with 0 to 24 percent full-time workers (95.3 percent) compared with those with a higher percentage of full-time workers (ranging from 98.0 percent to 99.5 percent at employers with 25 percent or more full-time workers) (Exhibit 1.10).

- Overall, 47.3 percent of workers in establishments that were part of firms with fewer than 50 workers were offered coverage in 2018 (Exhibit 1.1). However, there was substantial variation by establishment characteristics. Compared with other categories (e.g., for profit, only one location), offer rates were notably higher for small employers that:

- Were nonprofit (59.6 percent).

- Were in business for 20 or more years (60.5 percent).

- Had more than one location (70.1 percent).

- Had workforces with 75 percent or more of employees working full time (60.7 percent).

- Had workforces that were not predominantly low wage (55.5 percent) (Exhibits 1.9 and 1.10).

- Offer rates were lower for workers in predominantly low-wage establishments than in higher wage establishments, regardless of whether they worked at a firm with fewer than 50 workers (23.6 percent vs. 55.5 percent), 50 to 99 workers (72.0 percent vs. 93.1 percent), or 100 or more workers (96.9 percent vs. 99.5 percent) (Exhibit 1.10).

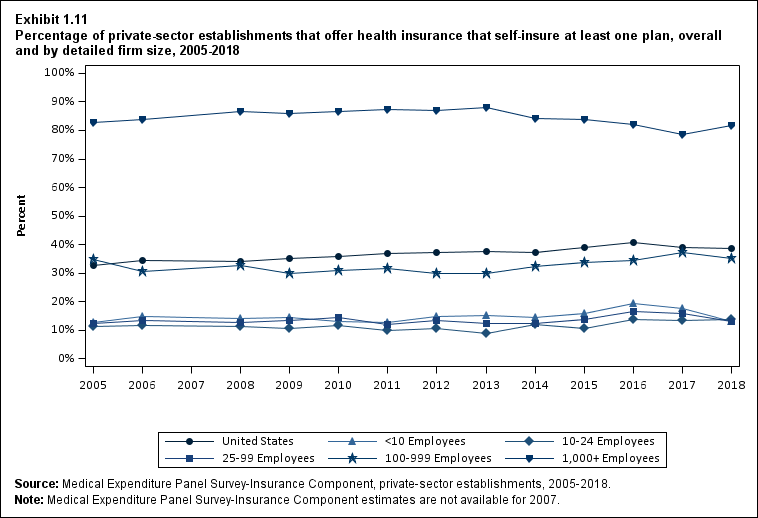

Availability of Self-Insured Plans

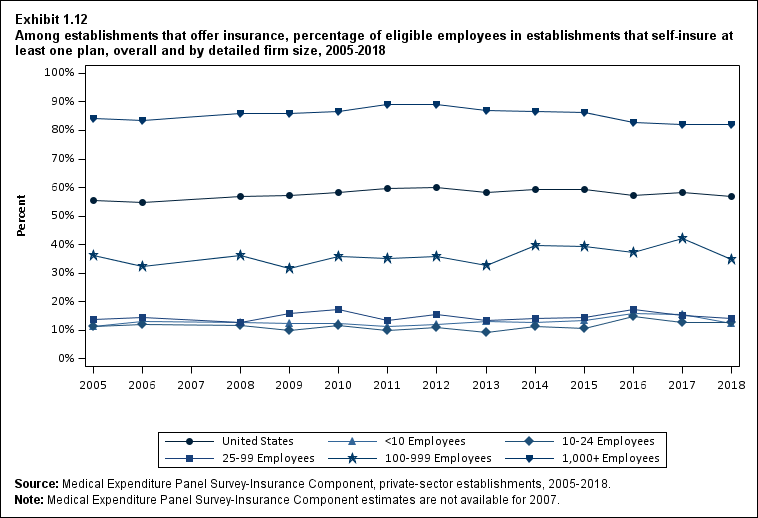

- Among employers that offered insurance, 12.9 percent to 13.8 percent of establishments in the three firm size categories with fewer than 100 workers self-insured at least one plan in 2018. By contrast, 35.1 percent and 81.6 percent of offering establishments in firms with 100 to 999 and 1,000 or more employees, respectively, self-insured at least one plan. There were similar differences by firm size in the percentage of eligible employees who worked for an employer that self-insured at least one plan (Exhibits 1.11 and 1.12).

- Between 2017 and 2018, there was no significant change in the overall percentage of offering establishments that self-insured at least one plan, but this percentage declined at establishments in firms with fewer than 10 employees (from 17.7 percent to 13.1 percent) and with 25 to 99 employees (from 16.0 percent to 12.9 percent). The percentage increased at establishments in firms with 1,000 or more employees (from 78.6 percent to 81.6 percent) (Exhibit 1.11).

- Among employers who offered insurance, there was no significant change from 2017 to 2018 in the overall percentage of eligible employees who worked for an employer that self-insured at least one plan (56.8 percent in 2018). However, employers with fewer than 10 workers and those with 100 to 999 workers both experienced a decrease in this measure from 2017 to 2018 (p <0.10 for employers with fewer than 10 workers) (Exhibit 1.12).

Availability of Dependent Coverage

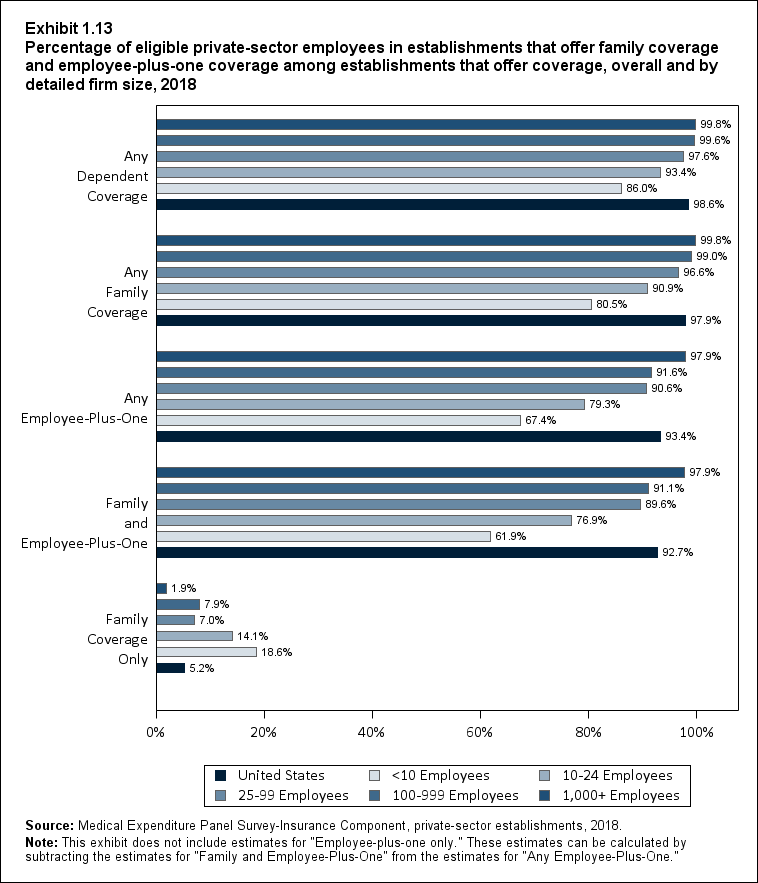

- In 2018, 98.6 percent of all workers who were eligible for single coverage were also offered coverage for their dependents (Exhibit 1.13). The likelihood of a dependent coverage offer increased with firm size, except that rates were similar for the two largest firm size groups. In 2018, the percentage of eligible employees who were offered coverage for their dependents was:

- 86.0 percent in firms with fewer than 10 employees,

- 93.4 percent in firms with 10 to 24 employees

- 97.6 percent in firms with 25 to 99 employees,

- 99.6 percent in firms with 100 to 999 employees, and

- 99.8 percent in firms with 1,000 or more employees.

- In 2018, 93.4 percent of all eligible workers were offered employee-plus-one coverage as an option in addition to an offer of single coverage (Exhibit 1.13). The likelihood of employee-plus-one coverage as an option increased with firm size (except that rates were similar for firms with 25 to 99 and 100 to 999 employees). In 2018, the percentage of eligible workers with an offer of employee-plus-one coverage was:

- 67.4 percent in firms with fewer than 10 employees,

- 79.3 percent in firms with 10 to 24 employees,

- 90.6 percent in firms with 25 to 99 employees,

- 91.6 percent in firms with 100 to 999 employees, and

- 97.9 percent in firms with 1,000 or more employees.

Availability of a Choice of Plans at Employers That Offer Health Insurance, by Firm Size

- The likelihood that a worker at an offering establishment had a choice of plans increased with firm size in all years from 2005 to 2018. In 2018, the percentage of workers with a choice of plans was 37.8 percent in firms with fewer than 50 employees, 56.4 percent in firms with 50 to 99 employees, and 84.7 percent in firms with 100 or more workers (Exhibit 1.14).

- The percentage of employees with a choice of plans increased from 72.4 percent in 2017 to 75.7 percent in 2018. From 2017 to 2018, employees at both large (100 or more employees) and small (fewer than 50 employees) firms experienced an increase in the likelihood of having a choice of plans (Exhibit 1.14).

- The availability of plan choice was significantly higher in 2018 than in 2005 for small employers (37.8 percent vs. 18.2 percent), medium employers (56.4 percent vs. 32.1 percent), and large employers (84.7 percent vs. 69.0 percent) (Exhibit 1.14).

Availability of a Choice of Plans at Employers That Offer Health Insurance, by Industry and Selected Employer Characteristics

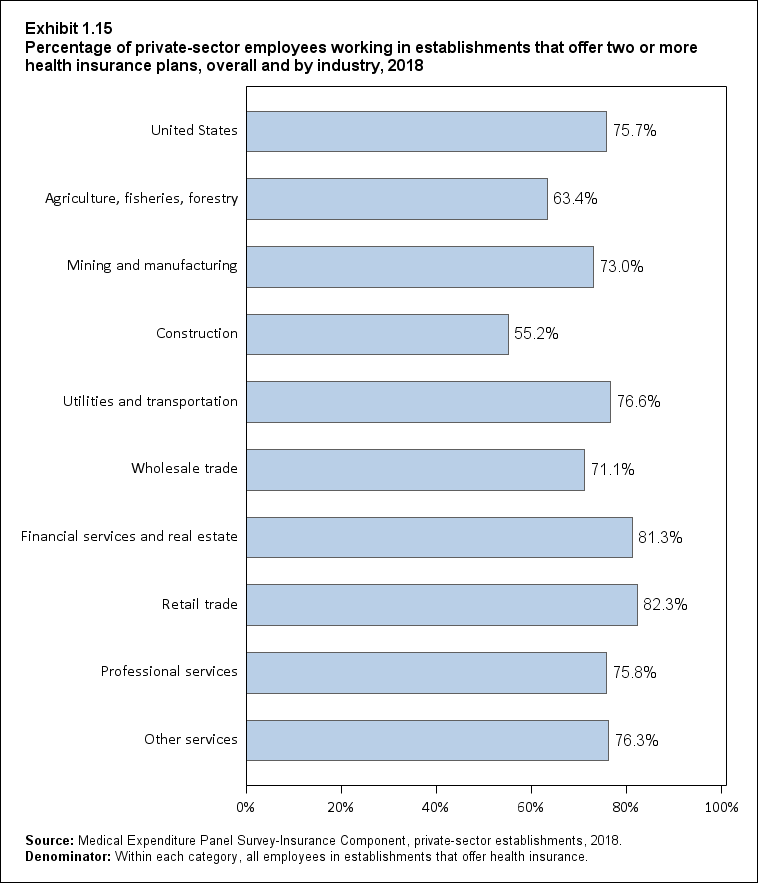

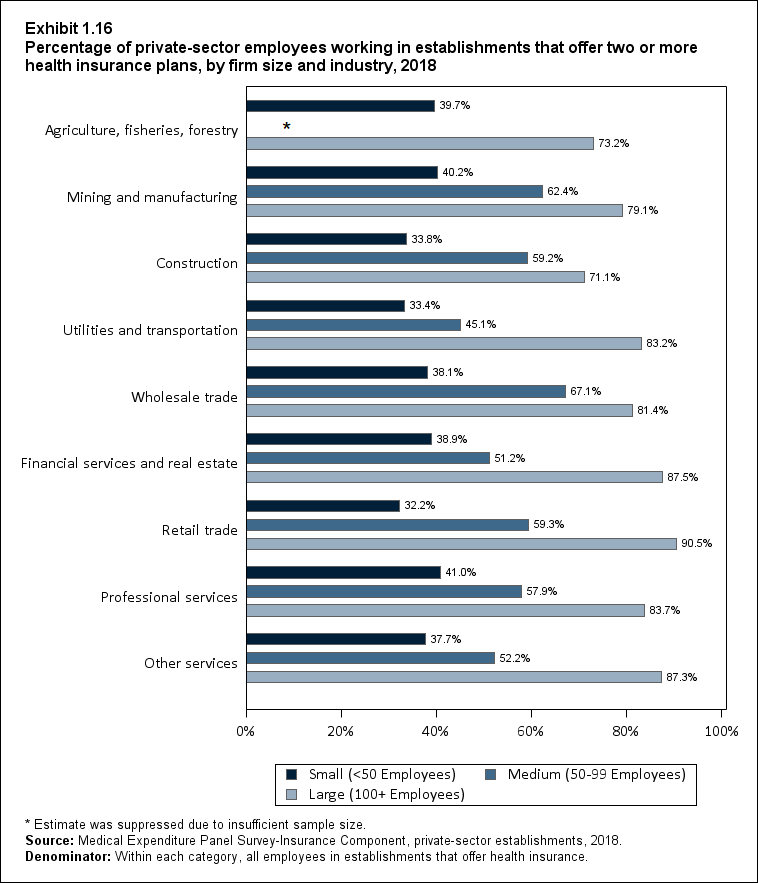

- Workers in financial services and real estate (81.3 percent) and in retail trade (82.3 percent) were more likely to be offered a choice of plans than workers in almost all other industries (there was no significant difference between the financial services and real estate sector and the utilities and transportation sector) (Exhibit 1.15). Exhibit 1.16 shows variation by industry and firm size.

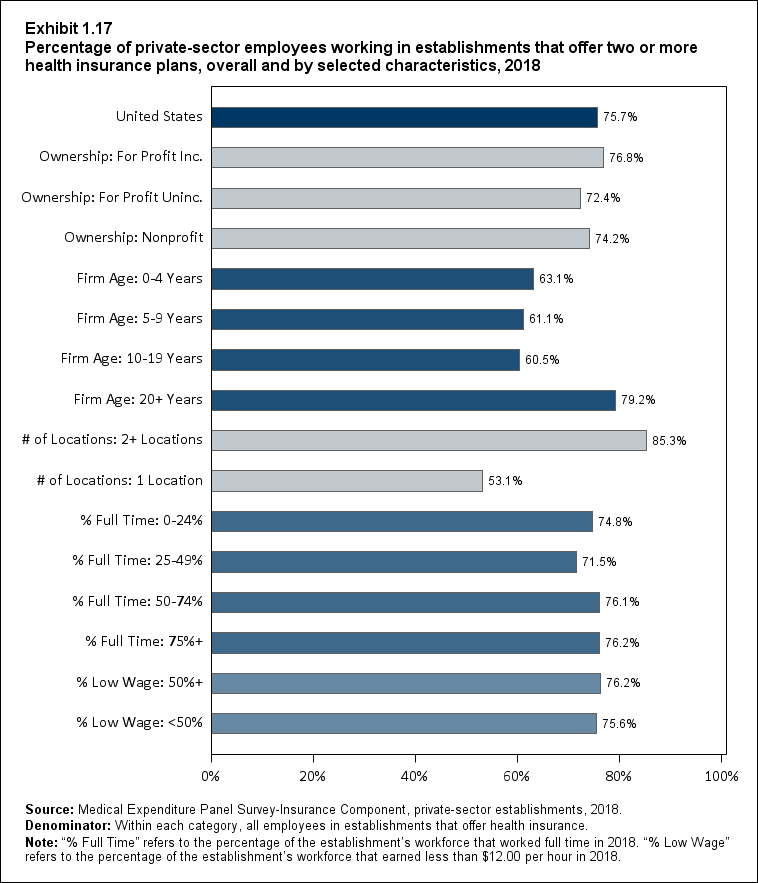

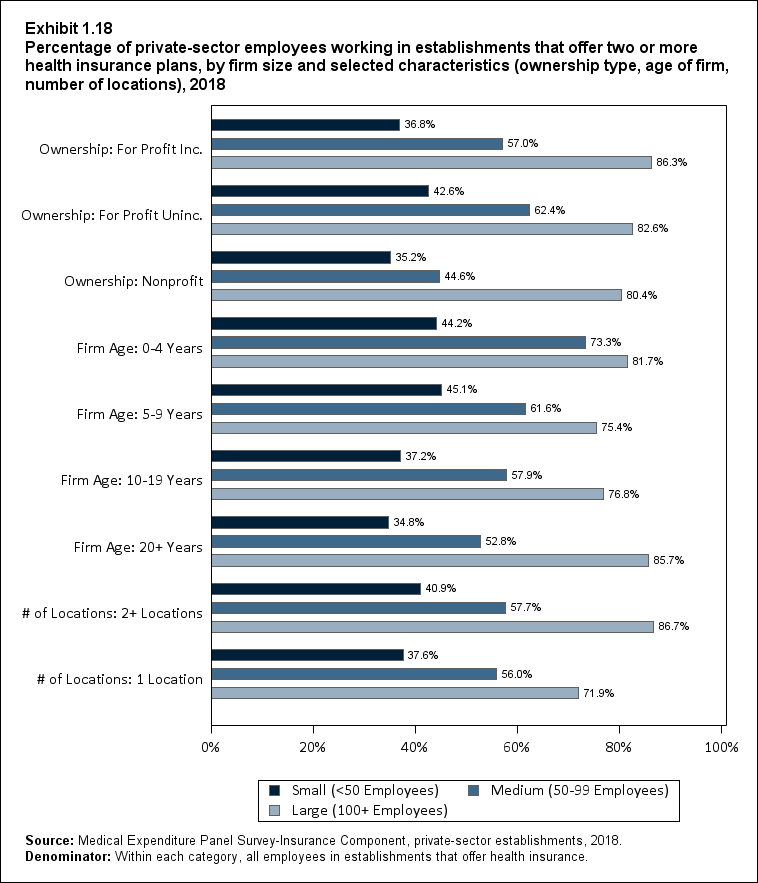

- Workers at for-profit, unincorporated employers were less likely to be offered a choice of plans than workers at for-profit incorporated employers (72.4 percent vs. 76.8 percent) (Exhibit 1.17). Exhibit 1.18 shows variation by ownership and firm size.

- Workers in firms in business for 20 or more years were more likely to be offered a choice of plans (79.2 percent) than employees at younger firms (63.1 percent, 61.1 percent, and 60.5 percent at firms in business for 0 to 4, 5 to 9, and 10 to 19 years, respectively) (Exhibit 1.17).

- Workers at establishments that were part of firms with two or more locations were more likely to be offered a choice of plans than those at firms with only one location (85.3 percent vs. 53.1 percent) (Exhibit 1.17).

- Workers at establishments where 25 to 49 percent of employees worked full time were less likely to be offered a choice of plans than workers at establishments with a higher percentage of employees working full time (p <0.10 for the comparison with 50 to 74 percent of employees working full time) (Exhibit 1.17).

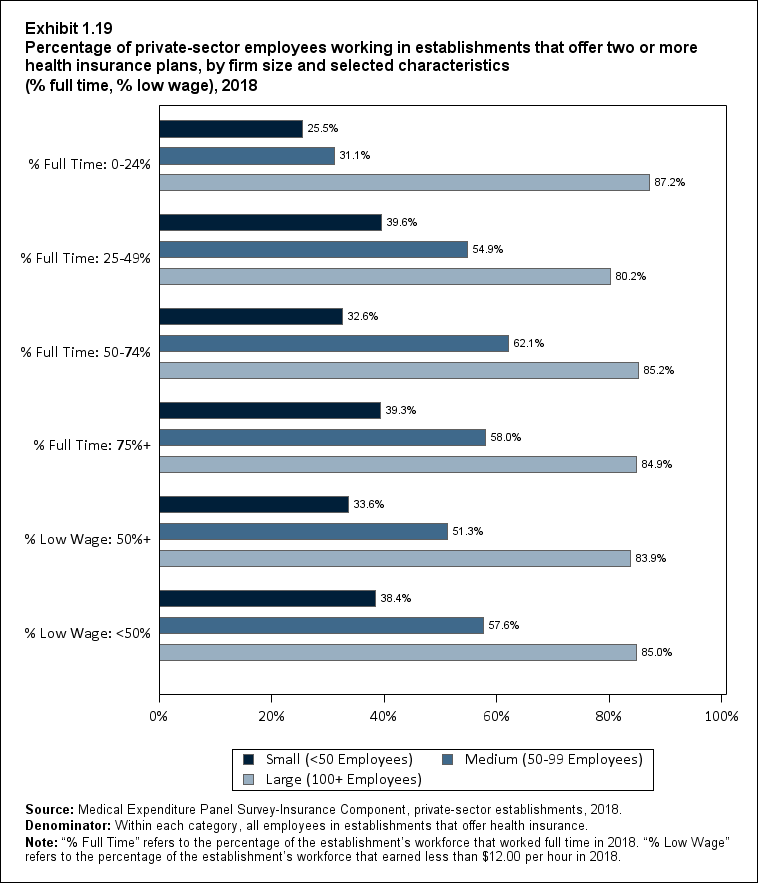

- Overall, there was no significant difference in the availability of a choice of plans by whether or not employees work in predominantly low-wage establishments (Exhibit 1.17). There was also no significant difference by wages in small, medium, and large firms (Exhibit 1.19).

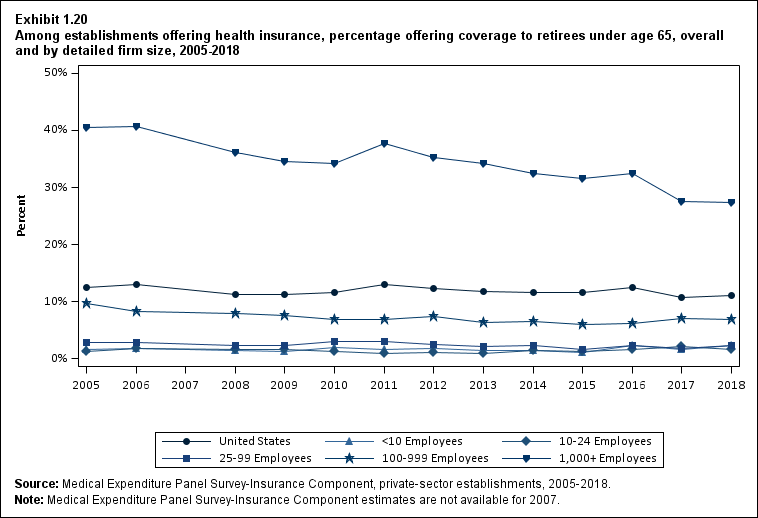

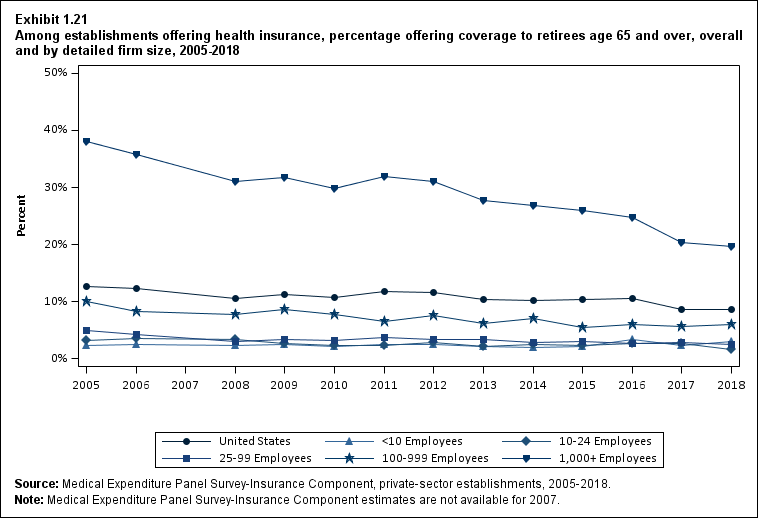

Availability of Retiree Coverage at Establishments That Offer Coverage

- In 2018, workers who retired from establishments that were part of the largest employers that offered employees insurance (1,000 or more workers) were the most likely to be offered retiree coverage. In 2018, 27.4 percent of these establishments offered coverage to retirees under age 65 (Exhibit 1.20). A smaller percentage, 19.7 percent in 2018, offered coverage to retirees age 65 and over (Exhibit 1.21).

- In contrast to the largest employers that offered employees insurance, in 2018, between 1.5 percent and 6.8 percent of their counterparts in all other size categories (fewer than 10, 10 to 24, 25 to 99, and 100 to 999 workers) offered retiree coverage to retirees under age 65 or age 65 and over (Exhibits 1.20 and 1.21).

- Among establishments that offered insurance to employees, there were no significant changes in the rate of offers of retiree coverage between 2017 and 2018, overall or in any firm size category (Exhibits 1.20 and 1.21).

- Between 2005 and 2018, the availability of retiree coverage in the largest firms declined by 13.1 percentage points for retirees under age 65, from 40.5 percent in 2005 to 27.4 percent in 2018. The rate for retirees age 65 and over declined by 18.4 percentage points, from 38.1 percent in 2005 to 19.7 percent in 2018 (Exhibits 1.20 and 1.21).

Return to Table of Contents

Exhibit 1.1 Percentage (standard error) of private-sector employees in establishments that offer health insurance, by firm size, 2005‑2018

| Number of Employees |

2005 |

2006 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

| U.S. |

86.9% |

86.9% |

87.7% |

87.6% |

86.5% |

85.3% |

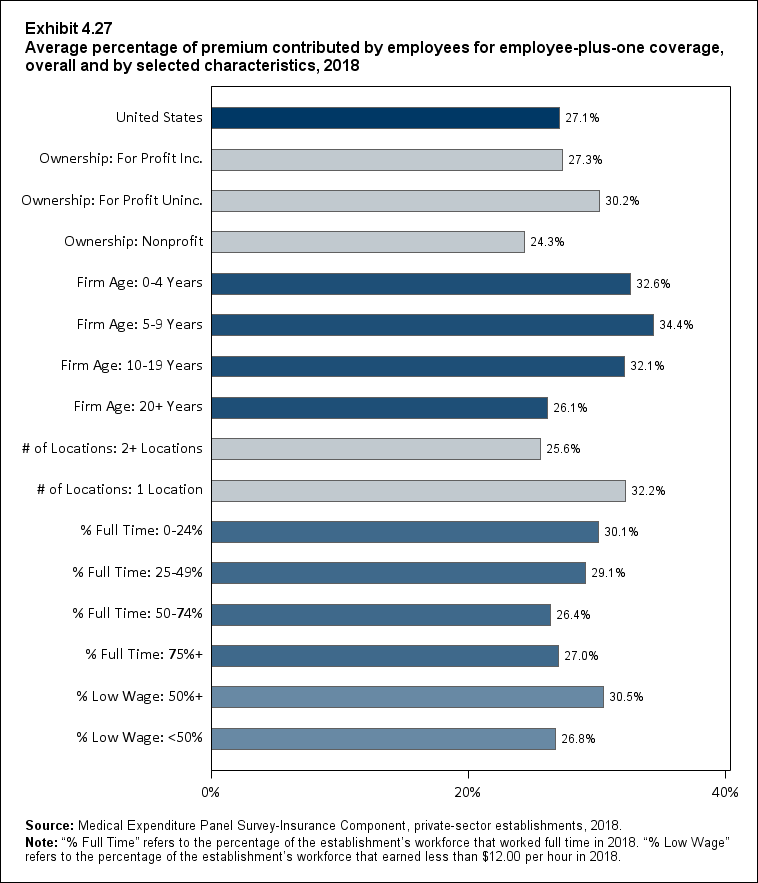

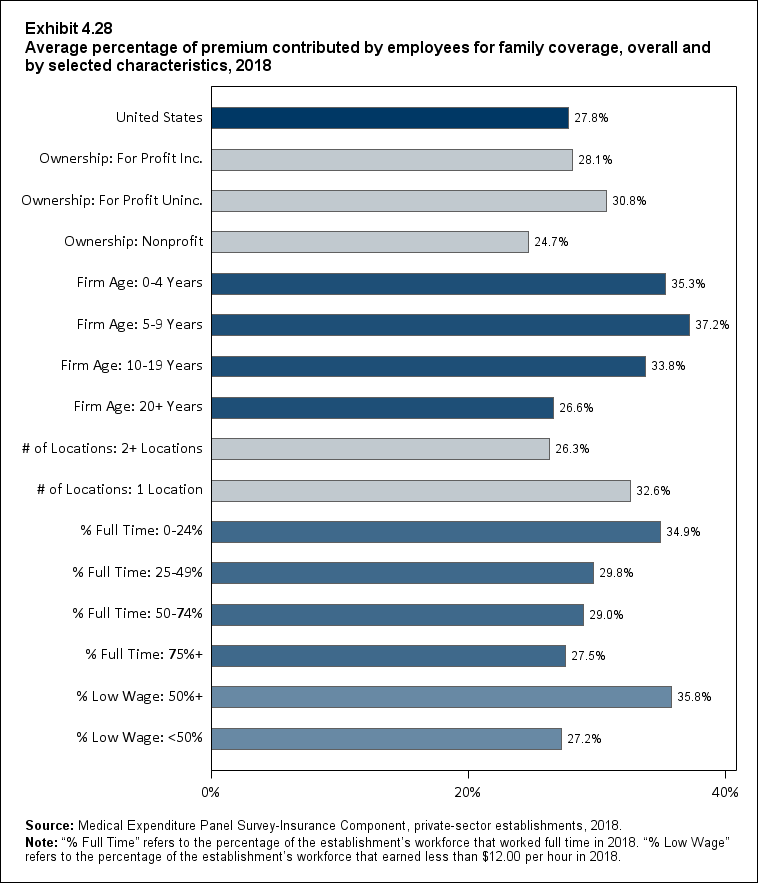

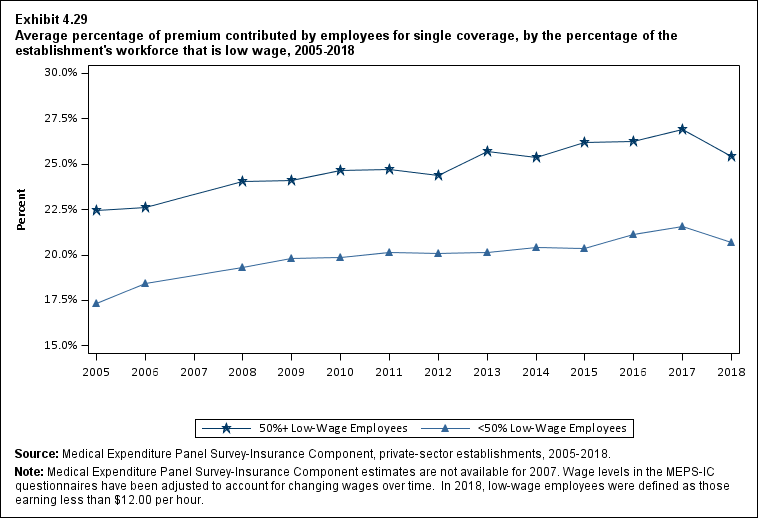

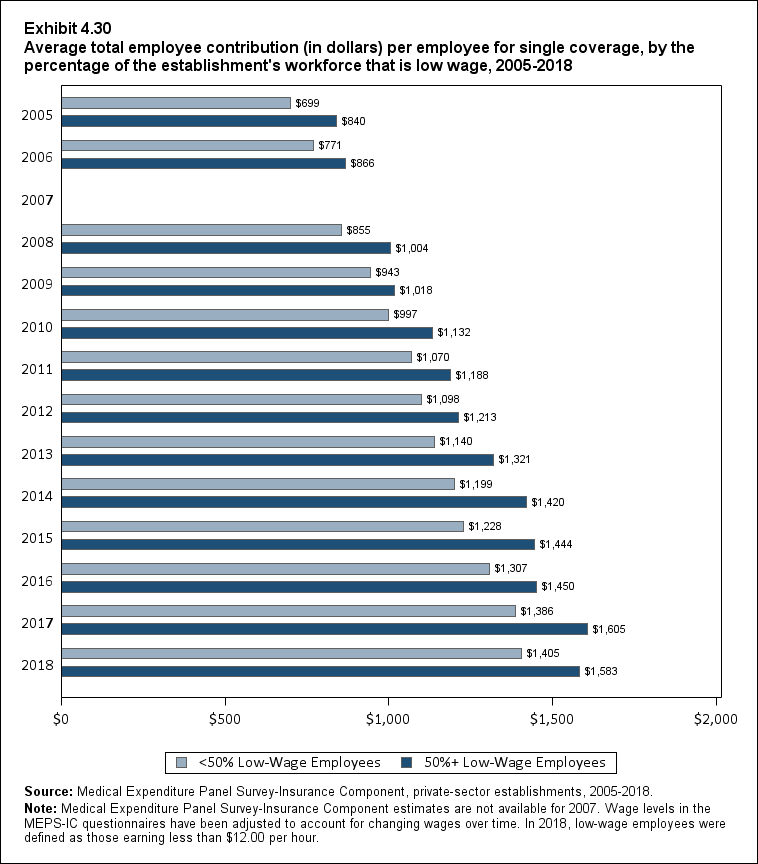

84.7% |