Skip to main content

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

STATISTICAL BRIEF #553: Trends in Health Insurance at Private Employers, 2008-2022 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| October 2023 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

G. Edward Miller, PhD, and Patricia Keenan, PhD

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Highlights

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

IntroductionEmployer-sponsored insurance is the primary source of health insurance coverage for individuals under the age of 65. This Statistical Brief uses private-sector national tables data from the Medical Expenditure Panel Survey-Insurance Component (MEPS-IC) to describe trends in employer coverage, premiums, and deductibles from 2008 to 2022. The MEPS-IC is an annual survey of private employers and state and local governments. It is designed to be representative of all 50 states and the District of Columbia.This Statistical Brief describes trends and patterns in employer-sponsored insurance for private-sector employees overall and by three firm size categories: fewer than 50 employees (small firms), 50 to 99 employees (medium-sized firms), and 100 or more employees (large firms). All differences discussed in the text are at the 0.05 significance level or better. All dollar estimates are nominal (not adjusted for inflation). |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

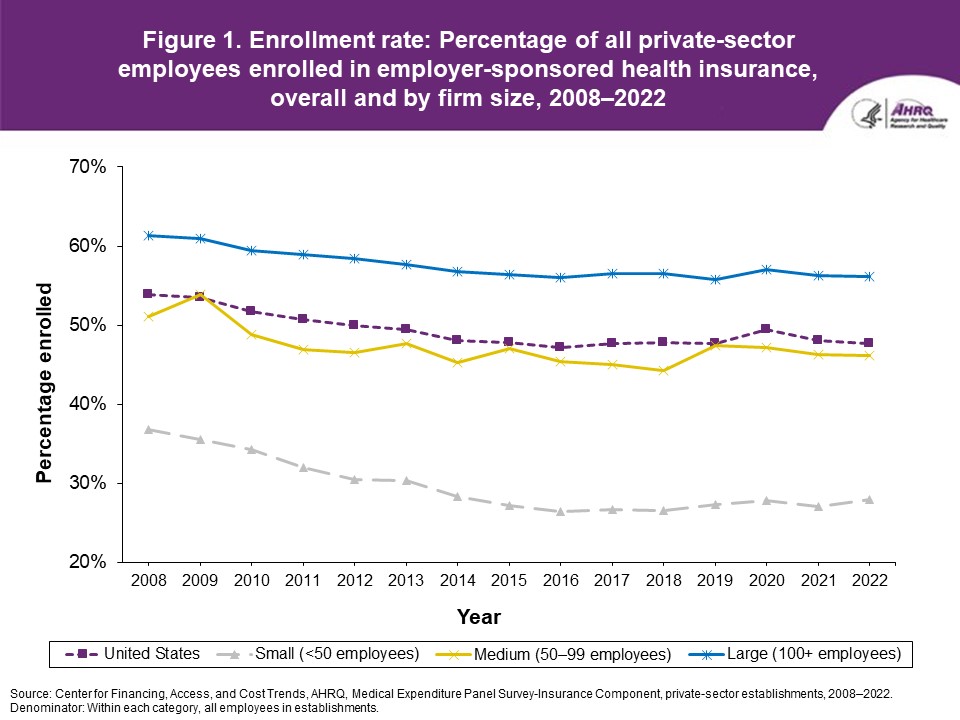

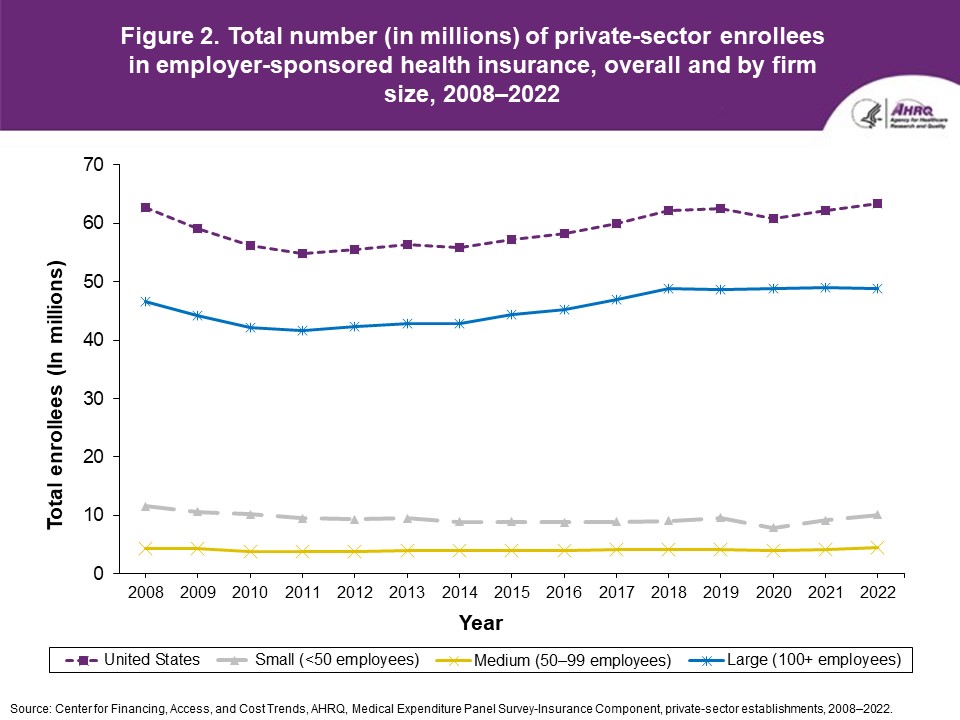

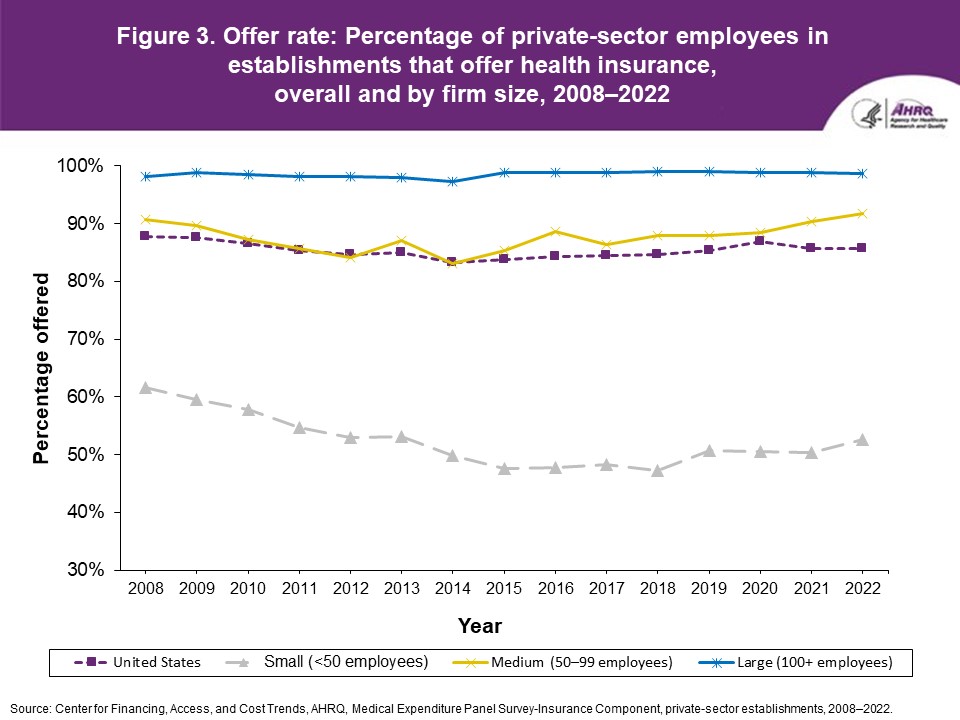

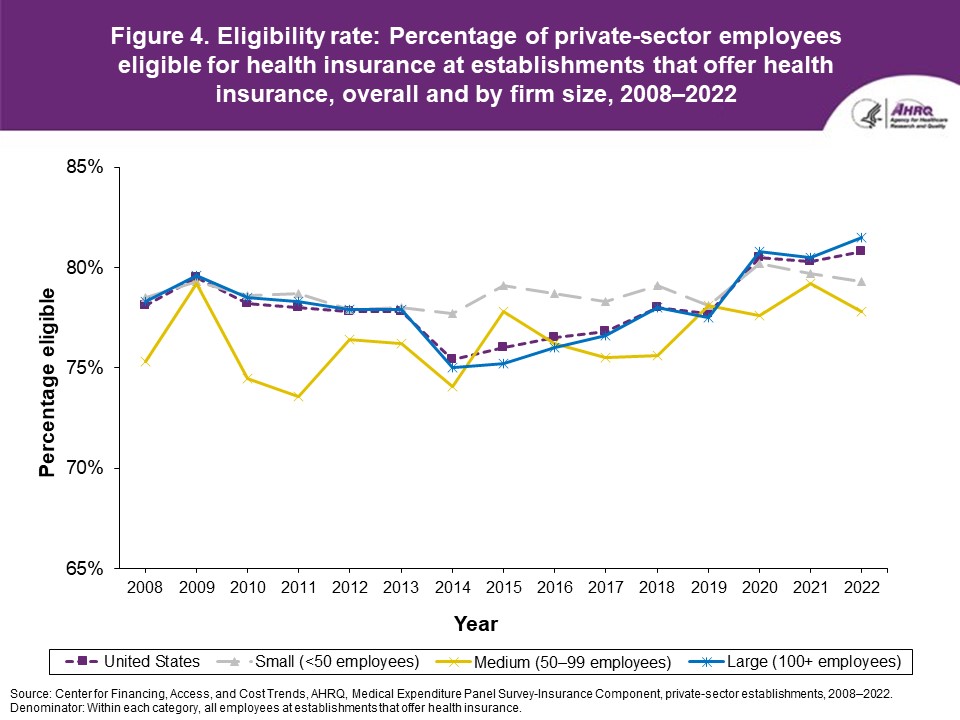

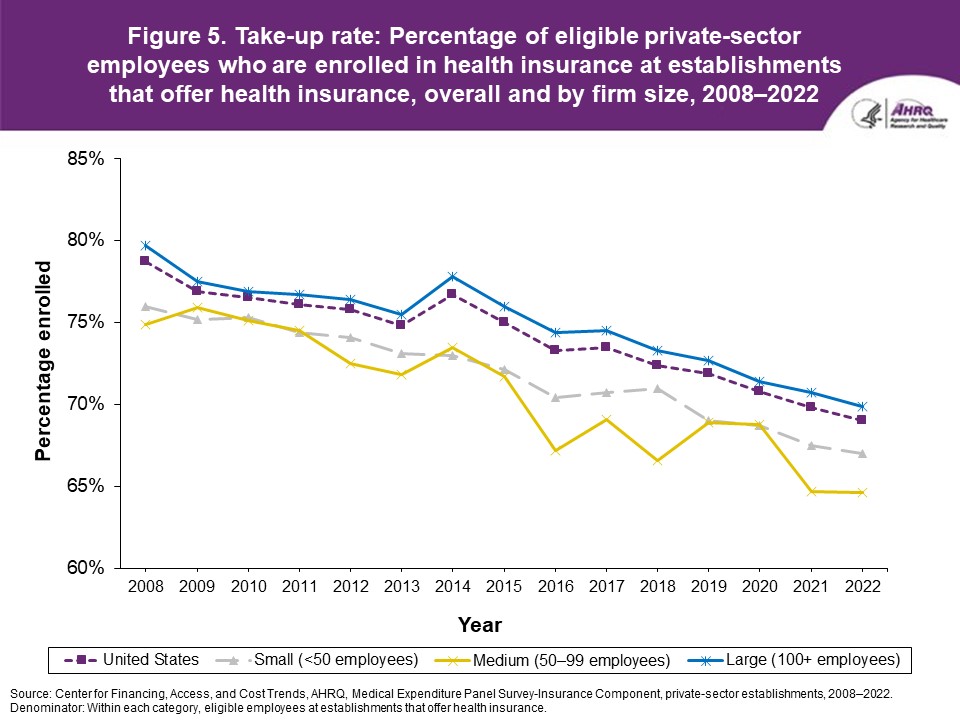

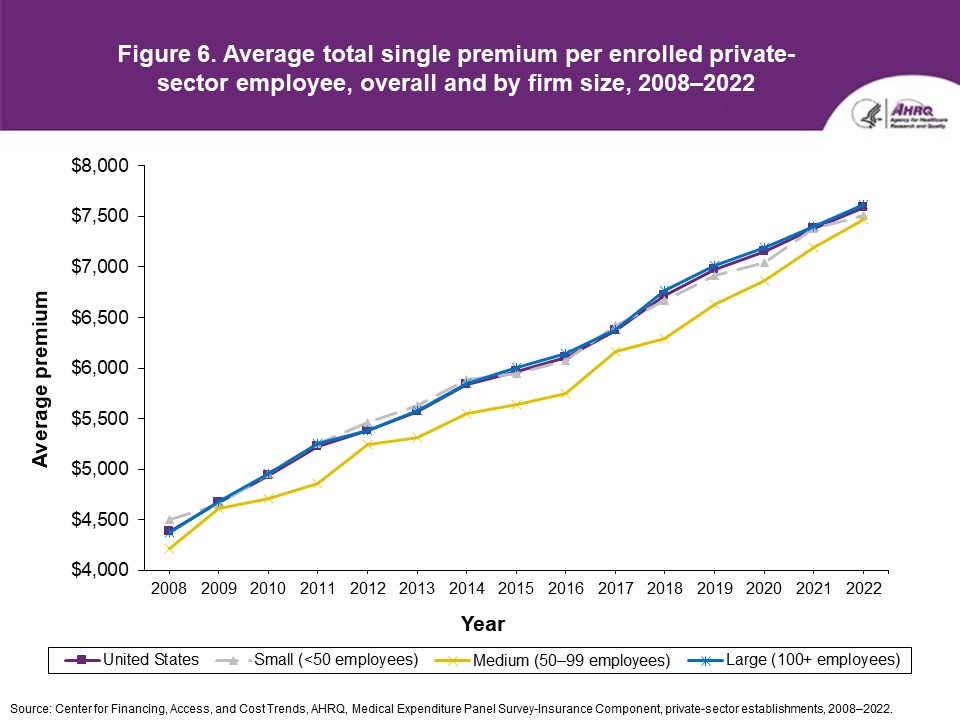

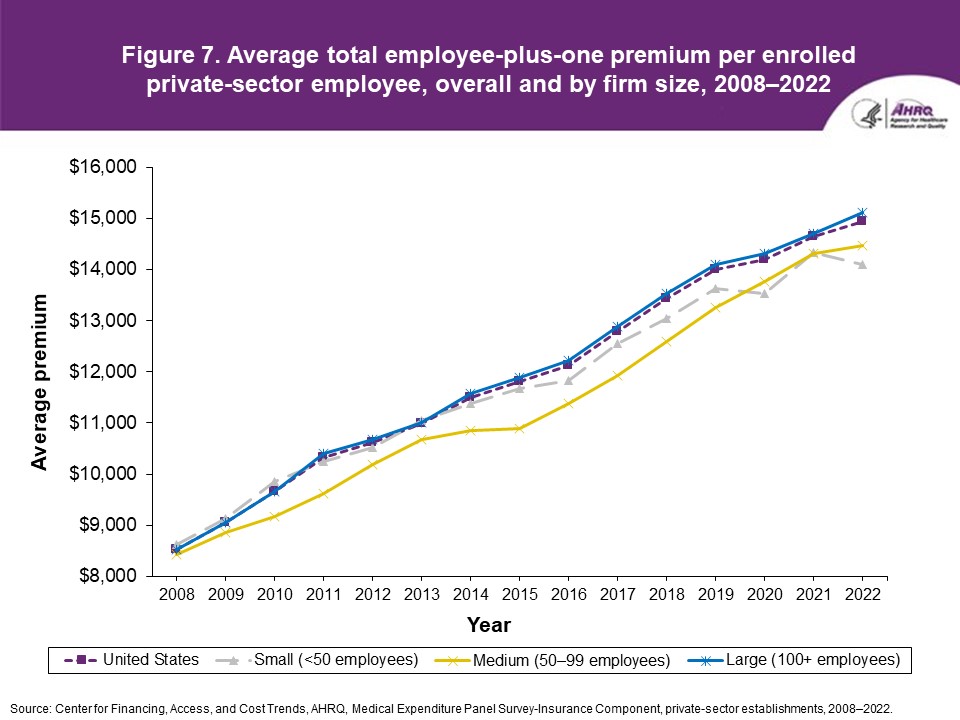

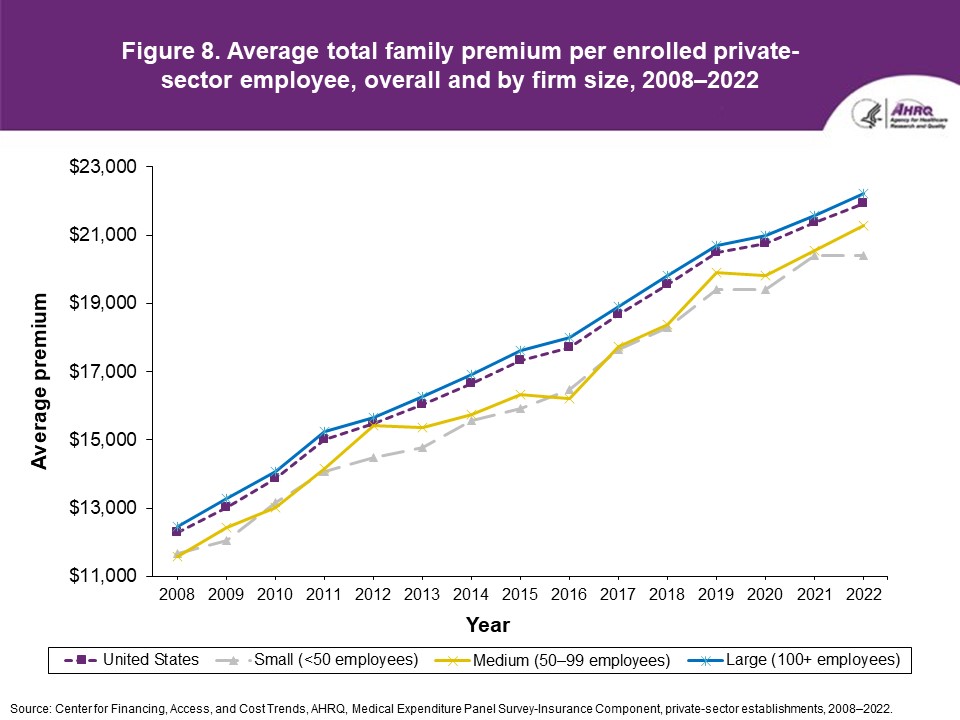

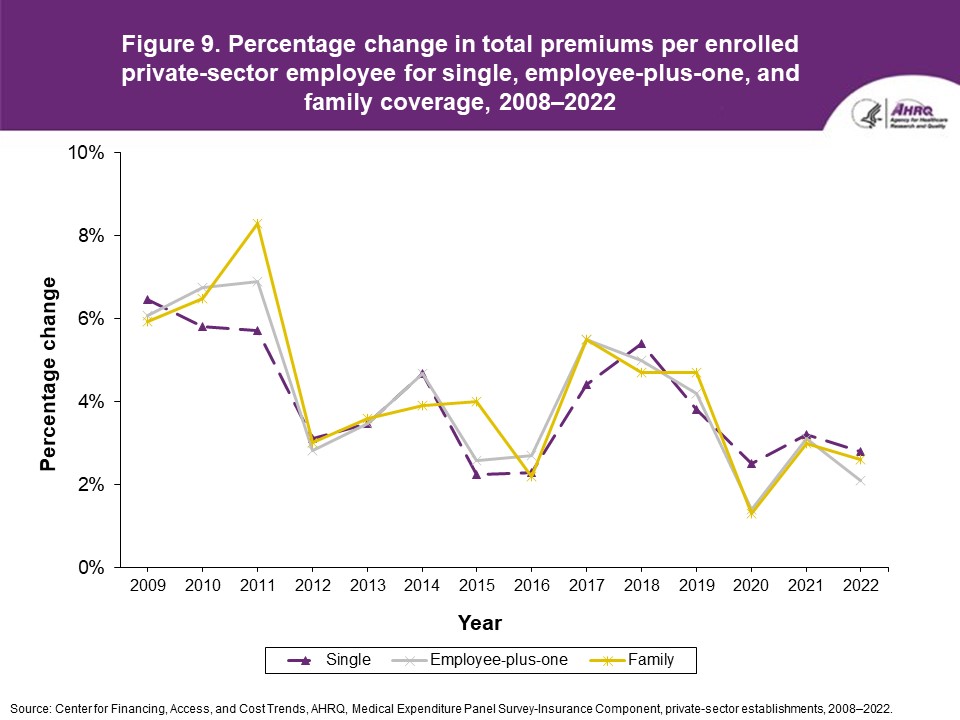

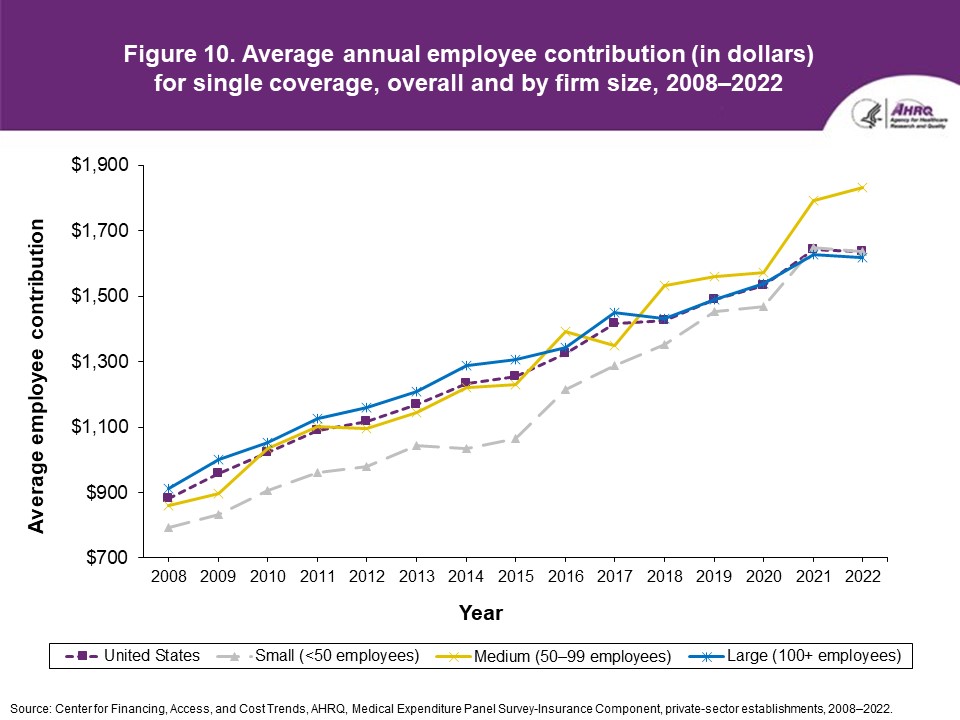

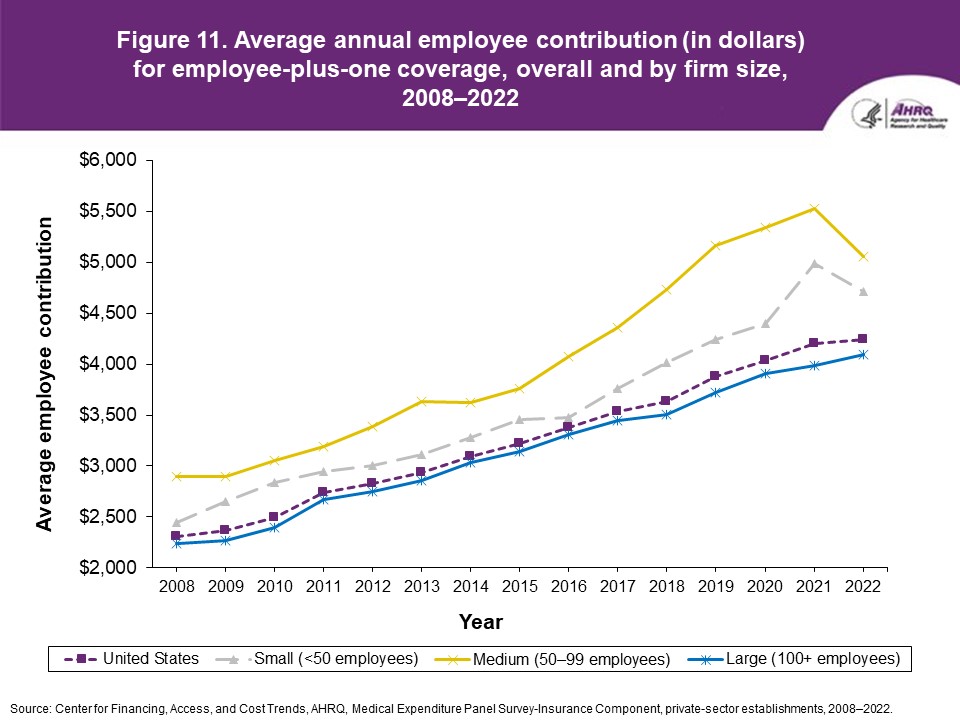

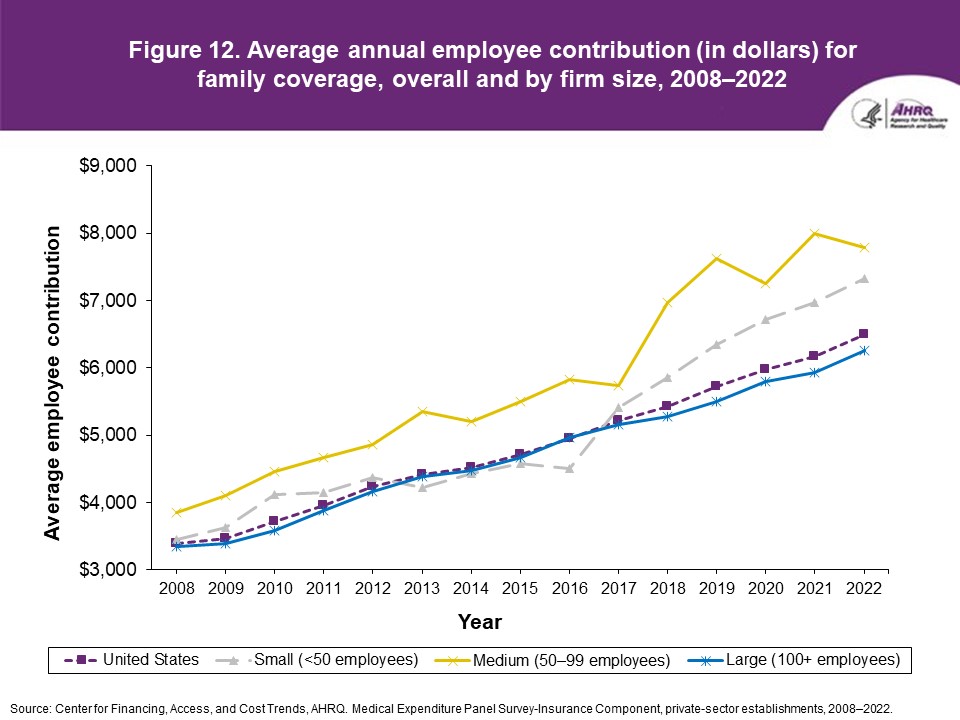

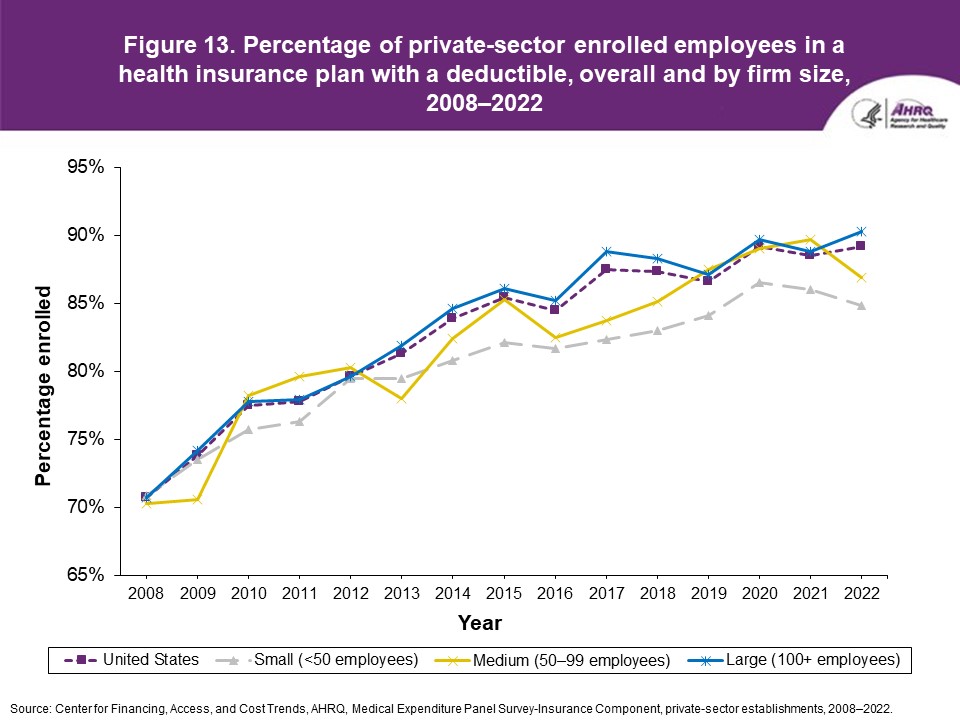

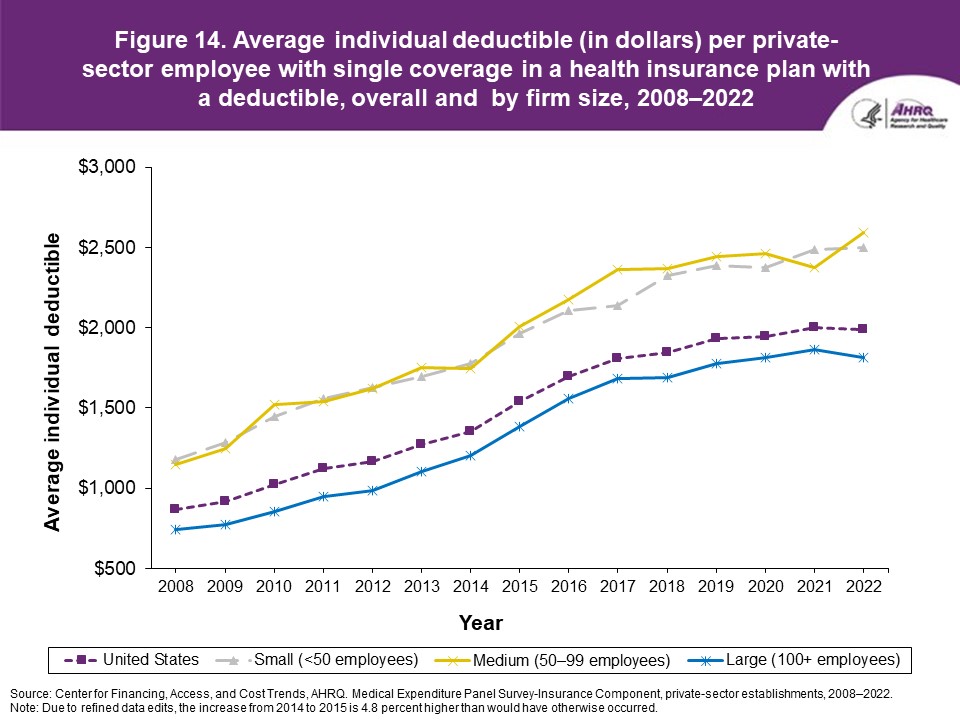

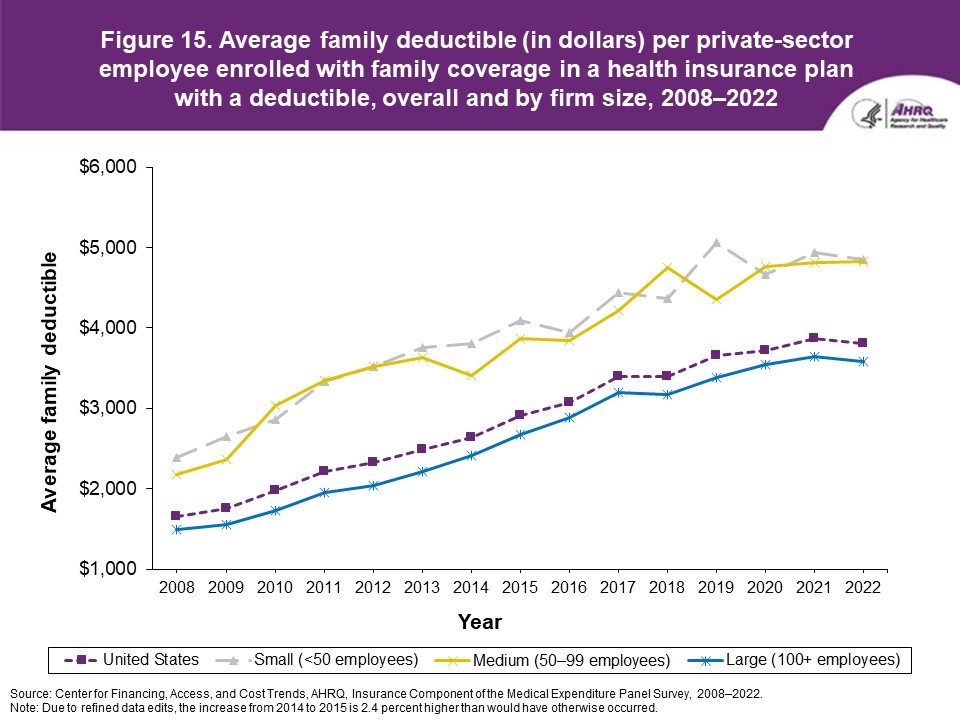

FindingsEnrollment rates and number of covered employees (figures 1-2)The overall enrollment rate—the percentage of private-sector employees covered by a health insurance plan offered by their employers—did not change significantly from 2021 (48.0 percent) to 2022 (47.7 percent) (figure 1). In 2022, the enrollment rate ranged from 27.9 percent at small employers to 56.2 percent at large employers.From 2021 to 2022, the point estimate for the total number of private-sector employees enrolled in a health insurance plan offered by their employers increased from 62.2 million to 63.4 million, but this change was not statistically significant (figure 2). Among small employers, the total number of employees enrolled in a health insurance plan offered by their employer increased from 9.2 million to 10.1 million. Offer rates (figure 3)Overall, there was no significant change in the offer rate—the percentage of employees working at an establishment that offered insurance—from 2021 (85.7 percent) to 2022 (85.6 percent) (figure 3). The offer rate at small firms, however, increased from 50.4 percent in 2021 to 52.6 percent in 2022, extending the recent period of stability and increases for small firm offer rates. Over the last 7 years, the small firm offer rate either remained stable or increased each year and rose by a total of 5.0 percentage points, from 47.6 percent in 2015 to 52.6 percent in 2022. This represents a significant change in this trend from the previous 7 years, when the small firm offer rate fell by 14.0 percentage points—from 61.6 percent in 2008 to 47.6 percent in 2015—with significant year-to-year decreases seen in nearly every year.Eligibility rates (figure 4)Overall, the eligibility rate was unchanged; 80.8 percent of employees at private-sector establishments that offered insurance were eligible for coverage in 2022 (figure 4). Similarly, the eligibility rates for small (79.3 percent), medium (77.8 percent), and large employers (81.5 percent) were not statistically different from 2021 eligibility rates. Overall, the eligibility rate showed little year-to-year variation from 2008 (78.1 percent) to 2019 (77.7 percent) before increasing by 2.8 percentage points in 2020 (80.5 percent) and maintaining that higher level in 2021 (80.3 percent) and 2022 (80.8 percent).Take-up rates (figure 5)The overall take-up rate for employees at private-sector establishments who were eligible for insurance did not show a statistically significant change from 2021 (69.8 percent) to 2022 (69.0 percent) (figure 5). From 2008 to 2022, the overall take-up rate fell by 9.7 percentage points (from 78.7 percent to 69.0 percent) and take-up rates fell by similar amounts in small (9.0 percentage points), medium (10.3 percentage points), and large firms (9.8 percentage points). In 2022, the take-up rate among large firms (69.9 percent) remained higher than in medium (64.6 percent) and small firms (67.0 percent), as has been true in almost every year from 2008 through 2022.Premiums (figures 6-9)In 2022, average health insurance premiums were $7,590 for single coverage, $14,943 for employee-plus-one coverage, and $21,931 for family coverage, representing increases of 2.8 percent, 2.1 percent, and 2.6 percent, respectively, relative to 2021 levels (figures 6-9).1 The overall growth in average premiums from 2021 to 2022 was driven by large firms, which had increases in average premiums of 2.8 percent to 3.0 percent for single, employee-plus-one, and family coverage. There were no significant changes in premiums among small and medium firms. In 2022, average family premiums were lower for small ($20,406) and medium employers ($21,289) than for large employers ($22,228).Employee premium contributions (figures 10-12)From 2021 to 2022, average employee contributions for family coverage increased by 5.2 percent overall (from $6,174 to $6,492) and increased by 5.5 percent among large firms (from $5,937 to $6,263) (figure 12). By contrast, there were no significant changes, overall or by firm size, in employee contributions for single and employee-plus-one coverage, which had overall average contributions in 2022 of $1,637 and $4,237, respectively (figures 10 and 11). In 2022, average employee contributions for the two types of dependent coverage—employee-plus-one and family—were lower at large employers ($4,096 and $6,263, respectively), than at small employers ($4,711 and $7,324, respectively) and medium employers ($5,052 and $7,788, respectively).Deductibles (figures 13-15)The percentage of enrollees in a health insurance plan with a deductible in 2022 was not significantly different from 2021 for firms overall (89.2 percent), or for small (84.8 percent), medium (86.9 percent), or large (90.3 percent) employers (figure 13). From 2008 to 2022, the percentage of enrollees with a deductible increased by 13.9 percentage points among small firms, by 16.6 percentage points among medium firms, and by 19.6 percentage points among large firms. In 2022, enrollees in small and medium firms were less likely than those in large firms to have a deductible.From 2021 to 2022, there was no significant change in overall average individual deductibles ($1,992 in 2022) (figure 14) or family deductibles ($3,811 in 2022) (figure 15). From 2008 to 2022, average individual and family deductibles increased at an average annual rate of 6.1 percent and showed significant increases every year during this period except for 2018, 2020, and 2022. Average individual deductibles were higher in small ($2,499) and medium firms ($2,596) than in large firms ($1,814) in 2022. Family deductibles were also higher in small ($4,854) and medium firms ($4,822) than in large firms ($3,581) in 2022. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Data SourceThis Statistical Brief summarizes data from 2008 through 2022 from the MEPS-IC. The data are available on the MEPS website at http://www.meps.ahrq.gov/mepsweb/survey_comp/Insurance.jsp or have been produced using special computation runs on the confidential MEPS-IC data available at the U.S. Census Bureau. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

DefinitionsSingle coverageSingle coverage is health insurance that covers the employee only.Employee-plus-one coverageEmployee-plus-one coverage is health insurance that covers the employee and one other family member at a lower premium level than family coverage. If premiums differed for employee-plus-spouse and employee-plus-child coverage, information for employee-plus-child coverage was collected.Family coverageFamily coverage is health insurance that covers the employee and one or more family members (spouse and/or children as defined by the plan). For the MEPS-IC survey, family coverage is any coverage other than single and employee-plus-one coverage. Some plans offer more than one rate for family coverage, depending on family size and composition. If more than one rate is offered, survey respondents are asked to report costs for a family of four.Enrollment rateThe enrollment rate is the percentage of all employees enrolled in their employer's health insurance at establishments both offering and not offering health insurance.Offer rateThe offer rate is the percentage of employees who work at establishments that offer health insurance.Eligible employeesEligible employees are those that are allowed to enroll in employer-sponsored health insurance offered by their employer. Common eligibility criteria include a minimum number of hours worked per pay period or a minimum length of service with the employer.EmployeeAn employee is a person on the payroll. This definition excludes temporary and contract workers but includes the owner or manager if that person works at the firm.EstablishmentAn establishment is a single physical location of a business.Health insurance planA health insurance plan is an insurance contract that provides hospital and/or physician coverage to an employee for an agreed-upon fee (premium) for a defined benefit period.Take-up rateThe take-up rate is the percentage of eligible employees who enroll in health insurance coverage through their employer at establishments that offer insurance.DeductibleA deductible is a fixed dollar amount during the benefit period—usually a year—that an insured person pays before the insurer starts to make payments for covered medical services. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

About MEPSThe MEPS-IC is a survey of private-sector business establishments and state and local governments that collects information on employer-sponsored health insurance, such as whether insurance is offered, enrollments, types of plans, and premiums. The survey is conducted annually by the U.S. Census Bureau under the sponsorship of the Agency for Healthcare Research and Quality (AHRQ). A total sample of approximately 42,000 private-sector establishments was selected for the 2022 survey, with 5.8 percent of the sample determined to be out of scope during the data collection process. The response rate for the private-sector was 54.6 percent of the remaining in-scope sample units. Private sector responses to the 2022 survey were collected from June 2022 through March 2023. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Suggested CitationMiller, G.E. and Keenan P. Trends in Health Insurance at Private Employers, 2008-2022. Statistical Brief #553. October 2023. Agency for Healthcare Research and Quality, Rockville, MD. https://meps.ahrq.gov/data_files/publications/st553/stat553.shtmlAHRQ welcomes questions and comments from readers of this publication who are interested in obtaining more information about access, cost, use, financing, and quality of healthcare in the United States. We also invite you to tell us how you are using this Statistical Brief and other MEPS data and tools and to share suggestions on how MEPS products might be enhanced to further meet your needs. Please email us at MEPSProjectDirector@ahrq.hhs.gov or send a letter to the address below: Joel W. Cohen, PhD, Director Center for Financing, Access and Cost Trends Agency for Healthcare Research and Quality 5600 Fishers Lane, Mailstop 07W41A Rockville, MD 20857 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 1. Enrollment rate: Percentage of all private-sector employees enrolled in employer-sponsored health insurance, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 2. Total number (in millions) of private-sector enrollees in employer-sponsored health insurance, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 3. Offer rate: Percentage of private-sector employees in establishments that offer health insurance, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 4. Eligibility rate: Percentage of private-sector employees eligible for health insurance at establishments that offer health insurance, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 5. Take-up rate: Percentage of eligible private-sector employees who are enrolled in health insurance at establishments that offer health insurance, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 6. Average total single premium per enrolled private-sector employee, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 7. Average total employee-plus-one premium per enrolled private-sector employee, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 8. Average total family premium per enrolled private-sector employee, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 9. Percentage change in total premiums per enrolled private-sector employee for single, employee-plus-one, and family coverage, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 10. Average annual employee contribution (in dollars) for single coverage, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 11. Average annual employee contribution (in dollars) for employee-plus-one coverage, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 12. Average annual employee contribution (in dollars) for family coverage, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ. Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 13. Percentage of private-sector enrolled employees in a health insurance plan with a deductible, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 14. Average individual deductible (in dollars) per private-sector employee with single coverage in a health insurance plan with a deductible, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ. Medical Expenditure Panel Survey-Insurance Component, private-sector establishments, 2008-2022. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Figure 15. Average family deductible (in dollars) per private-sector employee enrolled with family coverage in a health insurance plan with a deductible, overall and by firm size, 2008-2022

Source: Center for Financing, Access, and Cost Trends, AHRQ, Insurance Component of the Medical Expenditure Panel Survey, 2008-2022. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

1 Some of the estimates in this Brief (including the percentage increases in this sentence) are not shown in the figures but were calculated from the estimates in the figures. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||